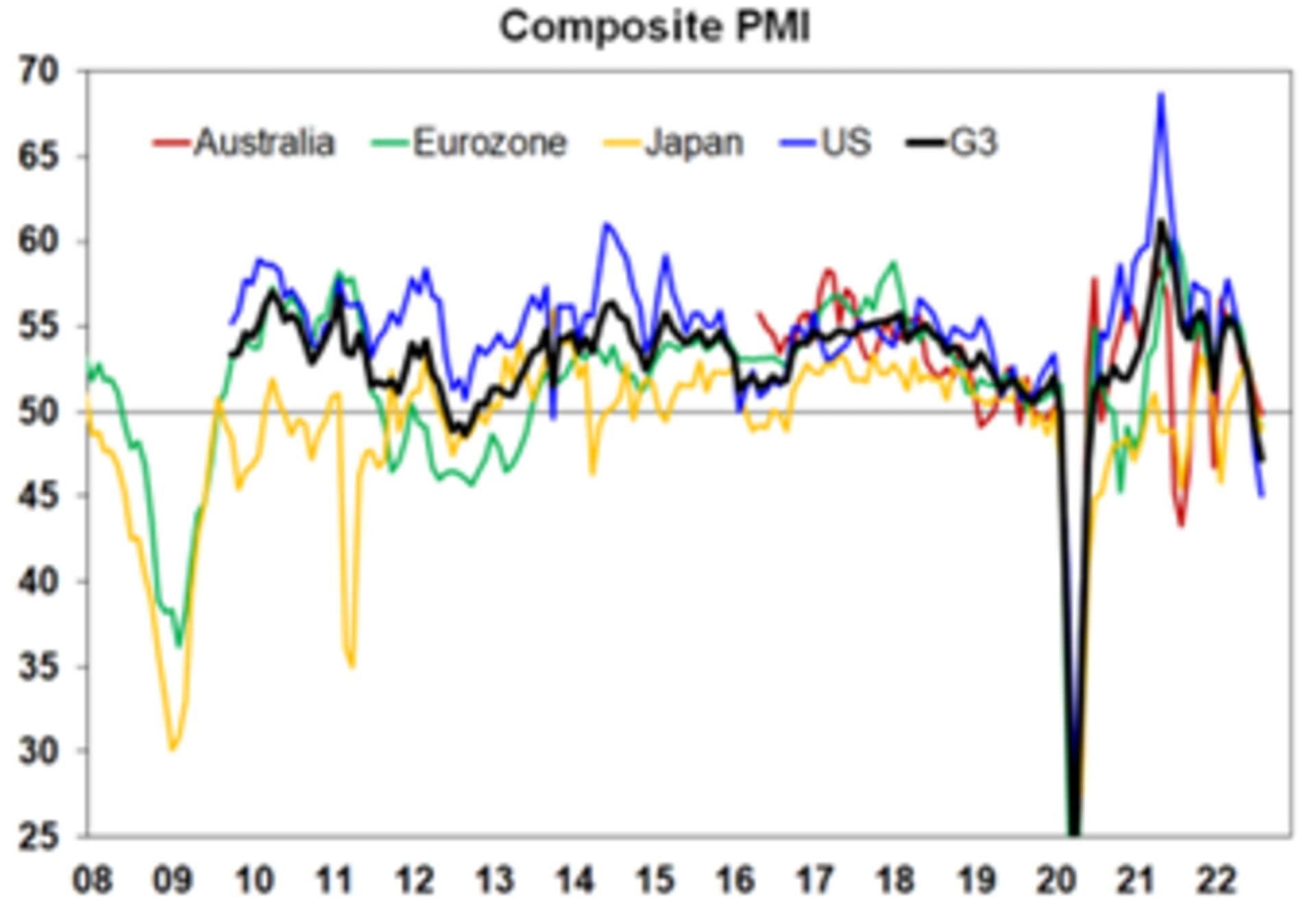

- Global PMI business conditions for August showed that the major countries composite PMI indices are now below 50, which means a contraction in activity (see the chart below). The US manufacturing PMI was down 0.9pts to an index of 51.3, while services was worse, down by 3.2ppts to an index of 44.1. The Eurozone manufacturing PMI fell 0.1pts to 49.7 and services was worse, down by 1pt, although services activity is still positive, with the index at 50.2. The Eurozone activity data is holding up better than expected (especially for services), given very high energy costs. Eurozone activity could be holding up thanks to summer tourism, although this will start to fade in coming months.

