- Share markets had another volatile week with worries about central bank rate hikes and Chinese covid lockdowns depressing global growth but generally good earnings news. Despite a fall back to March lows US shares managed to find support there and rose slightly for the week but European, Japanese, Chinese and Australian shares fell. The fall in Australian shares was led by sharp falls in IT, resources and health stocks. Global bond yields pulled back a bit from recent highs but they rose further in Australia. Oil prices rose, but metal and iron ore prices fell albeit they remain very high. The $A also fell as the $US continued to rise.

- Despite the pull back, the Australian share market remains a relative outperformer – thanks to its high exposure to resources shares and low exposure to tech stocks – being virtually flat year to date compared to falls of 10% in US shares, 12% in European shares and 7% in Japanese shares. While the pullback in commodity prices from overbought levels in the short term may weigh, Australian shares are likely to continue to outperform over the medium term as the commodity super cycle continues and as higher bond yields compared to the pre-covid era weigh on tech stocks.

- The base case for investment markets remains that US, global and Australian recession will be avoided over the next 18 months at least and this will enable share markets to have reasonable returns on a 12-month horizon. However, the past week provided a reminder that short term risks around inflation, rate hikes, the war in Ukraine and Chinese growth remain high which of course saw more volatility in share markets with US shares falling back to their March low and Nasdaq and Chinese shares making a new low.

- While investment markets seem to have moved on from worrying too much about the war in Ukraine the risk of escalation remains significant with: Russia cutting Poland and Bulgaria off from its gas as part of a strategy to put more pressure on western Europe and enforce its insistence they pay for gas in roubles; Russia appearing to be trying to destabilise Moldova (via its allies in Transnistria); and Sweden and Finland seriously considering joining NATO which will add to Russian annoyance. Russia is still unlikely to cut gas off from Germany because it needs the revenue, but it may. And in the meantime, Europe appears to be moving towards a ban on Russian oil imports which could put more pressure on oil prices. A Russian war with NATO remains unlikely (given both have nuclear weapons) but signs of an escalation in the war and more restrictions on Russian energy exports could still unnerve investment markets.

