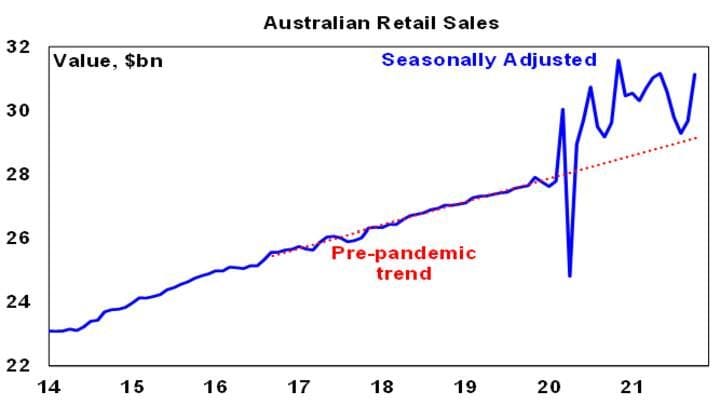

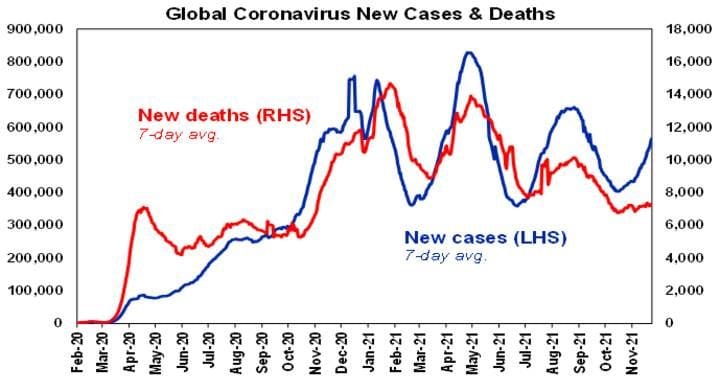

- Global coronavirus cases are continuing to rise globally, but its noteworthy that deaths are so far more subdued.

Source: ourworldindata.org, AMP Capital

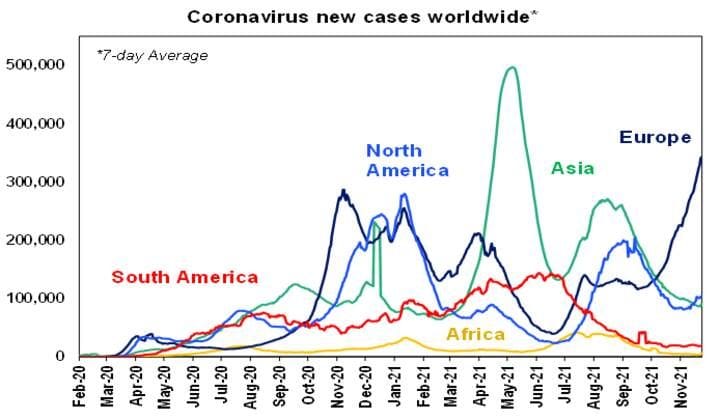

- The surge is mainly being driven by Europe where new cases are at record levels – notably in Germany, Austria, the Netherlands, Denmark, Belgium and Finland but France, Italy, Spain and the UK have also started to pick up. The US is also starting to head higher as well.

Source: ourworldindata.org, AMP Capital

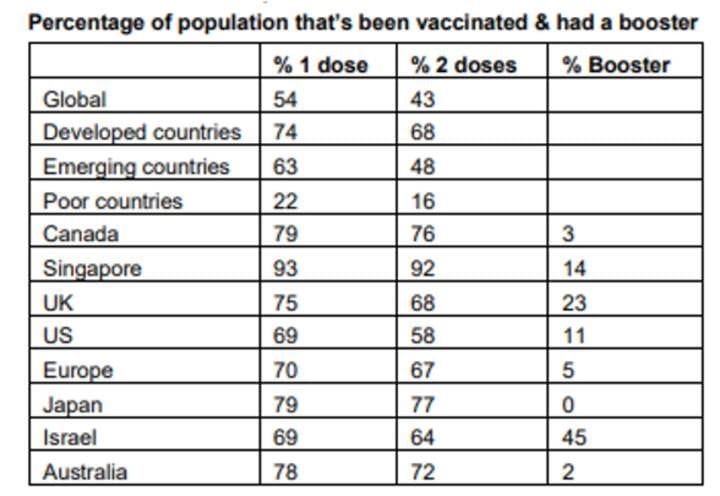

- The surge in new cases reflects a combination of the earlier almost complete removal of restrictions, the onset of cold weather, stalling vaccination rates at or below 70% of the whole population, fading efficacy against new infection and a slow start to boosters. Israel in the September quarter and more recently Singapore have seen the same but managed to control it with booster shots and only some restrictions.