Source: S&P, AMP

- The Australian composite PMI fell into contraction in August, with the index declining to 49.8. Manufacturing was down to 54.5 (from 55.7), while services activity went negative to 49.6 (from 50.9) as activity slows from higher interest rates. The PMI data is consistent with other signs of slowing global growth in 2H2022, like falling Taiwan and Korean export data, but not bad enough to signal a global recession. Expect global growth of 2.6% in 2022 – well below expectations of 4% growth at the beginning of the year and below the historical average of 3%pa.

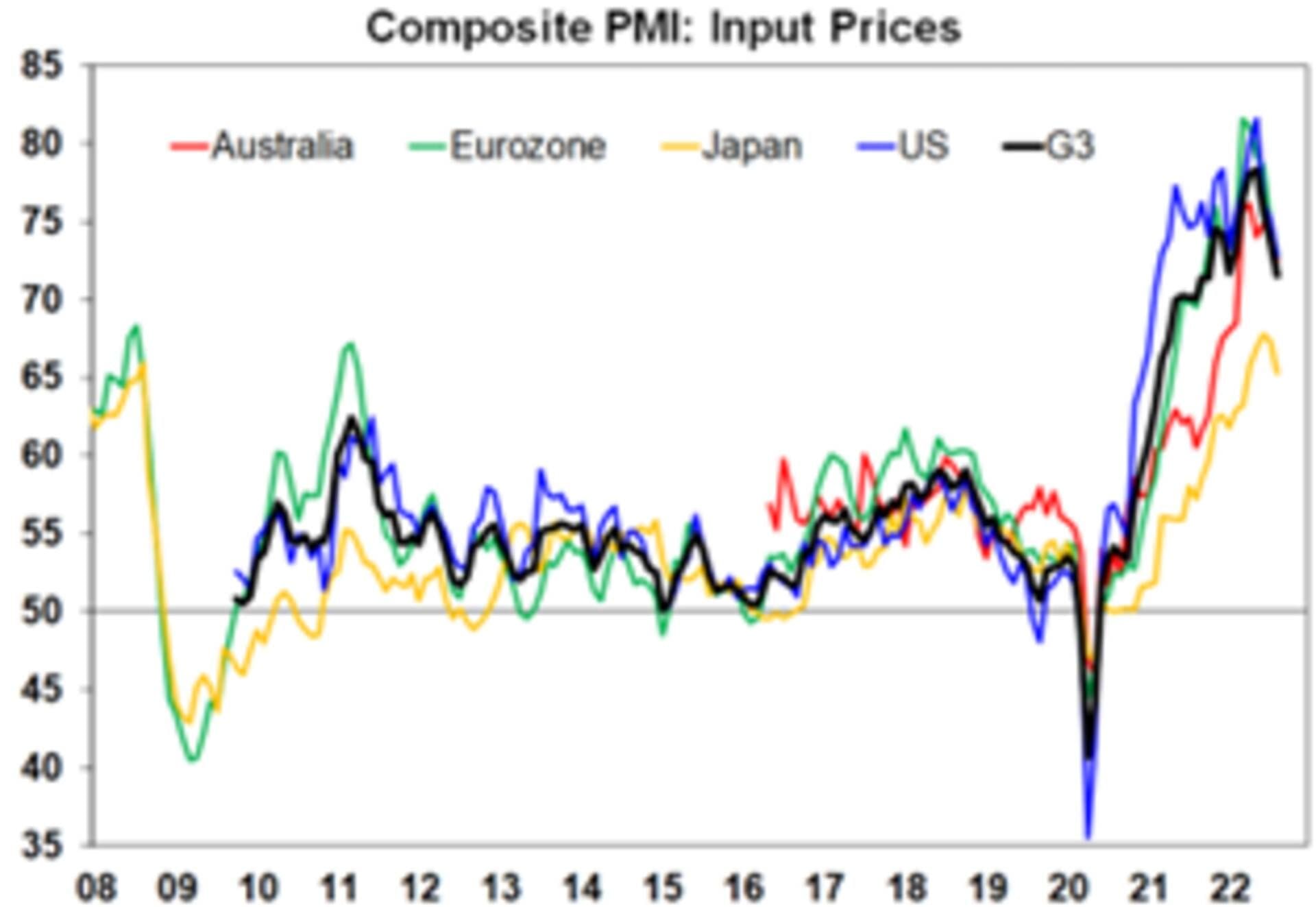

- The components of the PMI’s showed that input and output prices continued to decline and delivery times improved which are consistent with an easing in supply chain disruptions, which is why the inflation tracker also continues to decline. But backlogs of work and new orders are also declining, which shows a weakening in demand.

Source: S&P, AMP

- US data this week included an update on regional manufacturing activity, with the Richmond Fed manufacturing index moving into contraction at an index of -8 (from 0 last month) and the Kansas City Fed manufacturing index was down 10pts to 3, which means further downside to the national manufacturing PMI in coming months. Housing data continues to soften, with new home sales down by 12.6% in July (well below expectation), pending home sales were down by 1% in July (although this was better than expected) and MBA mortgage applications were down 0.5% over the week to 19 August. July US durable goods were flat in July, below expectations but the core data (which excludes transport) was better, which is good for third quarter GDP. US second quarter GDP was revised up 0.3 percentage points to a -0.6% annualised fall, so there is still a chance that the recession in 1H2022 is revised away! Initial jobless claims were 243K over the week to 20 August, below last week’s 250K, which shows that the labour market remains tight. Personal spending rose by only 0.1% in July (below expectations of 0.5%), a sign of a weakening consumer. The core PCE deflator, another inflation measure rose by a smaller than expected 0.1%, with annual growth at 4.6%, while the headline deflator actually fell over the month by 0.1% or 6.3% year-on-year. This is another sign that inflation has peaked in the US. The final University of Michigan consumer sentiment reading was revised up for August to 58.2 (from an initial reading of 55.1), although is still around its lows. And the 5-10 year inflation expectations index declined to 2.9% in August, from an initial read of 3%.

