Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

Weekly Market Update – 29th July 2022

Investment markets and key developments over the past week

- The bounce back in shares continued over the last week on hopes that slowing growth will see central banks ease up on the pace of monetary tightening helped along by mostly good earnings results. However, while US and European shares rose, Japanese and Chinese shares fell. The positive global lead along with a less bad than feared CPI result reducing the risk of a further step up in RBA rate hikes pushed the Australian share market higher, with gains led by resources stocks despite a dividend cut from RIO, property stocks and financials. Bond yields fell on expectations for slower growth, but oil, metal and iron ore prices rose. The $A also rose as the $US pulled back a bit.

- Shares have had a good rebound from their June lows but views remain that they are still at high risk of further falls: the rally since the June lows has been lacking in conviction; clearer signs are needed that inflation has peaked such that central banks can slow and then stop raising rates; it’s still early days in the profit downgrade cycle; uncertainty remains high regarding how badly economic activity will be hit; and the period out to September/October is often weak for shares particularly when their trend is already down. On a 6-12 month horizon remain optimistic on shares as inflation recedes, central banks become less hawkish & a deep recession is likely to be avoided – but there is a way to go yet.

- The Fed raised rates by another 0.75% taking the Fed Funds rate to a range of 2.25 to 2.5% and remains hawkish. While there were no new hawkish surprises and Chair Powell noted that at some point rate hikes will slow down (which markets took favourably) the key messages remained hawkish with Powell noting that inflation is too high, the Fed is strongly committed to bringing it under control, another 0.75% hike is on the table for September, the Fed Funds rate could still be on its way to 3.8% and that while the Fed is not seeking to bring on a recession the path to avoiding one has narrowed.

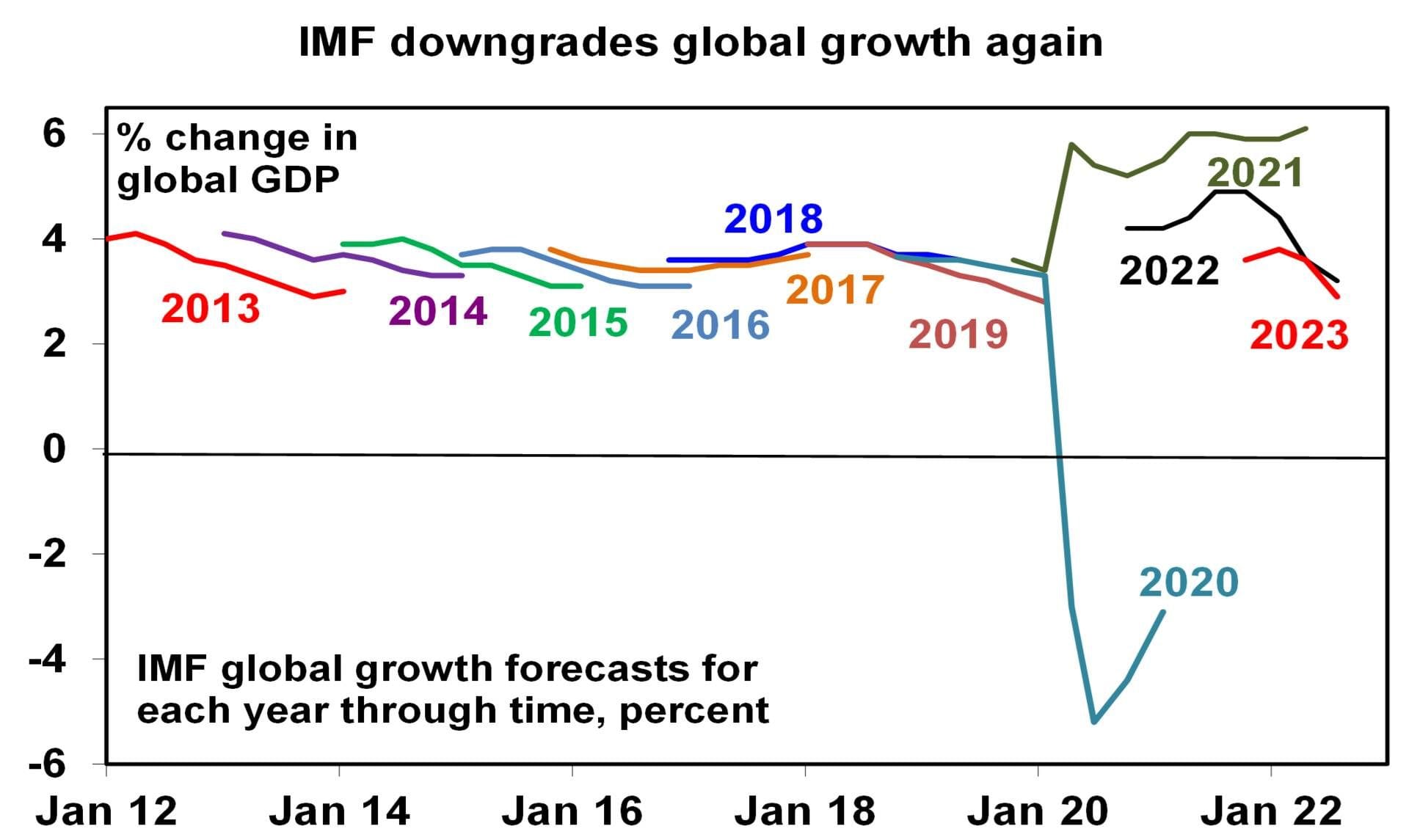

- The IMF downgraded the global growth outlook again and increased its inflation forecasts. Citing monetary tightening, China lockdowns and spillovers from the war in Ukraine the IMF cut its global growth forecasts again to 3.2% for 2022 and to 2.9% for 2023. While it’s not forecasting recession it notes that the risks are tilted to the downside. It also revised its rich country inflation forecast up to 6.6% for this year and to 3.3% for next year. There is nothing new in any of this for investment markets where the deteriorating economic outlook has already been factored in – but the next chart comparing IMF global growth forecast through time highlights the extreme volatility in economic forecasts since the pandemic began.

