Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

Weekly Market Update – 19th November 2021

|

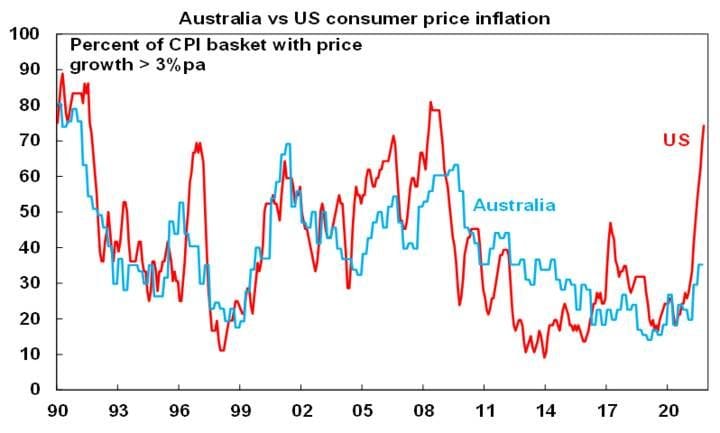

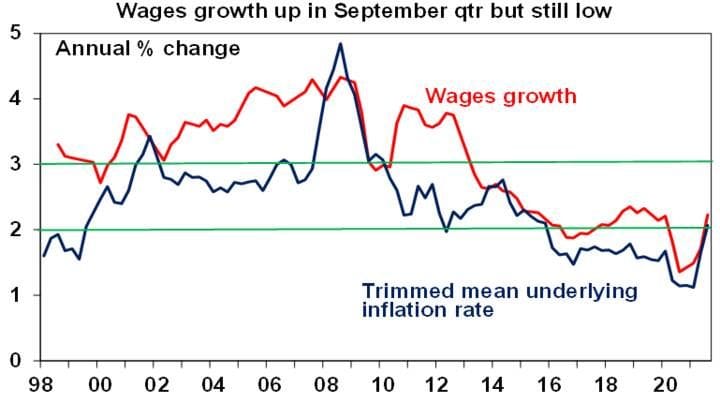

Source: Bloomberg, ABS, AMP Capital

|

|

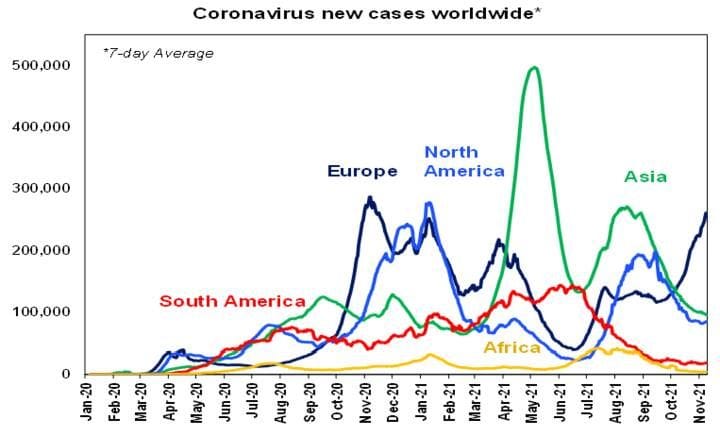

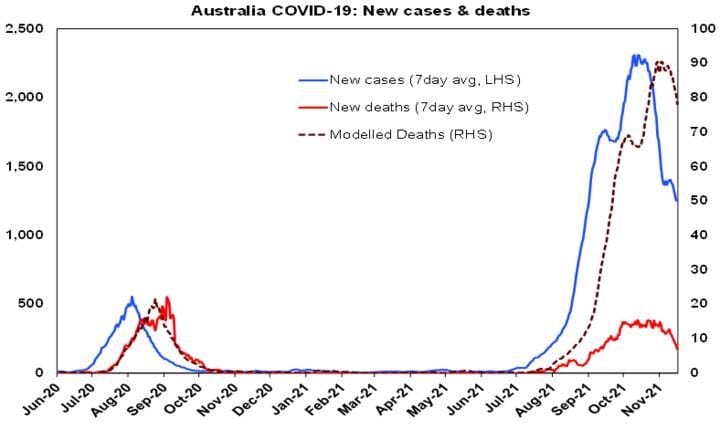

Source: ourworldindata.org, AMP Capital

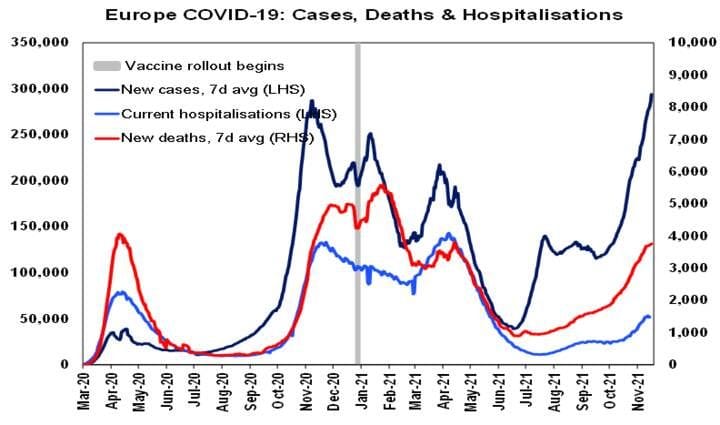

Source: ourworldindata.org, AMP Capital

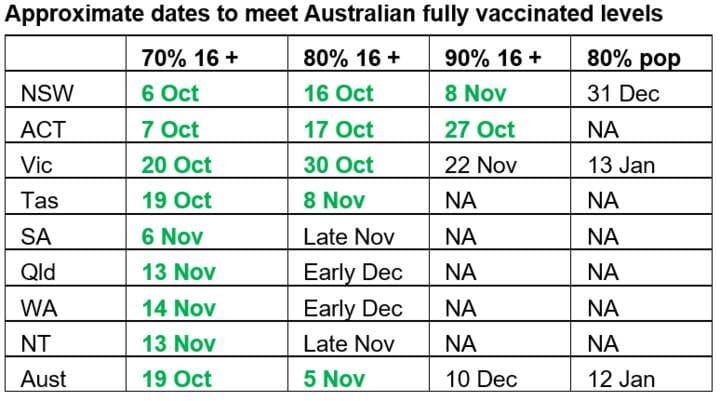

Source: covid19data.com.au, AMP Capital

