Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

The FinSec View #15

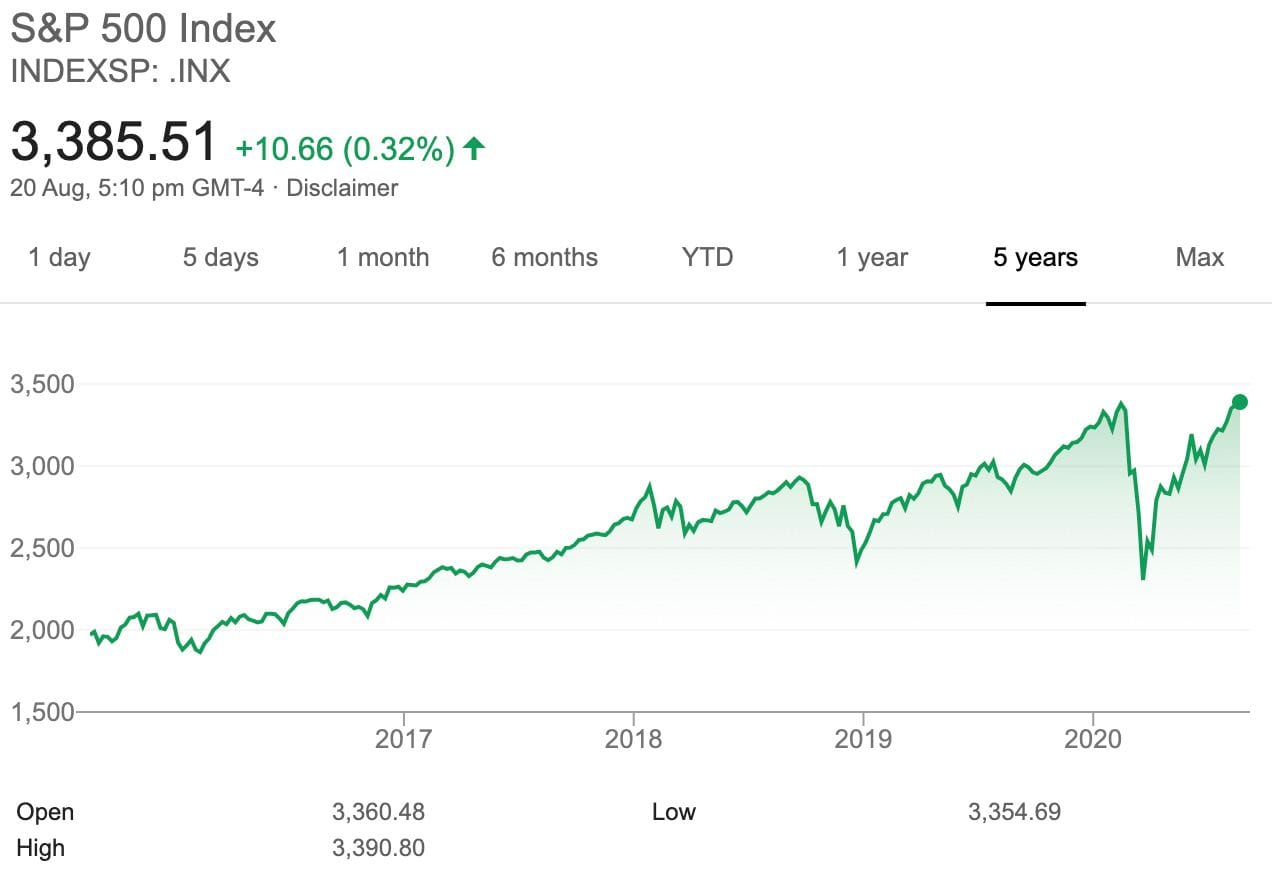

US Equities Defy Gravity

The S&P500 and the Nasdaq both hit all time highs this week.

A capitulation can occur at extremes in markets, where the rally becomes so strong that even the doubters get FOMO and want in on the action. Right now, we can see these pockets of euphoric sentiment emerging and caution that if such optimism continues, equity markets will become overbought. The danger here is that when risk-on assets reach this level, they can exhibit a disproportionate reaction to negative news – meaning they’re more vulnerable to a selloff (for instance US-China trade tensions or worries around future stimulus).

The drivers are of course March’s mass stimulus package and the ‘polarising’ tech giants. (It beggars belief to think that just one of these tech companies AKA apple – can be as big as the whole of the ASX combined! More on tech later in this view).

So how important is a second stimulus package for the US?

The short answer is ‘very’. While both the Democrats and the Republicans agree, they remain at odds with regard to the magnitude. The House of Representatives wants a $3 trillion package, while Senate Republicans favour a smaller package, to the tune of $1 trillion dollars.

With the two sides at an impasse and Congress now in recess until September, Trump has issued several executive orders that seek to continue aid, including one that would extend enhanced unemployment benefits at a rate of $400 per week. Other orders direct the U.S. government to defer payroll taxes and student loan repayments, and to prevent evictions.

Whilst experts say this won’t be enough, they do expect a second round of stimulus to be agreed on (somewhere between 1 Trillion and 3 Trillion).

TikTok, WeChat bans elevate China-U.S. tensions

For years, the Great (Fire)wall of China has blocked some of the largest online services coming out of the United States, including Google Facebook and Twitter.

This month, Trump indicated that he might be willing to build a wall of his own issuing executive orders that ban the use of the most popular Chinese-owned apps in the world: TikTok and WeChat. Claiming the apps pose risks to national security, citing concerns about data privacy and censorship they were given 45 days to find American buyers, or else.