Source: IMF, AMP

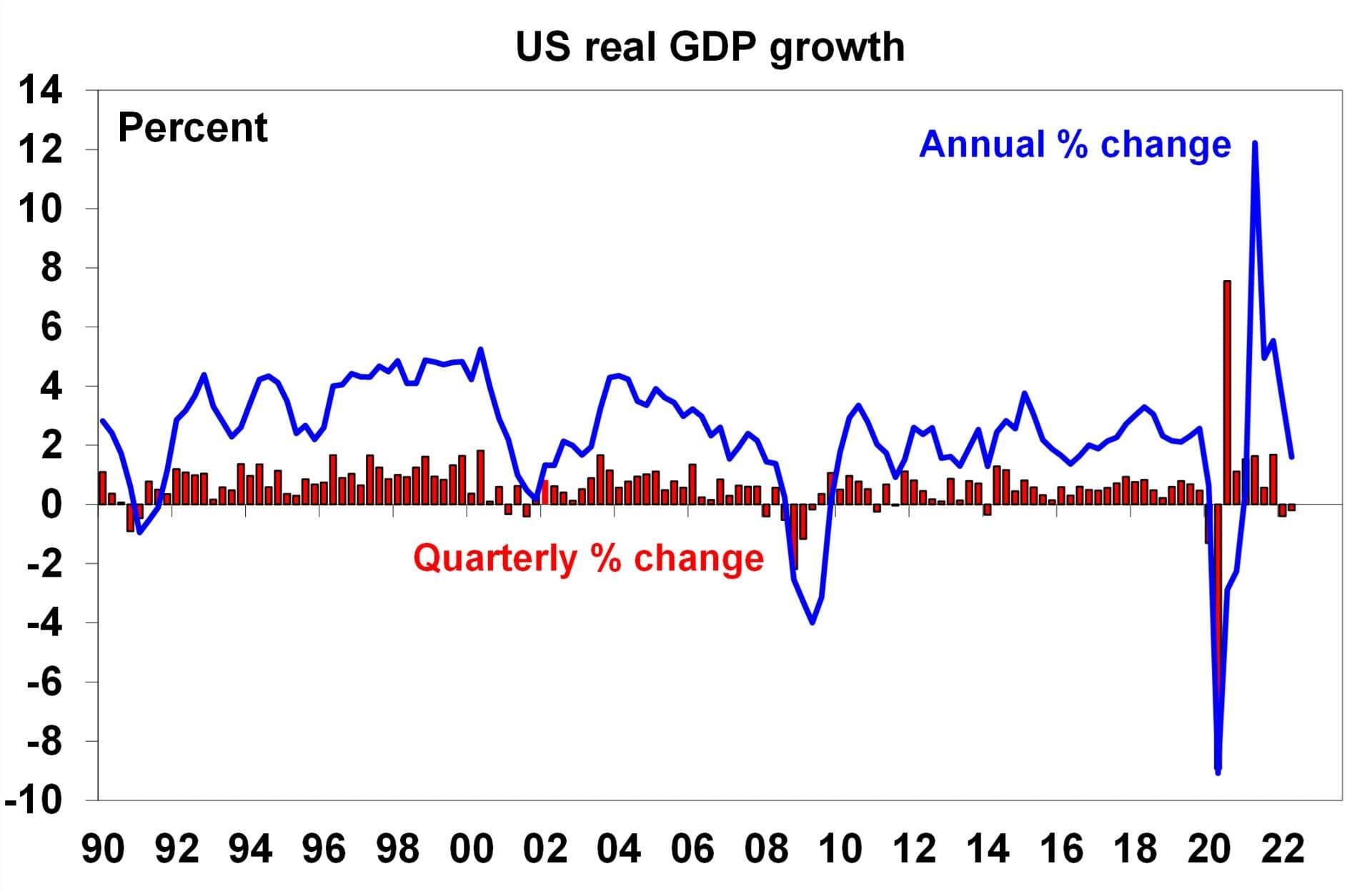

- US in a “technical recession”. US June quarter GDP contracted by -0.9% annualised which after the March quarter contraction met the technical “two quarters in a row of GDP falls” concept of a recession but with inventories playing a big role in the fall and payrolls still strong it’s unlikely to be classified as a recession by the NBER, at least not yet…

Source: Bloomberg, AMP

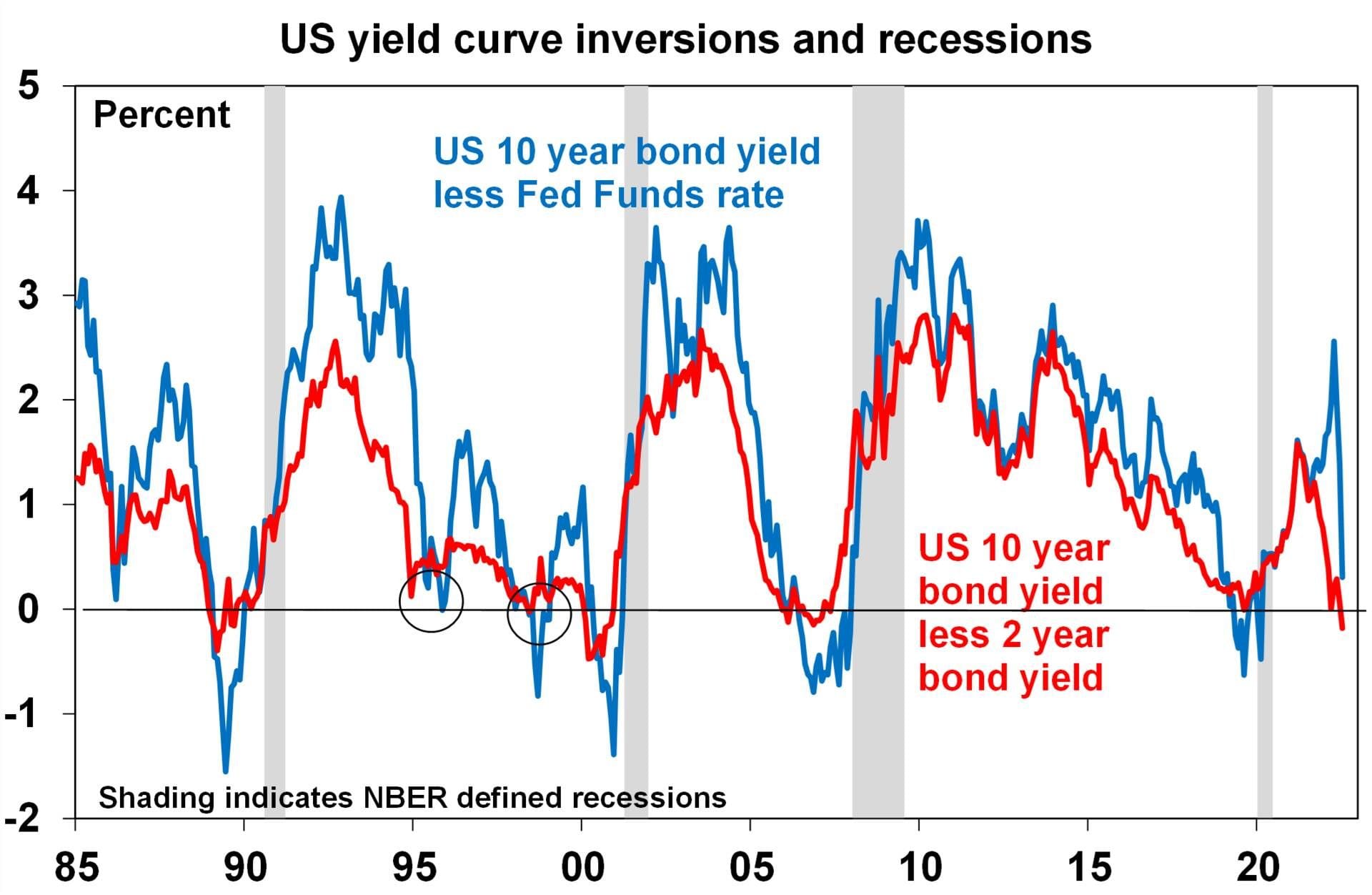

- … the risk of a real recession in the US is continuing to increase with the US 10-year less 2-year yield curve remaining inverted and the 10-year less Fed Funds rate gap getting close to inverting too.

