Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

Weekly Market Update – 11th August 2017

Investment markets and key developments over the past week

- Share markets fell over the last week on the back of escalating fears around conflict with North Korea. US shares fell 1.4%, Eurozone shares lost 2.6%, Japanese shares fell 1.5%, Chinese shares lost 1.6% and Australian shares fell 0.5%. Bonds benefitted from a flight to safety and continuing low inflation readings in the US, pushing yields down slightly. Commodity prices were mixed though with oil down but copper, iron ore and gold up. While the US dollar fell against the Japanese yen and the Euro, the Australian dollar fell against all three.

- North Korean risks have clearly ramped up significantly over the last week as the UN Security Council agreed on more sanctions, reports suggested North Korea may already have the ability to put a nuclear weapon in an intercontinental ballistic missile, President Trump threatened it with “fire, fury and, frankly, power” only to add a few days later that that “wasn’t tough enough” and that “things will happen to them like they never thought possible” and North Korea talked about plans to fire missiles at Guam. This is serious and naturally has led to heightened fears of an imminent military conflict. Of course it could all de-escalate again, but given North Korea’s growing missile and nuclear capability it does seem that the North Korean issue after years of escalation and de-escalation may come to a head soon. In thinking about the risks around North Korea it’s useful to think in terms of three scenarios as to how it could unfold:

- Diplomacy/no war sabre rattling would likely intensify further before a resolution is reached during which share markets could correct maybe 5-10% before rebounding once it becomes clear that a peaceful solution is in sight. An historic parallel is the Cuban Missile Crisis of October 1962 that saw US shares fall 7% before a complete recovery after the crisis was resolved.

- A brief and contained military conflict – perhaps like the 1991 and 2003 gulf wars proved to be, albeit without a full on ground war or regime change. In both gulf wars while share markets were adversely affected by nervousness ahead of the conflicts they started to rebound just before the actual conflicts began.

- A significant military conflict a contained gulf war style military conflict is unlikely as North Korea would most likely launch missile attacks against South Korea (notably Seoul) and Japan causing significant loss of life. This would entail a more significant impact on share markets with say 20% or so falls before it became clear that the US would prevail.

- Diplomacy remains by far the most likely path. The US is aware of the huge risks in terms of the potential loss of life in South Korea and Japan that would follow if it acted pre-emptively against North Korea and it is not interested in regime change there. Furthermore, North Korea appears to only want nuclear power as a deterrent. In this context Trump’s threats along with the US show of force earlier this year in Syria and Afghanistan are designed to warn North Korea of the consequences for them of an attack on the US or its allies, not to indicate that an armed conflict is imminent. Rather US officials are still working on a diplomatic solution. As such the base case remains that there is a diplomatic solution, but there could still be an increase in uncertainty and share market volatility in the interim and the risk is significant (particularly given the volatile personalities of Kim Jong-un and Donald Trump). Key dates to watch are North Korean public holidays on August 15 and 25 and September 9 which are often excuses to test missiles and US-South Korean military exercises starting August 21.

- More broadly, the intensification of the risks around North Korea comes at a time when there is already a significant risk of a global share market correction: the recent gains in the US share market have been increasingly concentrated in a few stocks; volatility has been low and short term investor sentiment has been high indicating a degree of investor complacency; political risks in the US may intensify as we come up to the need to avoid a government shutdown and raise the debt ceiling next month which will likely see the usual brinkmanship ahead of a solution; market expectations for US Federal Reserve tightening look to be too low (with only a 25% probability of a hike priced by December); tensions may return to the US-China trade relationship; and we are in the weakest months of the year seasonally for shares. While Australian shares have already had a 5% correction from their May high they may nevertheless be vulnerable to any US/global share market pull back. However, absent a significant and lengthy military conflict with North Korea (which is unlikely) see any pullback in the next month or so as just a correction rather than the start of a bear market. Share market valuations are ok particularly outside of the US, global monetary conditions remain easy, there is no sign of the excesses that normally presage a recession and profits are improving on the back of stronger global growth. As such, it is likely that the broad rising trend in share markets will resume through the December quarter and into 2018.

Major global economic events and implications

- US data remains solid with small business optimism rising in July to around a level that is about as high as it ever gets, job openings rising to a record and jobless claims remaining ultra-low. At the same time, producer and consumer price inflation remains soft with the core consumer price index stuck at 1.7% year-on-year in August. Strong growth readings keep the Federal Reserve on track to continue tightening, with a start to the winding back of quantitative easing expected next month, but low inflation will keep it gradual.