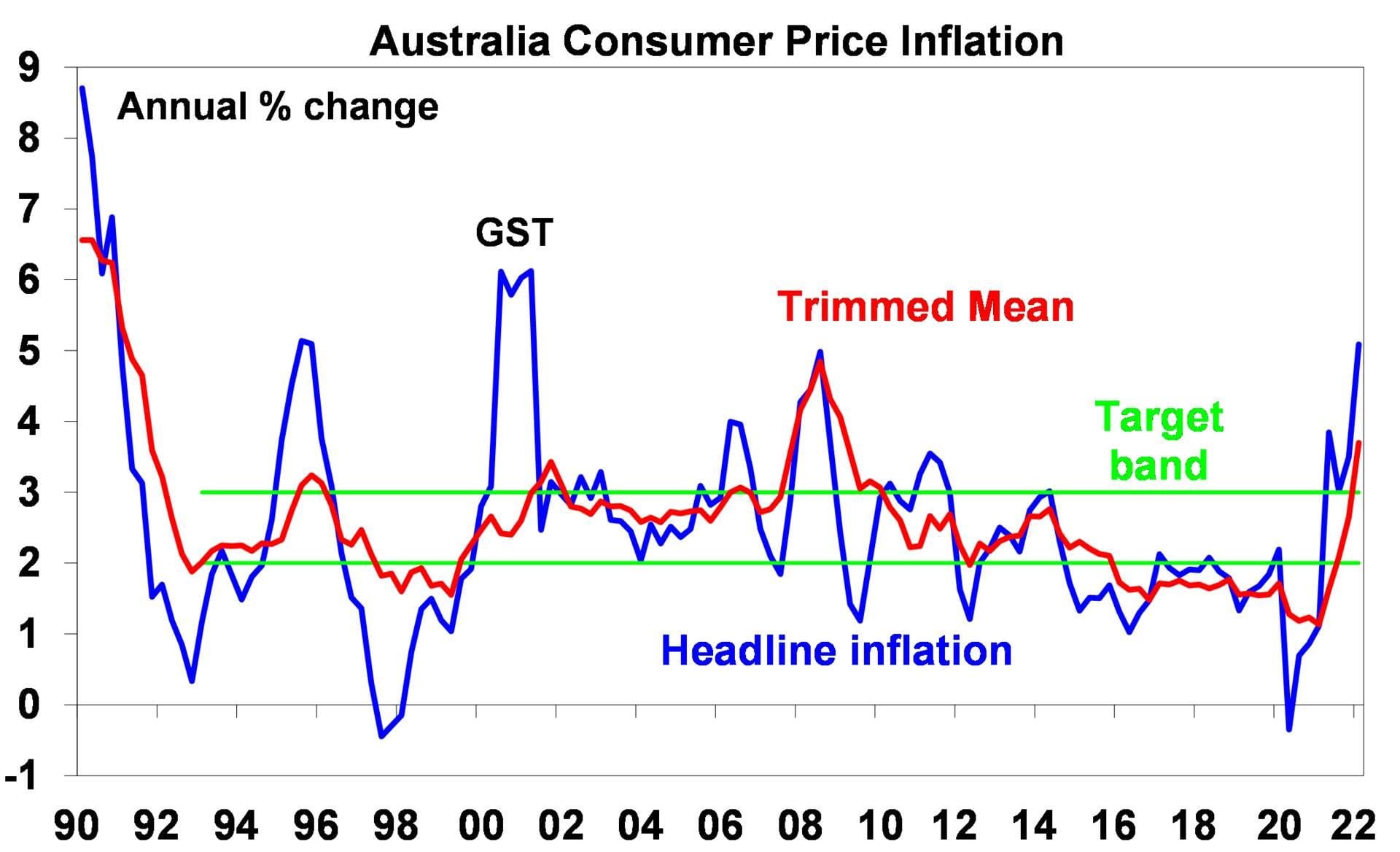

- Australian inflation blowout sets the scene for the RBA to start rate hikes at its May meeting. While a bad inflation report was expected for the March quarter it turned out far worse than expected:

- headline CPI inflation rose to 5.1%yoy which is the highest since the GST – and if the tax driven boost from the GST is excluded it’s the equal highest inflation rate since 1990;

- the RBA’s preferred measure of underlying inflation – the “trimmed mean” – rose to 3.7%yoy; and

- consistent with this the rise in inflation was broad based and more than just due to the 11%qoq rise in petrol prices with fruit and vegetables, meat and seafoods, soft drinks & juices, pets and pet products, new dwellings, tertiary education and non-durable household products like toilet paper seeing price rises of 5 to 7%qoq.

- While Australian inflation is still below the 8.5% in the US and the circa 7% rates in Europe, the UK, Canada and NZ, petrol prices will likely fall back this quarter, in the near-term underlying inflation will likely push higher with e.g. Coles warning of further significant supermarket inflation ahead.

Source: ABS, AMP

- While much of the surge in inflation owes to pandemic distortions to global supply and goods demand made worse by the war in Ukraine and the recent floods, the RBA has to act for two reasons. First, having a near zero cash rate when unemployment is 4% and inflation is over 5% makes no sense. Second, the experience from the late 1960s and 1970s tells us the longer high inflation persists the more inflation expectations will rise making it even harder to get inflation back down again without engineering a recession. Waiting till after the release of wages data and till after election would have been nice but the stronger broad based surge inflation means the RBA no longer has time on its side and should move now and do so decisively. As a result expect the RBA to hike rates on Tuesday and to do so by 0.4%. While it’s a close call as to whether the first hike is 0.15% (taking the cash rate to 0.25%) or 0.4% (taking it to 0.5%) as the RBA may prefer a cautious approach initially and to not upset the Government too much given the election it’s likely that a 0.15% hike won’t send a particularly strong signal in terms of its resolve to keep inflation expectations down and so it’s leaning towards a 0.4% move on Tuesday. Expect another 0.25% hike in June and now see the cash rate rising to 1.5% by year end.

- Moving earlier and faster initially should allow the RBA to slow the pace of rate hikes next year. And through next year the combination of fixed rate borrowers seeing a doubling in their interest rate as their fixed terms come to an end and falling home prices exerting a negative wealth effect will start to do some of the RBA’s work for it.