Source: Bloomberg, AMP

- Russia’s announcement that it will cut gas flows to Europe through the Nord Stream 1 pipeline from 40% to 20% supposedly due to maintenance issues (but more likely as part of a strategy to destabilise Europe and weaken its resolve in penalising Russia) have further increased the risk of recession in Germany and to a lesser degree Europe.

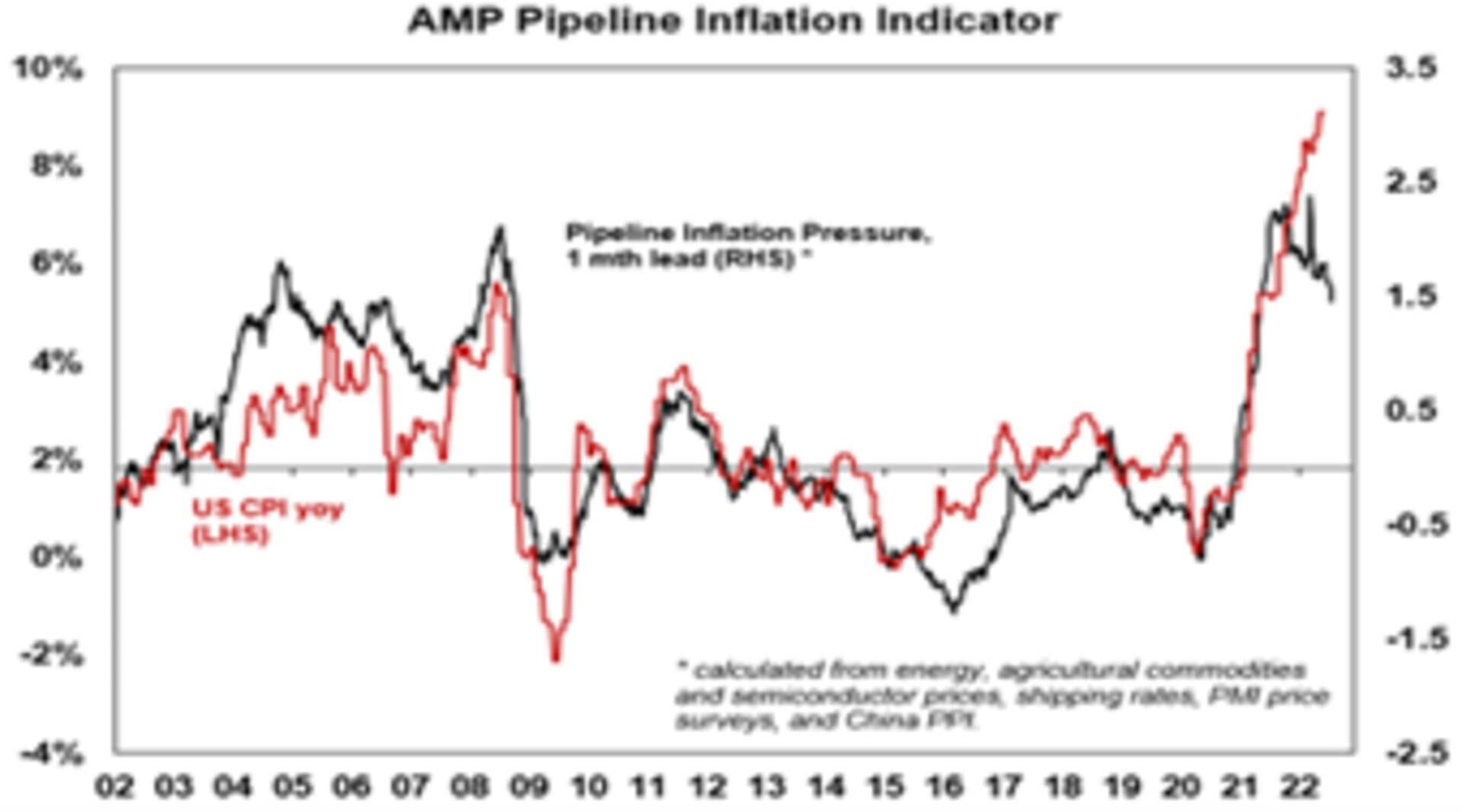

- The good news remains that global inflation pressures may be at or close to peaking. The US Pipeline Inflation Indicator is continuing to trend down reflecting a combination of a falling trend in work backlogs, freight rates, metal prices, grain prices and even oil prices. This is likely to flow through to cooler monthly inflation readings over the next 6 months in the US and then eventually elsewhere which – along with evidence of slowing demand should start to take pressure off central banks and slow the pace of rate hikes in time to avoid a recession, or at least a deep recession. Of course, there is a long way to go.

The Inflation Pipeline Indicator is based on commodity prices, shipping rates and PMI price components. Source: Bloomberg, AMP