Trump went further last Friday, ordering ByteDance, the Chinese owner of TikTok, to give up its American assets and any data that TikTok had gathered in the United States.

On Monday, the administration also clamped down further on Huawei by restricting the Chinese tech giant’s ability to buy computer chips produced abroad using American technology. That followed a White House initiative to begin purging Chinese apps and telecom companies from American networks.

The concern among markets now is that China will certainly retaliate and it may bear some partial resemblance to last year’s China-U.S. trade war. As 20 September approaches, markets will watch closely to see what a new, more invasive American philosophy of tech regulation will bring.

Even further, if more countries follow suit it could herald the beginning of digital controls based on diplomatic allegiances, protectionist aims or new concerns about the security of their citizens – Essentially an internet with borders.

Any such shift will have a big impact on American internet giants, which have greatly benefited from the borderless digital economy (outside China). These big tech stocks have driven the S&P and the Nasdaq to new heights, yet this (combined with Chinas reaction) has the potential to burst that balloon.

Things that make you go ‘mmm…’

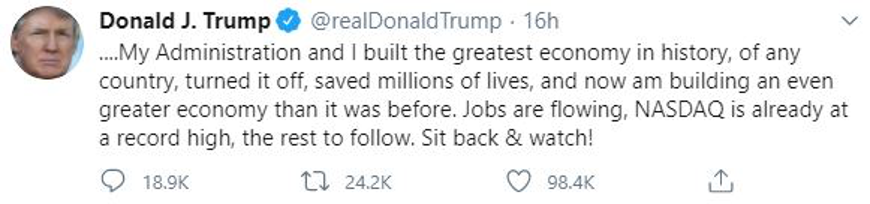

On the subject of Trump and the importance of the US elections, the tides appear to be turning. No one can rule out a Trump victory just yet. Political commentators back Trump over Biden in the debates, and US Sportsbet reported Trump’s odds are now $2.30 down from $2.50 and Biden up from $1.60 to $1.75.

Of course, who would doubt it, after all he’s built the greatest economy in history, saved millions of dollars and jobs are flowing…

‘Mmm…’ fact-check please!

Unemployment Claims During The Coronavirus Crisis

Initial claims filed weekly since Jan. 7, 2006 – source: Department of US Labour

The connectivity revolution is only just beginning

This week we bring you an article from our friends at Fidelity. Authored by Jon Guinness and Sumant Wahi, they write that the advances in connectivity (accelerated by the Coronavirus pandemic) means we are at the beginning of a second internet wave.

Having travelled through the first wave marked by super platforms (big tech giants) becoming global phenomena, now companies and investors are beginning to realise the second-order implications of such global connectivity. As a result, they believe the majority of investment opportunities around connectivity lie in the future and it will drive success in many companies outside the mega tech names.

Super is back

The preoccupation with pandemic induced worries must have eased enough this week to allow superannuation to regain its place as a political football.

Financial Services Minister Jane Humes has told the Australian Financial review that reform of the superannuation system is “in the wings” and could be unveiled during the October federal budget. This includes “a more efficient default system” and other areas considered “ripe for reform” including fees and the valuations of unlisted assets (hoorah!).

At the same time, Treasury is preparing to release its Retirement Income review, which is already reigniting debate over the scheduled increase in the super guarantee.

Last Friday, Prime Minister Scott Morrison flagged the possibility the government may freeze the rate (scheduled to go to 10% on 1 July 2021 on the way to 12% by 2024) stating “a rather significant event has happened since the 2019 election when he promised the increases would proceed”. Reserve Bank governor Philip Lowe also offered his view to the Standing Committee on Economics on 14 August 2020:

“I don’t know whether it would have a negative effect on employment. It would certainly have a negative effect on wages growth. If this increase goes ahead, I would expect wage growth to be even lower than it otherwise would be. So there will be an offset in terms of current income. Some people say that’s perfectly fine because people will have higher future income. There’s a trade-off: do we want people to have income now, or do we want them to have it later on?”

Research from the Grattan Institute has found raising the superannuation guarantee to 12 per cent would cost the budget $2 billion a year in tax concessions, on top of the $35 billion to $40 billion currently lost each year; hurt low-income workers by reducing take-home pay for little benefit in retirement; and fail to drive a meaningful increase in retirement income or result in a lower age pension bill.

The Reserve Bank has also found 80 per cent of the higher SG will be paid for by lower wages for workers, while the Australian Council of Social Service also opposes the hike.

However, Labor and the industry fund sector has argued the government’s early release program heightens the need for a higher contribution rate, arguing that a young saver who withdraws $20,000 will be as much as $100,000 worse-off at retirement.

As a positive and if nothing else, the early release scheme has at least increased people’s interaction with the super system, particularly the younger generations who can now understand it’s tangibility. Super for many is more relevant than ever and so it stands to reason that governments will try to make the most of the focus. The politics of super is back and we’re not surprised, with 3 Trillion dollars in the pool it was never going to be out of the news (or politics) for long.

Chart of the Week

Continuing with our tech theme, our chart of the week looks at how the big tech giants make their billions.

Despite their similarities, each of the five technology companies (Amazon, Apple, Facebook, Microsoft, and Alphabet(Google)) have very different cashflow breakdowns and growth trajectories. Some have a diversified mix of applications and cloud services, products, and data accumulation, while others have a more singular focus.

But through growth in almost all segments, Big Tech has eclipsed Big Oil and other major industry groups to comprise the most valuable publicly-traded companies in the world. As mentioned in our first article, by continuing to grow, these companies have strengthened the financial position of their billionaire founders and led the tech-heavy NASDAQ to new record highs. Click here to view image.