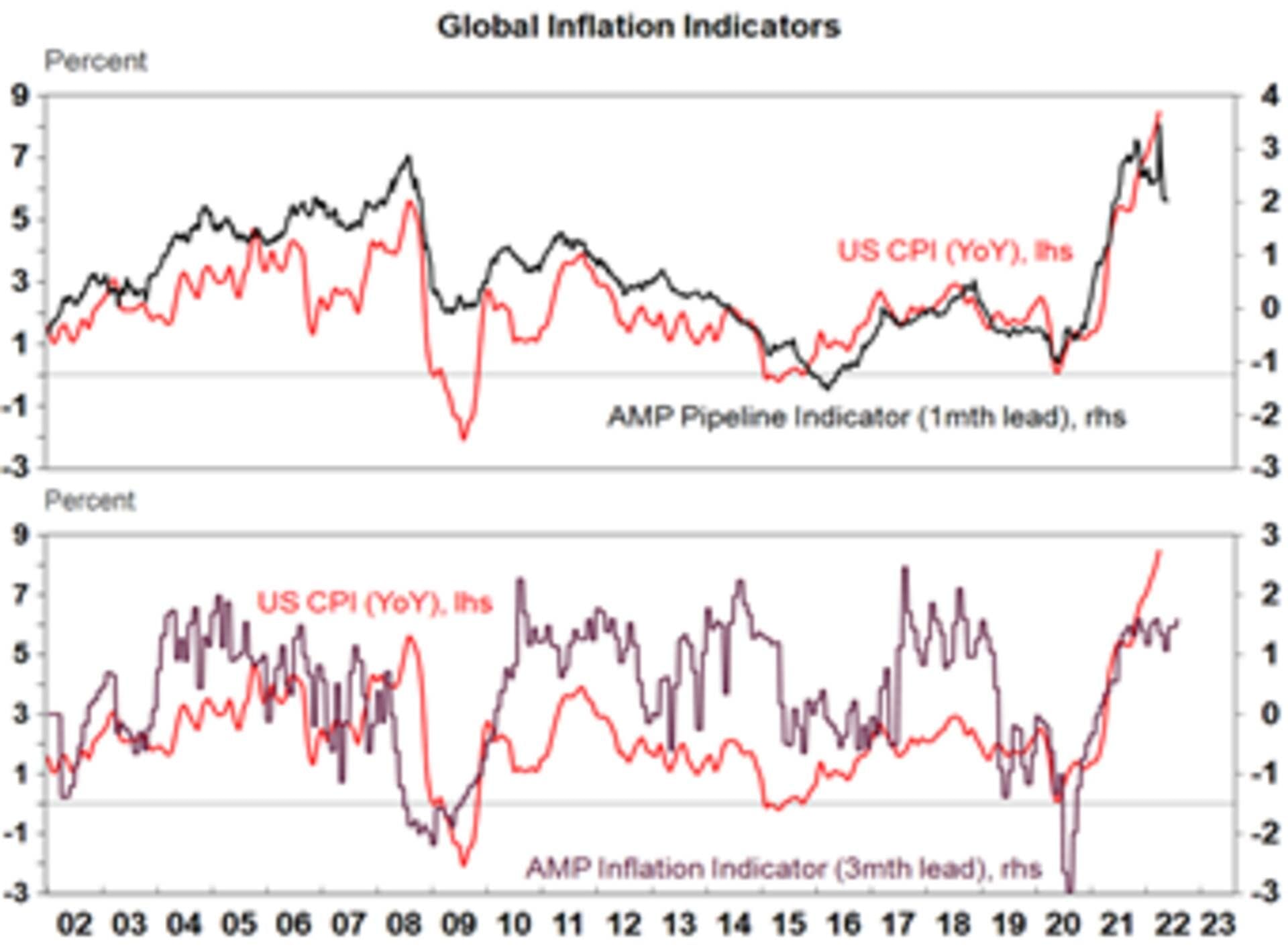

- The good news for central banks is that inflationary pressures may be peaking – as evident in the US Pipeline Inflation Indicator which is continuing to show signs of having peaked. Inflation rates will still be way too high which will keep the Fed and other central banks tightening in the short term. And annual inflation in Australia probably won’t peak until the September quarter. But a peaking in inflation pressures may allow some slowing in the pace of rate hikes from later this year and through next year.