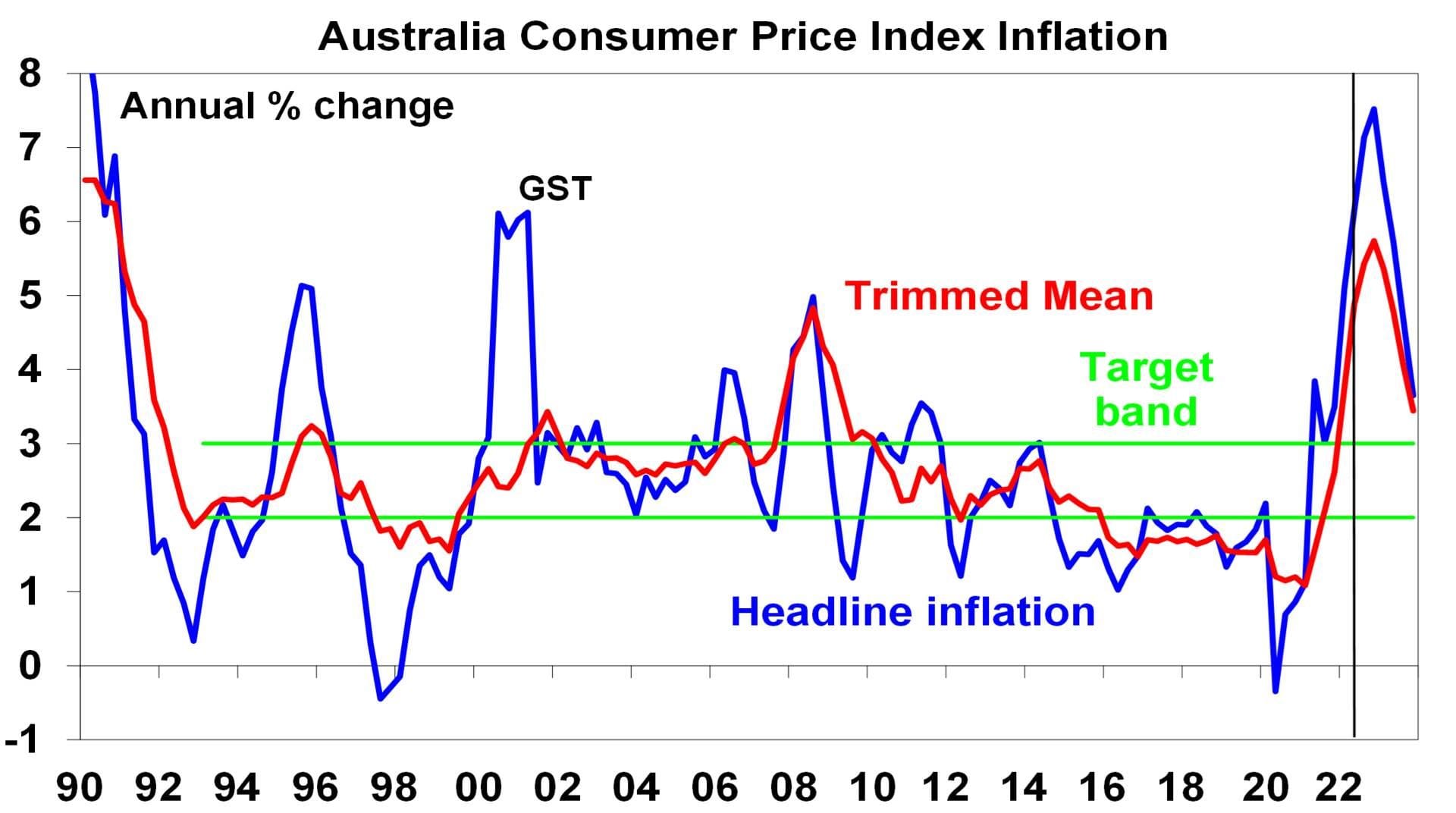

- Another rise in inflation in Australia to 6.1% for the June quarter keeps the RBA on track for another 0.5% rate hike in the week ahead but it wasn’t high enough to justify another step up in the pace of tightening to 0.75%. The CPI increase was slightly below market expectations. But nevertheless inflation is still going up, underlying price pressures are still rising with the trimmed mean inflation rate rising to 4.9%yoy which is its highest since 1990, the breadth of price increases in the CPI basket greater than 3%yoy rose again to 65%, various government subsidies (for transport fares, tourism and childcare) helped keep inflation down a bit and a further increase to 7-7.5% by December is likely as higher power and gas prices impact along with the scheduled reversal of the cut to fuel excise. The reversal of the fuel excise cut alone will add 0.5% to December quarter inflation.

- The assessment is that inflation will peak around 7-7.5% this half year and that the peak in the cash rate will be around 2.6% either late this year (if the RBA continues to go fast) or early next year. Supply pressures appear to be easing a bit globally with declines in freight costs, input and output prices, metal and food prices and reduced delivery lags (as indicated by the Pipeline Inflation Indicator), energy prices should stabilise next year and the plunge in consumer confidence and home prices is pointing to a slowing in Australian demand, all of which should lead to a fall back in inflation through next year.

Source: ABS, AMP

- Market expectations for the cash rate to rise to around 3.5% will likely crash the property market and the economy. The implication from the RBA’s relatively relaxed view on the ability of the Australian household sector to withstand rising interest rates and argument that the cash rate remains well below its estimate of the so-called “neutral rate” have been interpreted by some as supporting expectations for the cash rate to rise above 3%. The RBA has to sound tough to keep inflation expectations down, which is what it’s been doing lately, it’s unlikely that rates will need to rise that far and if they do it will cause a major problem for the economy. While it’s true that many households are well ahead on their mortgage payments many seeing a massive increase in their monthly debt servicing bill. On the RBA’s own analysis around 1.3 million households are set to see a 40% or greater increase in their mortgage payments with a 3% rise in interest rates. This at a time of falling real wages will have a huge impact on spending in the economy and risk a significant rise in forced property sales. Coming at a time when home prices are already falling rapidly due the impact of rising rates on home buyer demand it will only add to home price falls which will weigh further on consumer spending. And the neutral rate of interest concept was also of little use in the pre-pandemic period when rates were below estimates of neutral and yet growth remained weak. As such the assessment remains that the RBA won’t need to raise rates above 3% and it is expected to see the peak in the cash rate as being around 2.6% either later this year or early next year.

