Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

Weekly Market Update – 18th August 2017

Investment markets and key developments over the past week

- Share markets were mixed over the last week with a rebound early on as North Korea decided against shooting a missile towards Guam but renewed mayhem around President Trump and a terror attack in Barcelona weighing later in the week. US shares fell 0.6% and Japanese shares fell 1.3%, but Eurozone shares rose 1.2% (after losing 2.6% the week before), Chinese shares rose 2.1% and Australian shares rose 0.9%. Bond yields were flat to slightly up, commodity prices were mixed with oil and gold down but metals and iron ore up and the A$ was up slightly.

- Political mayhem continues in the US. So far it’s unlikely to impact the GOP’s tax reform agenda but the risks are rising. While President Trump had a bad week back in May, it seems like he is having one bad week after another lately. While the war of words between North Korea and the US receded over the last week (for now), the mayhem around President Trump seems to be going from bad to worse with the disbanding of two business councils as US business leaders resigned in protest over Mr Trump’s response to racist violence in Charlottesville and rumours that top economic adviser Gary Cohn may resign too. This is clearly all disconcerting and highlights the divisions in the US that appear to be widening.Next month the political noise in the US will escalate further with the need to pass a 2017-18 budget, approve funding to avoid a government shutdown and raise the debt ceiling by late September ahead of moving on to tax reform. However, while there will likely be another bout of brinkmanship that could cause volatility in financial markets, ultimately a last minute solution remains most likely as the 2013 experience highlighted that it’s in neither party’s interest to allow a shutdown and neither want a debt default. While it all looks messy it’s doubtful that the disbanding of the business councils has reduced the chance of tax reform. Business groups will still lobby for it and it’s the Republicans in Congress who are driving the agenda now (not the President) and they want a win on taxes ahead of the November 2018 mid-term elections. The removal of alt-right adviser Stephen Bannon may help steady the White House, but the risks will grow if Mr Trump can’t start to heal the divisions he is creating (including with Congressional Republicans).

- Meanwhile, President Trump provided no surprises in announcing a directive to consider whether Chinese practices around US intellectual property should be formally investigated. This is process oriented and will have a long way to go with plenty of opportunities for win/win compromises along the way. Mr Trump is a long way from the imposition of huge tariffs ‘from day one’ that was talked about in his election campaign.

- Political uncertainty on the rise in Australia. While the key issues seemingly troubling Australian politicians at present – marriage equality and the “foreigners stealing Aussie politicians’ jobs” debacle – may seem trivial compared to what most Australians worry about, the first highlights Australia’s problem in achieving reforms that other countries seem to have no problem in doing (eg New Zealand) and the citizenship issue risks bringing on an early election to the extent it is threatening the Government’s lower house majority. Investors have yet to focus on the implications of an early election but a change of government could have significant implications for some sectors eg banks (with the Labor Party committed to a bank royal commission) and real estate (with the ALP committed to restricting negative gearing and cutting the capital gains tax discount).

- Our view remains that shares are at high risk of a short term correction led by the US share market where low volatility readings and high levels of investor sentiment until recently are a sign of complacency and participation by sectors and shares in recent gains has narrowed sharply which is often a sign of impending weakness. The trigger for a correction is always hard to know: but there are plenty of candidates out there including around North Korea, US politics and possibly the Fed later this year.

- Terrorism reared its ugly head again in Barcelona over the last week and our thoughts are with all those affected. It’s worth noting that the impact of terrorist attacks in recent times on share markets has been relatively minor and short lived as invariably there is little economic impact from them.

- Finally, the past week was disappointing for those of us in the US and Australia who value and celebrate diversity and respect for our fellow humans and detest discrimination and bigotry. But seeing American business leaders and most Australian Senators taking a strong stand was heartening.

Major global economic events and implications

- US economic data remains mostly solid. Retail sales rose strongly in July with an upward revision to June, manufacturing conditions in the New York and Philadelphia regions remain strong, jobless claims remain low, leading indicators are strong and while housing starts fell in July strength in the NAHB’s home builders’ conditions index suggest that the starts should remain solid going forward. The minutes from the Fed’s last meeting were balanced with the implication being that the tight labour market justified further tightening but low inflation means that it should be gradual.