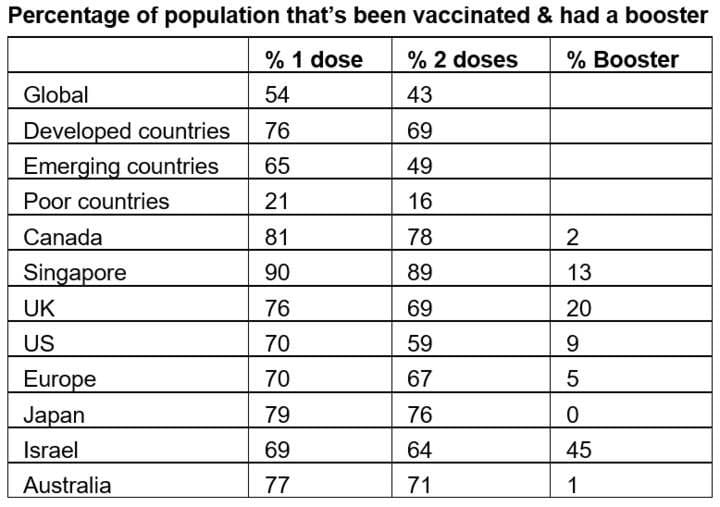

Source: ourworldindata.org, AMP Capital |

|

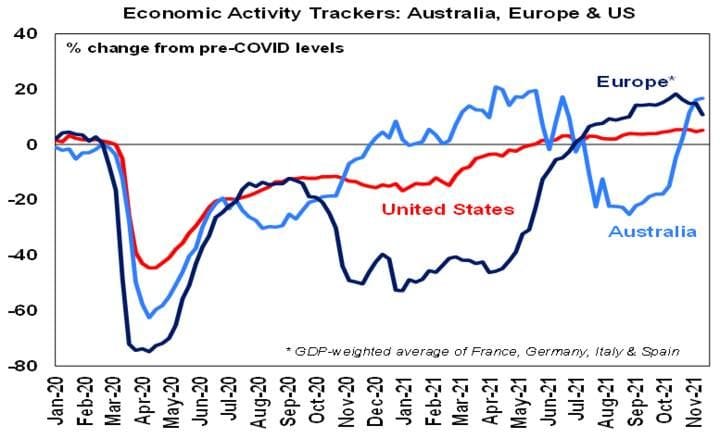

Based on weekly data for eg job ads, restaurant bookings, confidence, mobility, credit & debit card transactions, retail foot traffic, hotel bookings. Source: AMP Capital |

|

Source: Bloomberg, AMP Capital

|

|

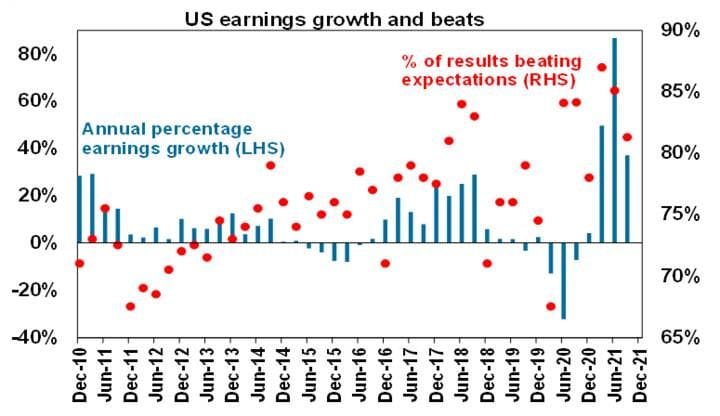

Source: ABS, AMP Capital

|

|

|

|

Source: AMP CAPITAL ‘Weekly Market Update’ AMP Capital Investors Limited and AMP Capital Funds Management Limited Disclaimer |