- The US June quarter earnings reporting season is now 90% complete with 78% beating on earnings, 68% beating on sales and earnings up around 11% year-on-year.

- Earnings growth seen in the June quarter is even stronger in Europe at 35% year-on-year and Japan at 37% year-on-year.

- Chinese export and import growth slowed a bit more than expected in July but remain consistent with gross domestic product growth running around 6.5%-7.0% year-on-year. Inflation data for July was benign with 1.4% year-on-year consumer price inflation and 5.5% year-on-year producer price inflation, neither of which have any significant implications for monetary policy.

Australian economic events and implications

- Reserve Bank of Australia Governor Lowe’s Parliamentary testimony provided no real surprises and basically repeated the themes of the bank’s commentary released over the last two weeks.However, he highlighted the issues around low wages growth, noted that the bank is continuing to watch consumer spending and the housing markets in Sydney and Melbourne very closely and reiterated his warning that the appreciation in the Australian dollar is weighing on inflation and growth and that a lower Australian dollar would be “helpful”. While Lowe indicated that the next move in rates is more likely to be up than down he also indicated that this won’t be for some time. Our view remains that rates will remain on hold ahead of a rate hike late next year, but if the Australian dollar continues to rise rate hikes will be even further delayed and the next move could turn out to be a cut. At this stage, Governor Lowe appears to be happy with the tightening in mortgage lending standards, but with a further cooling in Sydney and Melbourne still needed, additional measures cannot be ruled out.

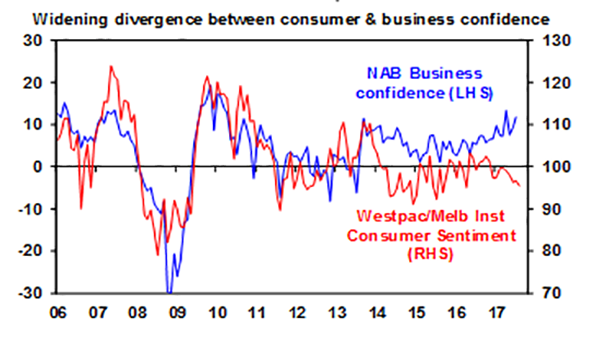

- Australian data was the usual mixed bag with solid readings for ANZ job ads and business conditions and confidence according to the NAB business survey for July and a slight rise in housing finance commitments but a further decline in consumer confidence. The gap between upbeat business confidence and downbeat consumers is widening and remains a bit perplexing. The combination of record low wages growth, rising energy costs, increases in some mortgage rates and worries about having too much debt are all weighing on Australian households. While low wages growth may be good for profits and business, subdued consumer confidence will weigh on future consumer spending. Better jobs growth should help eventually push up wages growth and hence consumer confidence, but as we have seen globally, the lags are long these days. All of which supports the case for the Reserve Bank of Australia to keep interest rates down for some time to come.