- The minutes from the ECB’s last meeting highlighted the need for “patience, persistence & prudence” in getting inflation back to 2% and concern about the Euro overshooting on the upside. Expect easy money to continue, albeit with lower quantitative easing next year.

- Japanese June quarter GDP growth was much stronger than expected at 1% quarter-on-quarter and 2% year-on-year driven particularly by consumer spending and business investment.

- Chinese data points to slowing in growth in July. Retail sales, industrial production, investment (particularly property related investment) and M3 growth all slowed a bit in July consistent with earlier mixed readings from business conditions surveys and slower export and import growth. This likely suggests that recent policy tightening may be starting to impact. But it’s worth noting that total credit growth actually accelerated in July and any growth slowdown looks to be modest leaving growth around or above the 6.5% GDP target for this year.

Australian economic events and implications

- Australian data was the usual mixed bag. While the composition of jobs growth was poor in July, overall jobs growth remains solid and leading labour market indicators indicate it will remain so. Hopefully, the strength in employment growth will lead to stronger wages growth and this will boost consumer confidence and support consumer spending. But with June quarter wages growth remaining at a record low of 1.9% year on year there is as yet little evidence of this. And with the boost to growth from housing construction set to reverse, underlying inflation remaining below target and a rising A$ threatening lower growth and inflation it remains best for the RBA to keep interest rates unchanged at 1.5%.

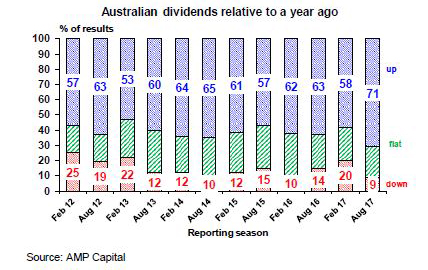

- We are now about 45% through the June-half earnings reporting season and results remains mixed. 41% of results have exceeded expectations which is the weakest since 2013 (see the first chart below), outlook guidance has been a bit soft, and reflecting this only 50% of companies have seen their share price outperform the market on the day they reported. Against all this of course, earnings are up with 73% of companies reporting higher profits than a year ago and 71% have increased dividends from a year ago although Telstra’s cut to future dividends was taken as a huge disappointment. 2016-17 earnings growth is on track to come in at around 18% with resources up 132% (down a bit from initial expectations) and the market excluding resources up 6% (which is a bit above initial expectations). Expectations for the current financial year have been revised down a bit to 1.6% though. Key themes have been: large caps doing better than small caps; moderate revenue growth with the domestic economy just okay; some disappointment from foreign earners; and dividends (ex Telstra) continuing to roar ahead.

What to watch over the next week?

- In the US, expect a further gain in home prices (Tuesday), continued strength in August business conditions PMIs (Wednesday), small gains in new home sales (also Wednesday) and existing home sales (Thursday) and a continuing rising trend in durable goods orders (Friday). The Fed’s annual central bankers’ symposium in Jackson Hole (Thursday) where the topic this year is “Fostering a Dynamic Global Economy” will be watched for clues on monetary policy both in the US and globally, particularly with Fed Chair Yellen due to speak on financial stability and ECB President Draghi also speaking and likely to issue further warnings about a rising Euro.

- In the Eurozone, expect August business conditions PMIs (Wednesday) to remain strong.

- Japanese inflation data for July is expected to show core inflation stuck at zero, providing a reminder that it’s a long way from the Bank of Japan’s 2% target and hence that the BoJ is a long way from starting to exit easy money.

- In Australia it will be a quiet week on the data front but the focus will remain on the profit reporting season which will see its biggest week with around 100 major companies reportingincluding Fortescue and BlueScope on Monday, Oil Search, BHP and Amcor on Tuesday, Worley Parsons, IAG and Woolworths on Wednesday, Scentre Group and South 32 on Thursday and Qantas on Friday.

Source: AMP CAPITAL ‘Weekly Market Update’

AMP Capital Investors Limited and AMP Capital Funds Management Limited Disclaimer