Coronavirus update

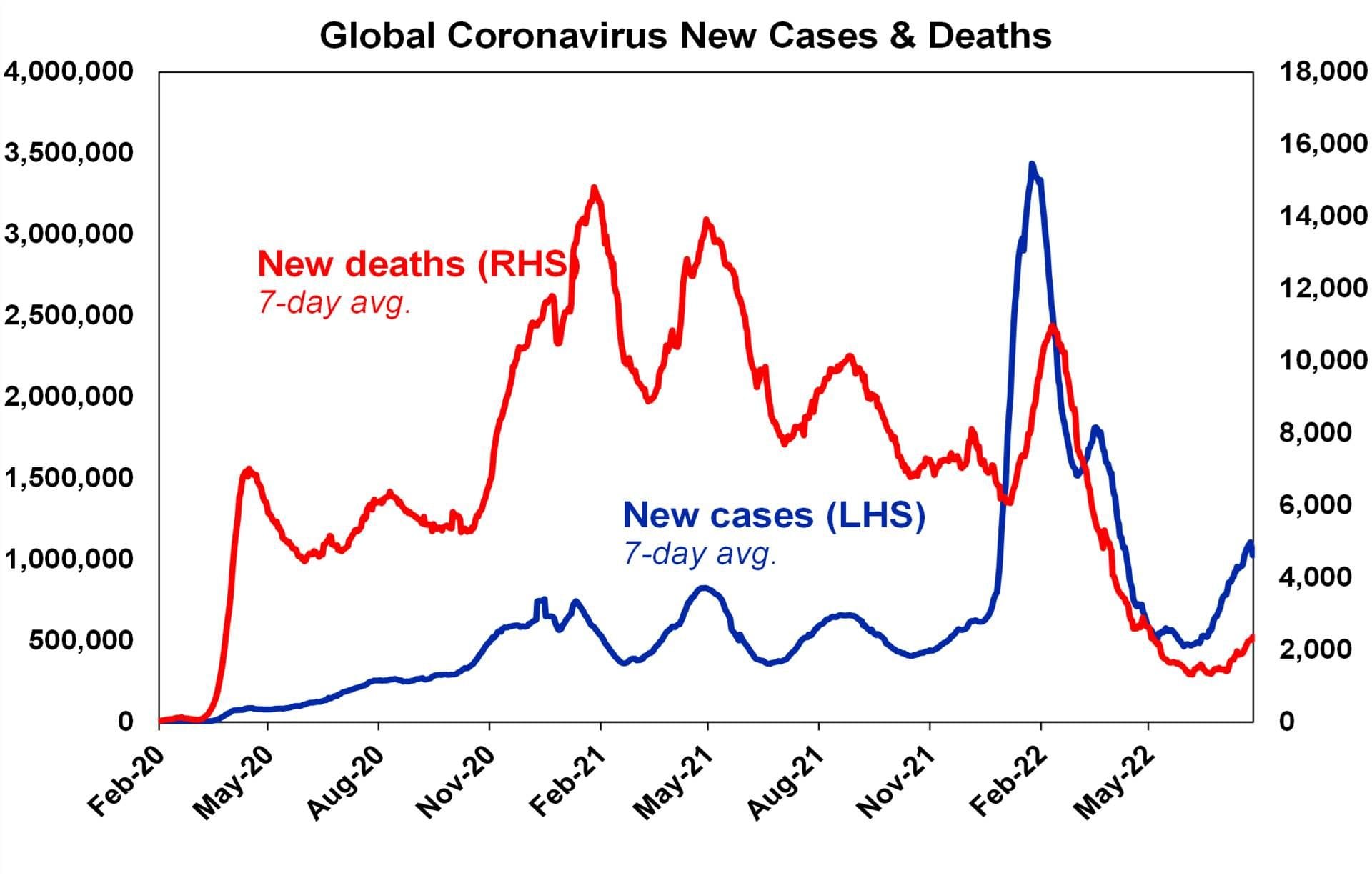

- New global Covid cases edged down a bit over the last week with Asia (notably Japan) up but Europe down. Hospitalisations and deaths generally remain subdued in most countries relative to cases compared to pre-Omicron waves.

Source: ourworldindata.org, AMP

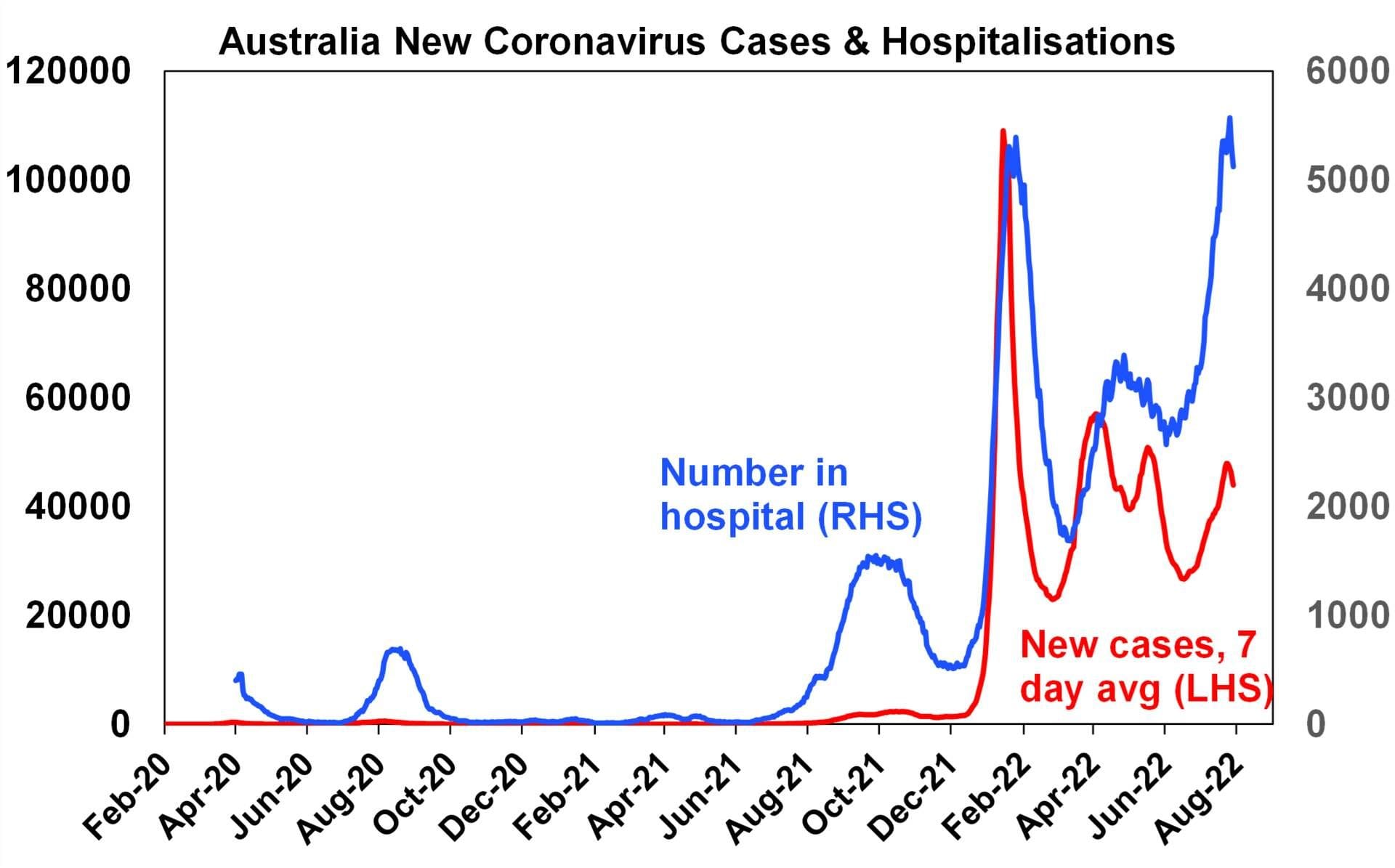

- Australia has seen hospitalisations rise above their January high – although hospitalisation and death rates remain subdued compared to pre-Omicron waves. Fortunately, there has been some tentative signs of a slowing in the last few days. South Africa’s experience with Omicron BA4/5 is continuing to augur well with cases, hospitalisations and deaths now low again after a spike in May. The proportion of the population to have had a 3rd dose is now at 55%, and 4th doses are now at 15%.

Source: covidlive.com.au, AMP

- While Monkeypox is causing increasing concern note that it is far harder to get than Covid, it can be treated and Smallpox vaccine is around 85% effective against it.