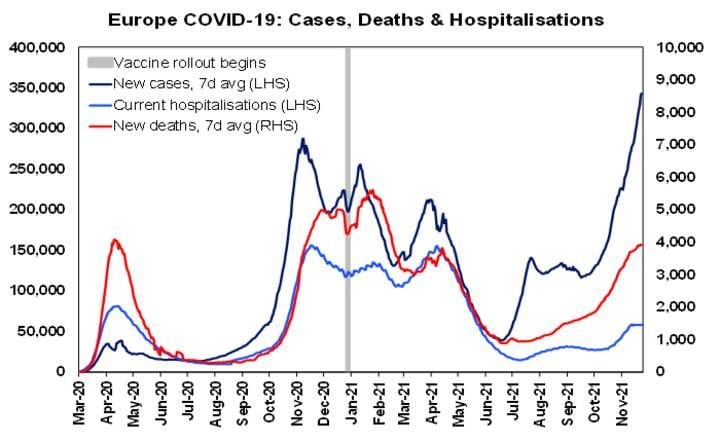

- While the latest coronavirus wave poses a significant threat to the economic outlook the key remains whether vaccinations are successful in keeping hospitalisations down such that hospital systems can cope so hard long lockdowns can mostly be avoided. This also remains the key issue in relation to the new Omicron variant – but it’s too early to tell at present what impact it will have on vaccine effectiveness. So far hospitalisation and death rates in Europe remain subdued relative to the wave a year ago. But with big parts of the population still unvaccinated in Europe and the US there is still a risk that many could get sick at once overwhelming hospital systems. The only way to avoid that is to get vaccination rates to very high levels, quickly roll out booster shots to those whose last shot was 5 months or so ago and only remove restrictions gradually. Singapore is probably the best example of how to handle this – 92% of its population is fully vaccinated and booster shots are being rapidly rolled out and it’s seeing cases trend down again.

Source: ourworldindata.org, AMP Capital

- 68% of people in developed countries are fully vaccinated, 48% in emerging countries but its only 16% in poor countries. A key problem though is that some advanced countries (notably the US and Europe) have seen vaccination programs stall at low levels leaving them vulnerable to this latest wave as we are now seeing. An even bigger risk is that poor countries are lowly vaccinated which increases the risk of mutations that are more transmissible and deadly. Whether Omicron poses a major threat or not, its arrival highlights the high risk on this front. Only 24% of South Africans are fully vaccinated and vaccine suppliers had been asked to pull back on new deliveries due to reduced demand. The rest of Africa is only 7% vaccinated. It all highlights the need for the whole world to be vaccinated as fast as possible to head off mutations.

Source: ourworldindata.org, AMP Capital

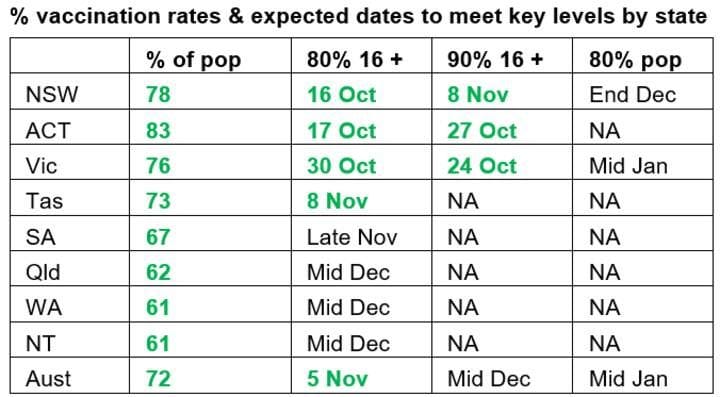

- Australia at 72% fully vaccinated (and that’s before Queensland and WA have met their targets) is well above the developed country average. On current trends Australia will average 90% of the adult population fully vaccinated by mid-December and 80% of the whole population around mid-January. New coronavirus scares and the likely approval of vaccines for 5 to 11-year olds should take the percentage of the population fully vaccinated well beyond 80%.

Source: covid19data.com.au, AMP Capital

- A resurgence in new cases in Australia looks almost inevitable given the experience of Israel, the UK, the US, Europe, Singapore, etc. Australia’s relatively high vaccination rate have helped keep hospitalisation and deaths subdued relative to last years’ experience through the recent wave (see the next chart) and the fully vaccinated remain a very small share of new cases (just 8% in NSW). But as seen in Israel and Singapore if new cases rise too quickly it can still threaten to overwhelm hospital systems. So the key to minimise the risk of a surge in new cases necessitating new lockdowns is to get vaccination rates up to very high levels (90% plus), rapidly roll out booster shots to those whose last dose was 5 months or so ago and maintain social distancing requirements and aids such as QR check ins. The risk posed by new variants (as the new South African variant may demonstrate) suggests a strong case also to go very slowly and cautiously in reopening the international border.

|