Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

Coronavirus Update

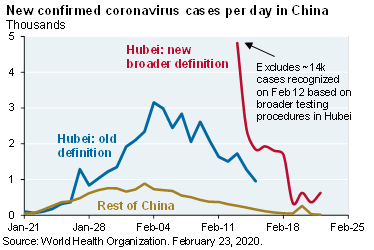

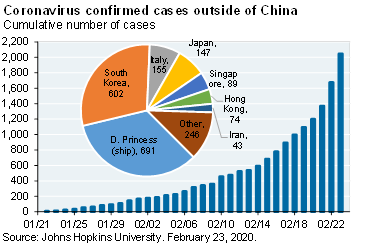

By now you have all probably seen the news on the spike in reported cases outside of China. The coronavirus disease is apparently communicable even by those who are not showing signs of having it, which is making it harder to control. The number of new infections in Wuhan/Hubei and the rest of China are falling sharply (latest new infection rate was 630 in Hubei and 20 in the rest of China). However, markets are reacting to the jump in reported cases cumulative outside China (mostly in South Korea, Italy, Japan and Iran), as well to the 700 people infected on the Diamond Princess ship (out of 3700 total crew/passengers).

How markets have reacted

We are seeing a major correction occurring in all global equity markets as investors try to assess the impact of the coronavirus on corporate profits. The Dow Jones is now down over 12% from the peak it reached on the 12th February as near panic grips many markets.The extensive factory closures and travel bans that we are seeing in many parts of the world due to the coronavirus outbreak will no doubt have a real impact on global economic activity and this will in turn impact the profits of many companies.

These types of markets, where uncertainty and fear are leading to many investors selling indiscriminately while not that frequent are nothing new. In these types of markets “the good the bad and the ugly” all get sold down heavily as investors reduce their overall exposure to the equity market.In times like these, there are a few things to bear in mind:

The correction is happening at a time when many sharemarkets around the world had reached record highs on investor optimism of continued world growth, with many stocks arguably in over-valued territory.

While the coronavirus is being taken very seriously by government authorities, so far the virus has led to around 3,000 deaths. To keep this in perspective, it is worth noting a 2017 World Health Organisation study attributed between 300,000 and 650,000 deaths per annum from the annual influenza virus.

Economic Implications

- Widespread shutting down of industries and regions did not occur during SARS.

- China is a much larger part of the global economy and more integrated into the supply chain than when SARS hit in 2003.

- China’s scope for fiscal stimulus is much less this time since it is running a larger fiscal defecit.

- Travel restrictions have occurred when many migrant workers had returned home for the new year holiday and now cannot return to their workplaces.

Markets that appear particularly vulnerable are:

- Emerging markets. Apart from China the other ones to watch in the short term are Korea and Taiwan given their supply chain links with China.

- Resource companies. If construction activity has stopped then iron ore prices could fall significantly in the short term.

- Other Chinese exposed Australian companies. Blackmores and Cochlear have already warned of an impact. The most other vulnerable stocks are those linked to tourism (Qantas, Sydney Airport, Crown and Star Entertainment).

- There is some risk to credit markets from the fall in oil prices and an extension of the crisis could cause some stress in companies with stretched balance sheets.

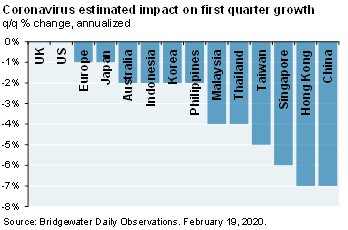

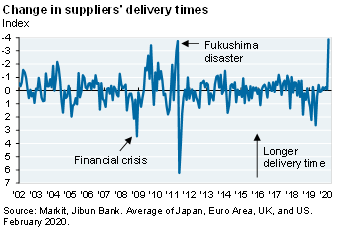

It is hard to pinpoint exactly what the economic outcomes of the Coronavirus might be, but they look worse than they did a few weeks ago and they will take some time to run their course. The first chart below is an estimate of the impact of the virus on Q1 GDP in different countries. The second chart looks at “supplier delivery times”, which reflects the extent to which supply chains are disrupted by the virus.

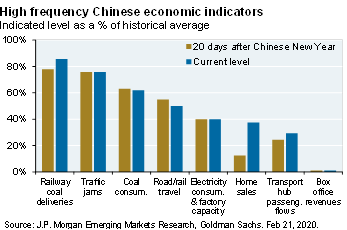

Within China, there are a number of indicators that reflect the impact of the lockdown on Chinese activity. Here’s how to read the next chart. Twenty days after the Chinese Lunar New Year (Feb 14) was the low point for economic activity due to quarantines and travel bans. At that time, for example, electricity consumption was running at 40% of its normal level for that time of the year. As of the latest reading, that hasn’t changed. Only coal deliveries, passenger flows and home sales have picked up since the low levels, and even these have only risen by a small amount.

In Australia, there will be a temporary disruption to tourism, education and exports (particularly commodities and to a lesser extent agriculture). Chinese tourist and education arrivals make up around 20% of total arrivals a significant chunk. There could also be an impact if Australians start staying home. On our estimates the total detraction to growth is worth around 0.2-0.3% of GDP. But there are offsets the $A depreciation from a risk-off global environment will boost broad export growth and lower travel to China is seen as a reduction in imports and it could even mean that Australians choose to holiday in Australia. Along with the bushfires, the total negative impact to March quarter GDP growth could be around 0.5% which is a decent amount.

Investors: keep watch, keep calm

Despite the rightly mounting concern about the spread of the Coronavirus, there is reason to believe that the threat will be contained and managed, but it could take some time with epidemics usually taking 6-18 months to run their course.

The rapid and widespread response from the Chinese government, and mobilising of countries outside China to detect and contain cases of the virus which have crossed their borders are important steps in containing the virus. Markets have been impacted by similar situations before and have recovered but the concern about the spread of the Coronavirus will keep investors cautious and markets volatile in the near-term given the disruption to economic activity. Once it becomes more evident that the number of people infected has reached a peak, markets tend to take this as a positive signal and will react accordingly.

We were due a correction and in many ways even if the markets fall further, taking pressure off of the next few months has the potential to allow the normalised growth cycle to continue for longer. It’s important to note that this is a situation which is constantly evolving, and that the synopsis covered in this update is a point in time assessment.

We stress that these views do not change our long-term view or asset allocation. The coronavirus will have a negligible impact on the value of portfolios over the medium to long-term.

** Resources:

- Michael Cembalest, Chairman of Market and Investment Strategy for J.P. Morgan Asset & Wealth Management

- Shane Oliver, Chief Economist AMP – The case for calm as coronavirus hits global markets

- Evans & Partners Chief Investment Officer and Portfolio Strategist- View from the outer February 2020

- Investors Mutal Limited (IML’s) Investment Team, Update on the current correction in equity markets