Economic activity trackers

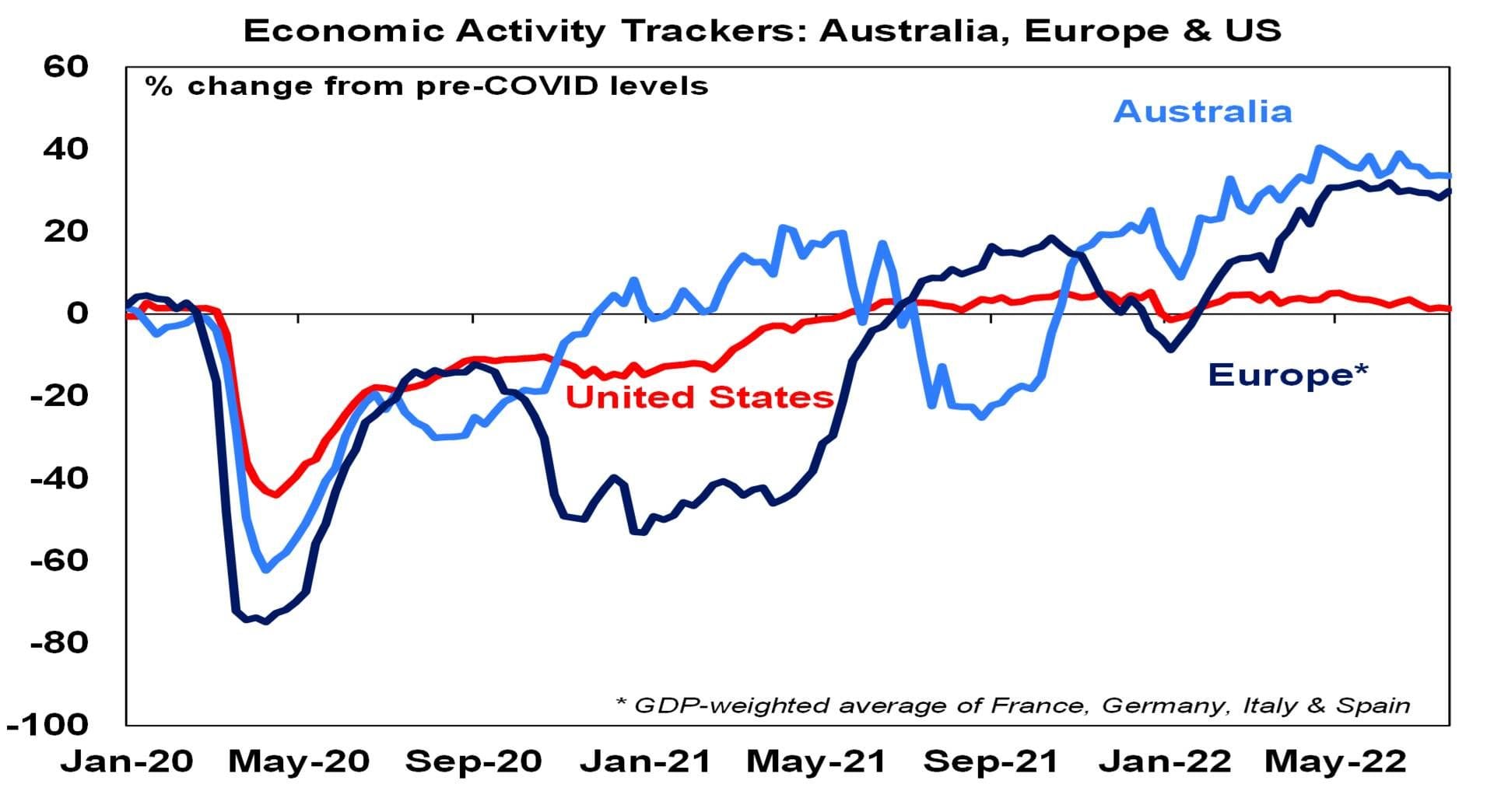

- The Australian Economic Activity Tracker was little changed again in the last week and is still showing a loss of momentum consistent with a slowdown in growth. The US Tracker was also little changed, but the European Tracker rose slightly.

Based on weekly data for eg job ads, restaurant bookings, confidence, mobility, credit & debit card transactions, retail foot traffic, hotel bookings. Source: AMP

Major global economic events and implications

- Apart from the fall in June quarter US GDP other US data was mixed with falls in home sales and consumer confidence, solid but slowing gains in home prices, strong durable goods orders and falls in unemployment claims albeit the trend remains up.

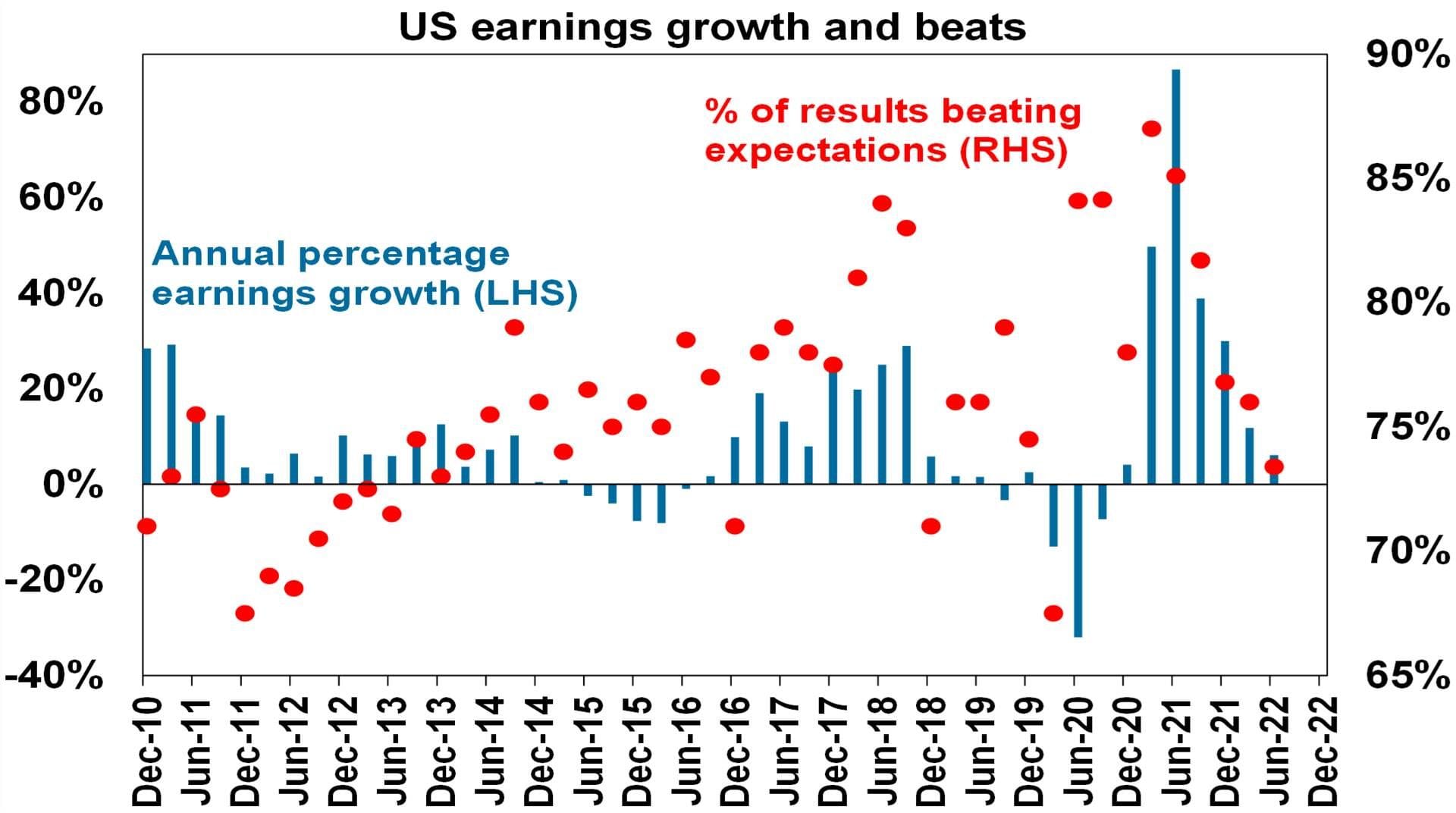

- 53% of US S&P 500 companies have now reported June quarter earnings with so far 73% ahead of expectations and earnings growth expectations for the quarter moving up from 5%yoy to 6.1%, and on track for around 9% based on the current rate of earnings surprise. Outlook comments have been mixed reflecting the uncertainty regarding the growth outlook. Earnings growth outside the US has actually been stronger.