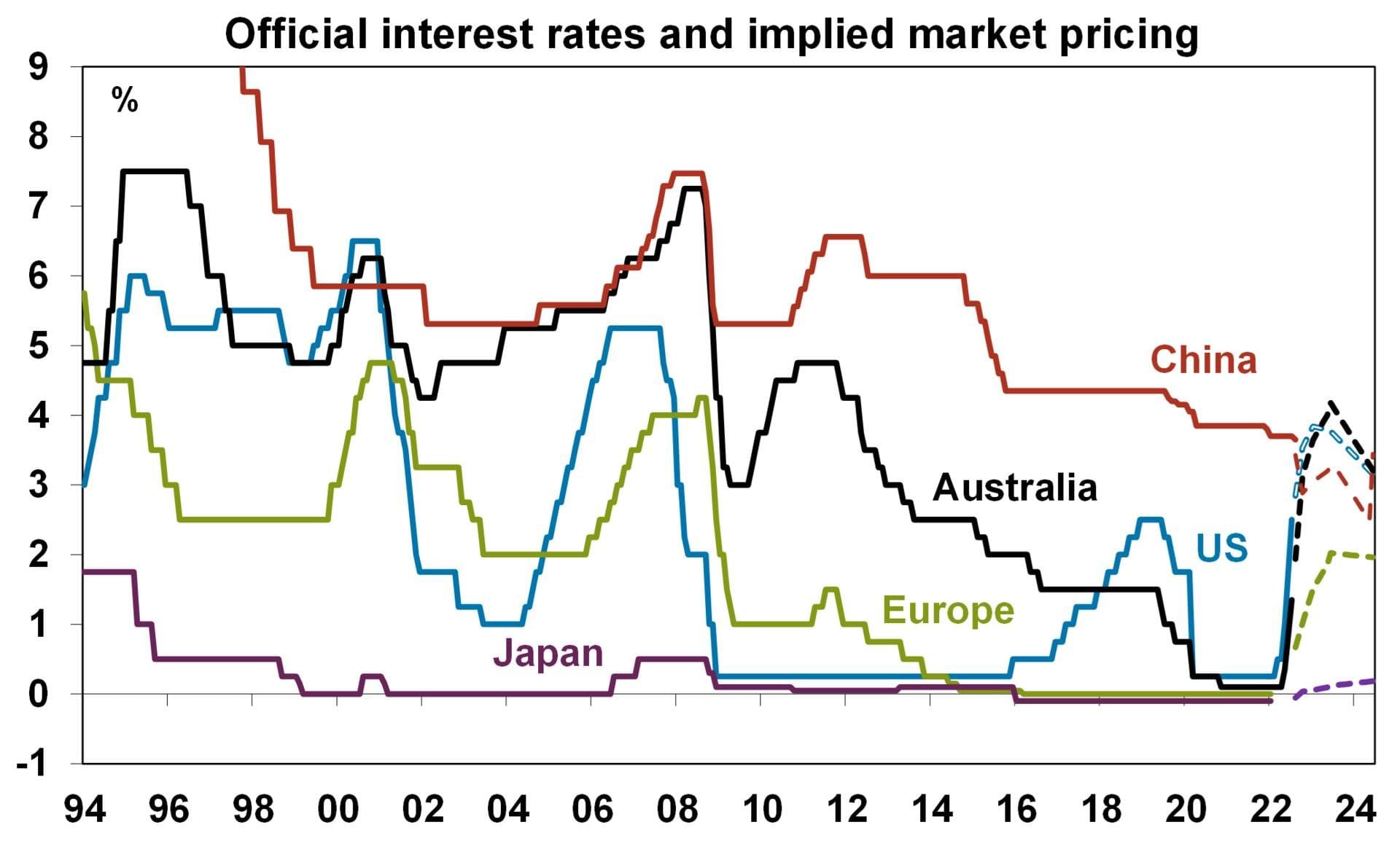

- The People’s Bank of China cut the one and five-year loan prime rates on Monday to 3.65% (from 3.7%) and 4.3% (from 4.45%) after reducing the rate of the medium-term lending facility last week.

Source: Bloomberg, AMP

- China remains one of the few economies where interest rates are still being cut rather than hiked (see the chart below).