The Inflation Pipeline Indicators is based on commodity prices, shipping rates and PMI price components. Source: Macrobond, AMP

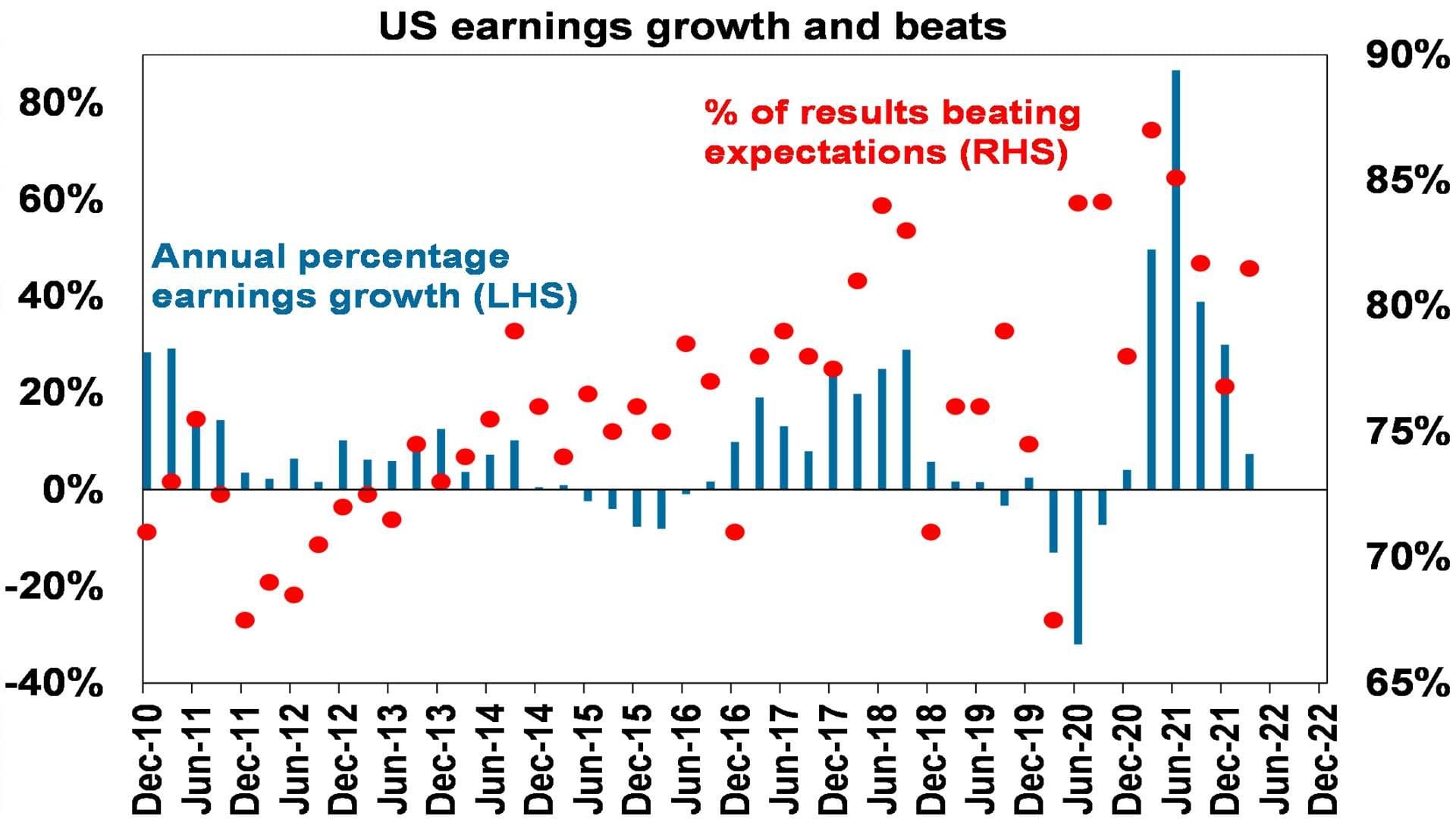

- Two things went well for investment markets in the last week. First, US March quarter earnings reports are continuing to surprise on the upside and earnings look on track to rise around 11%yoy which is up from initial expectation for a 4.3%yoy gain. And earnings growth in Europe and Asia is averaging slightly faster.

- Second, centrist Emmanuel Macron was returned as French president with 58.5% of the vote which was around 2% ahead of the more recent polls in the second-round runoff with far-right Marine Le Pen. This is positive for continued European integration and European resolve against Russia and a continuation of President Macron’s French economic reform program, depending on June parliamentary elections. Which in turn means it’s a positive outcome for European assets – all things being equal which of course they weren’t in the last week.

|