Source: Bloomberg, AMP

- Looks like the Democrats may be getting a Build Back Better budget reconciliation – called the Inflation Reduction Act – back on track but don’t get too excited as it’s a fraction the size of the original $3.5trn plan. The main elements appear to be a 15% minimum corporate tax rate (which will make it easier for other counties to do the same), lower drug prices and clean energy subsidies. Over ten years it will raise more revenue than it spends, and it may help lower drug prices but its downward impact on inflation will likely be minor.

- Eurozone economic confidence fell again in July. Including business confidence it’s only fallen back to around pre-pandemic levels, but consumer confidence is at a record low.

- Japanese data was mixed with a sharp rise in industrial production for June but stable jobs data and a fall in retail sales.

Australian economic events and implications

- The Federal Treasurer’s statement on the economic outlook provided few surprises with economic growth revised down (but still a long way from recession) and inflation revised up to a peak of 7.75% in December and not expected to fall to target until 2024. This is similar to what markets have been assuming. The Treasurer is now acknowledging that the 2021-22 budget deficit will be far better than expected thanks to higher commodity prices and lower unemployment – recent data suggests it will be at least $30bn lower than forecast in March. But he also pointed to $30bn in extra spending pressure over the next 5 years. The statement appears aimed at resetting expectations lower and setting the scene for savings in the October Budget. Spending cuts would make the RBA’s job in controlling inflation easier.

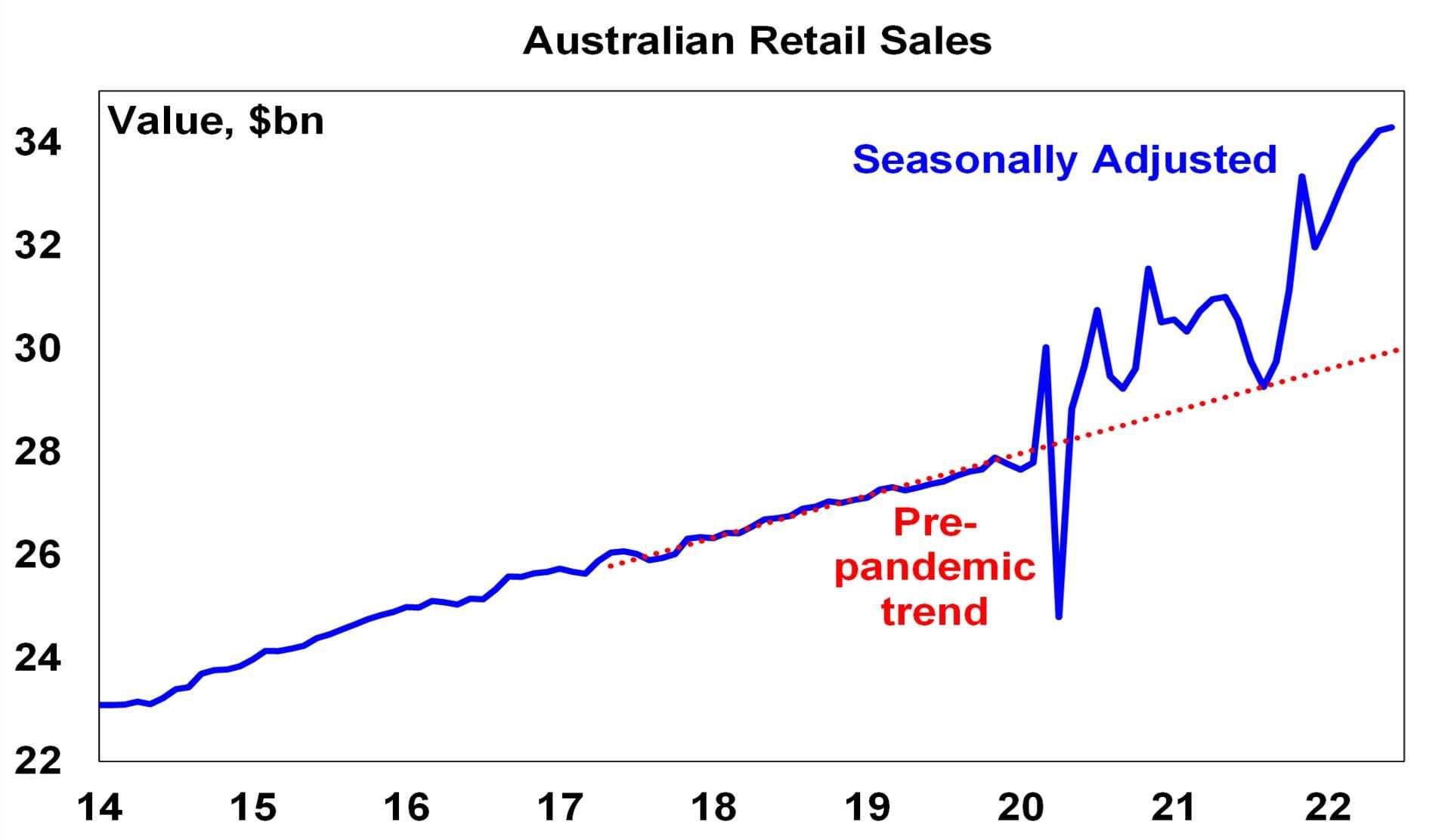

- Aust retail sales growth slowed to 0.2% in June, which would be negative after inflation. It looks like the pace of gains may be starting to slow reflecting the drag from cost of living pressures and rising mortgage rates.