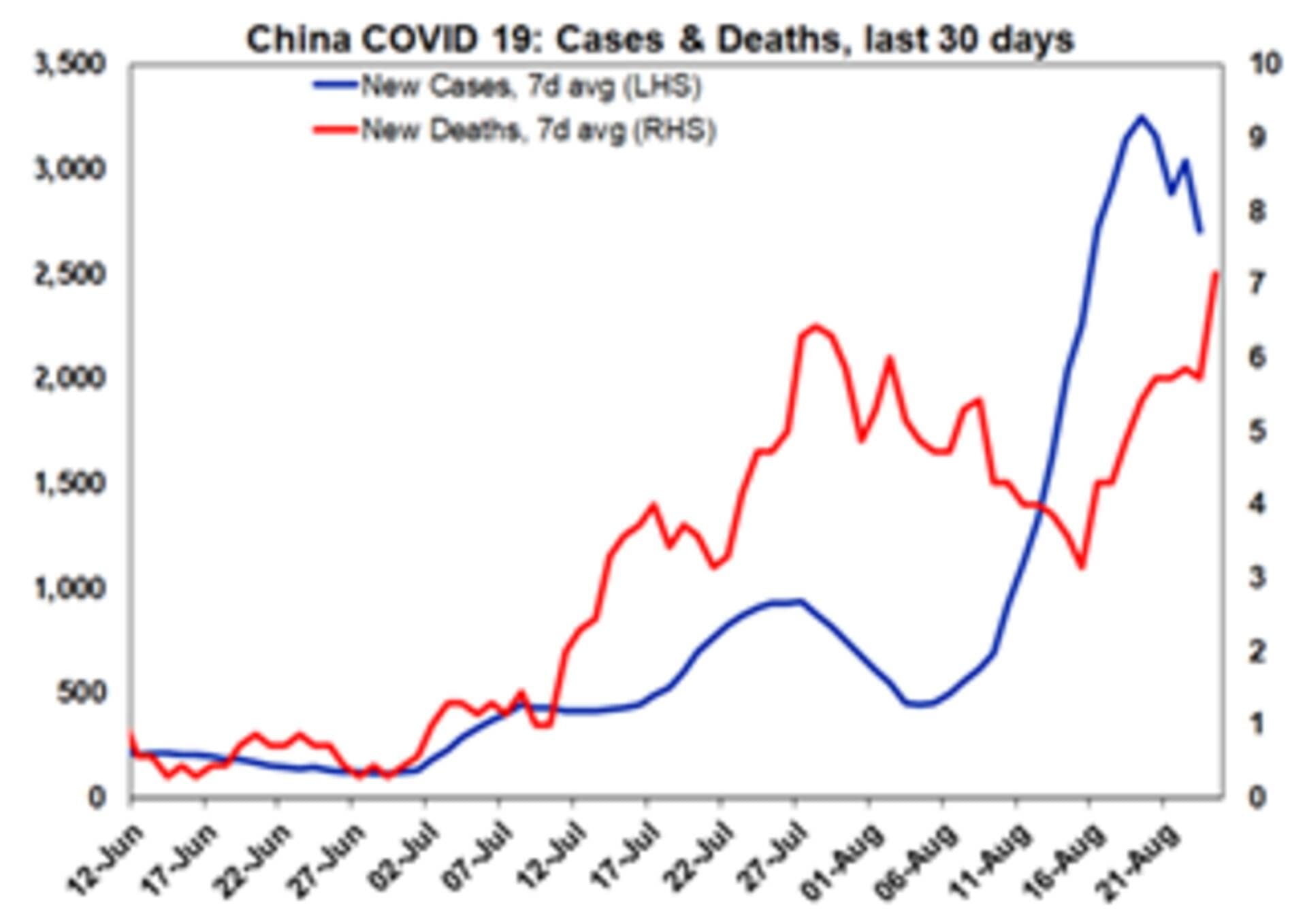

- China’s State Council also announced a 19-point stimulus package worth $146bn USD (under 1% of GDP) to boost economic growth, as China is facing many concurrent issues including drought, power shortages, property crisis and COVID-related restrictions – Cases however are rolling over (see the chart below), which could help restrictions.

Source: ourworldindata.ord, AMP

- Chinese GDP growth is likely to disappoint this year at under 3%, well below the 5-6% rates assumed at the beginning of the year and 4% assumed after the COVID outbreak.

- In Eurozone, consumer confidence actually ticked up in August by 2.1pts to -24.9 although sentiment is still extremely negative near its July all time lows (see the chart below).

- The German IFO business climate survey was down 0.2 percentage points to 88.5, better than expected but still low relative to its historical average.