Source: NAB, Westpac/Melbourne Institute, AMP Capital

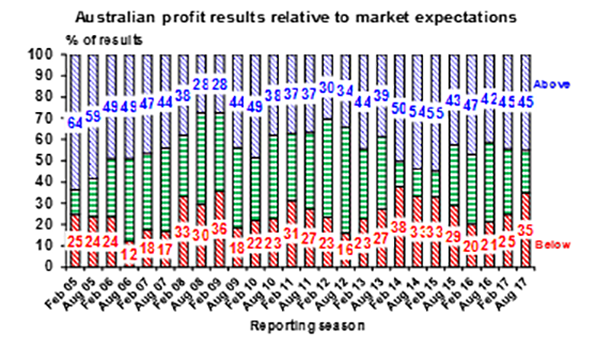

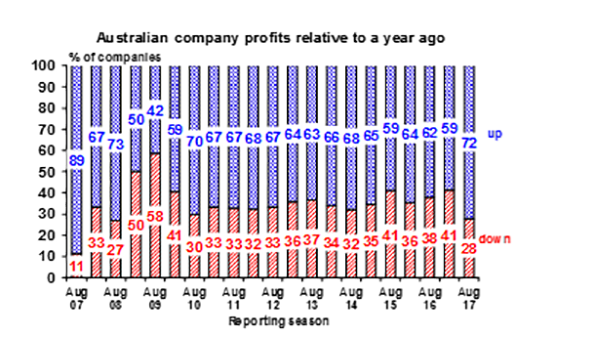

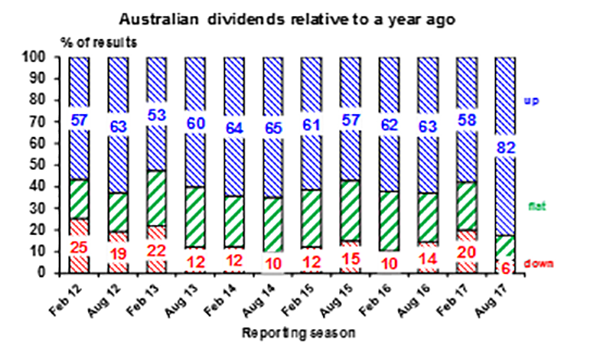

- Its early days in the June half-year earnings reporting season as only 25 or so major companies have reported, but so far it has been mixed. 45% of results have exceed expectations which is around the long term norm of 44% (see the first chart below), but 72% have reported profits higher than a year ago and 82% have increased dividends from a year ago. However, reflecting the mixed results so far, 50% of companies have seen their share price outperform the market on the day they reported and 50% have seen underperformance. It’s worth noting though that there is a tendency for the quality of results to tail off a bit as the reporting season proceeds. Consensus earnings expectations for 2016-17 have been revised down by 0.4% to 17.7% over the last week but mainly due to resources stocks.

Source: AMP Capital

Source: AMP Capital

Source: AMP Capital

What to watch over the next week?

- In the US, the minutes from the US Federal Reserve’s last meeting (Wednesday) are likely to firm expectations that it will announce the start of it letting its balance sheet run down next month (basically quantitative tightening) but signal that sub-target inflation means a degree of uncertainty around the timing of the next interest rate hike (likely to be in December). On the data front expect gains in retail sales and the National Association of Home Builders’ index (both Tuesday), housing starts (Wednesday) and industrial production (Thursday) and solid readings for the New York and Philadelphia manufacturing conditions indices.

- Japan’s June quarter gross domestic product growth data (Monday) is expected to show a bounce in growth to 0.6% quarter-on-quarter or 2.5% year-on-year driven by consumer spending and investment.

- Chinese activity data for July is expected to show a slight slowing after the acceleration seen in June with retail sales growth slowing to 10.8%, industrial production slowing to 7.2% and fixed asset investment unchanged at 8.6%.

- In Australia, the minutes from the Reserve Bank of Australia’s last board meeting (Tuesday) are likely to show the Bank firmly on hold with most interest likely remaining on how it sees the recent rise in the Australian dollar. Speeches by the central bank’s officials Kent and Ellis will be watched for any additional clues on interest rates. On the data front the focus will be on the labour market with June quarter wages data (Wednesday) expected to show that wages growth remains soft at 0.5% quarter-on-quarter or 1.9% year-on-year and July labour force data (Thursday) expected to show a 10,000 gain in jobs and unemployment remaining around 5.6%.

- The August profit reporting season will speed up in the week ahead with around 60 major companies reporting including Bendigo Bank, Ansel and JB Hi Fi on Monday, GPT on Tuesday, Westfield, Origin, Fairfax, Seek and Woodside on Wednesday and Wesfarmers, QBE and Telstra on Thursday. 2016-17 profits for the market as a whole are likely to have increased by around 18%, driven by a huge 133% gain in resources profits on the back of the rebound in commodity prices. Profit growth for the rest of the market is likely to be around 5.5% led by retailers, utilities, healthcare stocks and financials. Dividends and outlook statements will remain the key focus.

Outlook for markets

- Share markets are at risk of a short term correction with signs of short term investor complacency in the US share market and various potential triggers including risks around North Korea, US politics and the Federal Reserve. However, with valuations remaining okay particularly outside of the US, global monetary conditions remaining easy and profits improving on the back of stronger global growth, a pullback could be seen as just a correction with the broad rising trend in share markets likely to resume through the December quarter and into 2018.

- Low yields point to ongoing low returns from bonds.

- Unlisted commercial property and infrastructure are likely to continue benefitting from the ongoing search for yield, but this will wane eventually as bond yields trend higher.

- National residential property price gains are expected to slow, as the heat comes out of Sydney and Melbourne.

- Cash and bank deposits are likely to continue to provide poor returns, with term deposit rates running around 2.5%.

- While further short term upside in the Australian dollar is possible, views remain that the downtrend from 2011 will ultimately resume as the interest rate differential in favour of Australia is likely to continue to narrow as the Federal Reserve hikes rates and the Reserve Bank of Australia holds.

Source: AMP CAPITAL ‘Weekly Market Update’

AMP Capital Investors Limited and AMP Capital Funds Management Limited Disclaimer