Source: ABS, AMP

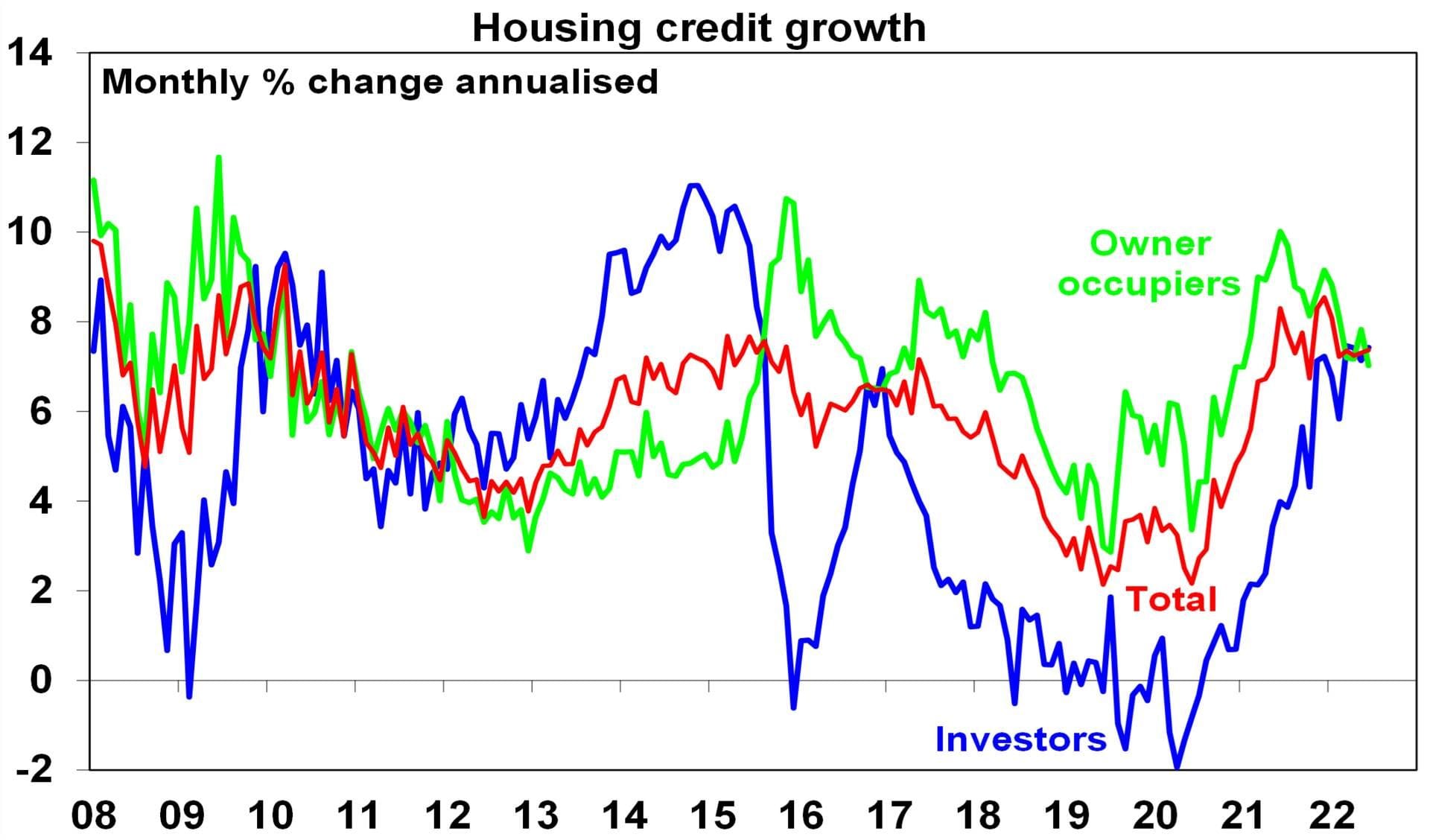

- Credit growth remained solid at 9.1%yoy in June. Business credit growth is still strong and housing credit growth remained solid. It’s likely to fall as the housing downturn impacts.

Source: RBA, AMP

- Another terms of trade surge in the June quarter. Export prices rose another 10% due to surging coal prices (+271%yoy) and gas prices (+105%yoy) whereas import prices rose only 4%qoq (largely due to higher petrol prices). The continuing surge in the terms of trade is good for national income and tax revenue – but can’t be assumed to last. (Fortunately, Treasury is not assuming that it will in its budget projections.)

What to watch over the next week?

- In the US, the main focus is likely to be on July jobs data to be released on Friday which is expected to show a further slowing in payroll growth to around 250,000, unemployment flat at 3.6% and wages growth slowing slightly to 5.1%yoy. June data for job openings (Tuesday) is likely to remain high but show some moderation and the ISM business indicators (Monday and Wednesday) for July are likely to slow further. US June quarter earnings reports will continue.

- China’s July Caixin business conditions PMIs (Monday and Wednesday) are likely to see a stalling in their improvement.

- In Australia, the RBA on Tuesday is expected to raise the cash rate by another 0.5% taking it to 1.85%, as part of an ongoing effort “to do what is necessary” to return inflation to target by slowing demand and ensuring that long term inflation expectations don’t rise. Fortunately, the slightly slower than expected inflation rate for the June quarter of 6.1%yoy likely removed the need for a further step up in the size of rate hikes to 0.75%. However, with the RBA still seeing the economy as resilient, the labour market coming in stronger than expected, inflation on its way to over 7% and the RBA viewing the cash rate as still well below its assessment of the neutral rate the RBA is expected to remain hawkish warning of further rate hikes ahead. The RBA’s Statement on Monetary Policy (Friday) is expected to lower its unemployment rate forecast for this year to 3.25% but revise down the growth outlook for the next year and revise up the inflation outlook to over 7%yoy for this year.

- Another 0.5% increase in the cash rate if passed on the mortgage holders as expected will add roughly another $150 to the monthly payment on a typical $500,000 mortgage which will take the total increase in monthly payments since May to around $500 a month.

- On the data front in Australia, expect CoreLogic home price data (Monday) for July to show a 1.5% fall with Sydney prices down by 2.3%, the Melbourne Institute’s Inflation Gauge for July (also Monday) to show a further pick up reflecting rises in energy prices, June building approvals and housing finance data (Tuesday) to show falls of -14% and -2% respectively, June quarter real retail sales (Wednesday) to rise 0.6% and the June trade surplus (Thursday) to fall back to $12.5bn.

Outlook for investment markets

- Shares remain at high risk of further falls in the months ahead as central banks continue to tighten to combat high inflation, the war in Ukraine continues and uncertainty about recession remains high. However, it is likely to see shares providing reasonable returns on a 12-month horizon as valuations have improved, global growth ultimately picks up again and inflationary pressures ease through next year allowing central banks to ease up on the monetary policy brakes.

- With bond yields looking like they have peaked for now short-term bond returns should improve.

- Unlisted commercial property may see some weakness in retail and office returns (as online retail activity remains well above pre-covid levels and office occupancy remains well below). Unlisted infrastructure is expected to see solid returns.

- Australian home prices are expected to fall 15 to 20% into the second half of next year as poor affordability & rising mortgage rates impact. Sydney and Melbourne prices are already falling aggressively, and falls are spreading to other cities.

- Cash and bank deposit returns remain low but are improving as RBA cash rate increases flow through.

- The $A is likely to remain volatile in the short term as global uncertainties persist. However, a rising trend in the $A is likely over the medium term as commodity prices ultimately remain in a super cycle bull market.

Source: AMP CAPITAL ‘Weekly Market Update’

AMP Capital Investors Limited and AMP Capital Funds Management Limited Disclaimer