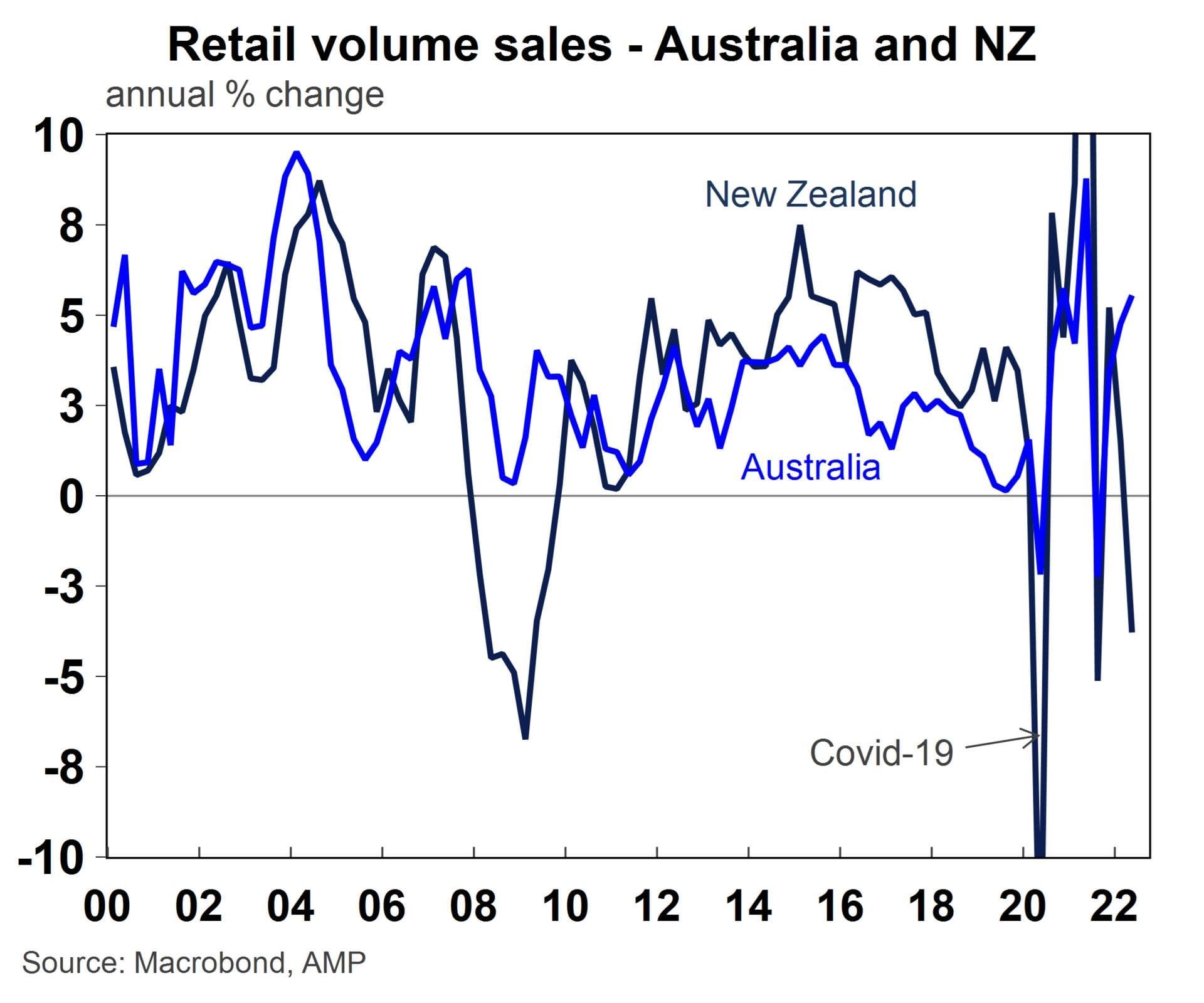

- In New Zealand, retail sales volumes fell by 2.3% in the June quarter, after also declining in the March quarter and missing expectations of a rise in spending. Weakness was concentrated in furniture, hardware and electronic goods which reflects the start of consumer spending weakness related to higher interest rates.

|