Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

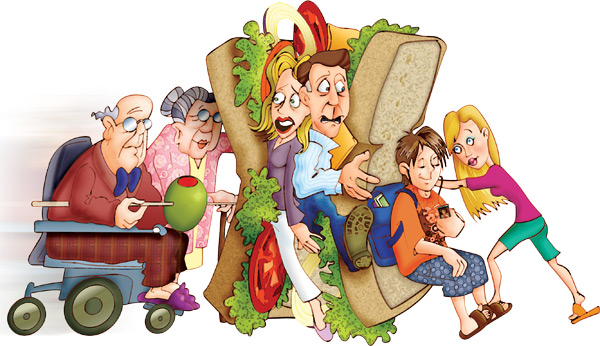

The Conversation: The Meat in the Sandwich

The “sandwich generation” has a lot on its plate these days, and it’s determining how to handle the financial side of the equation that’s most likely to be causing indigestion.

The term ‘sandwich generation’ is used to describe those who are supporting both children and parents financially and as care givers, a trend affecting more and more people as the giant baby boomer generation settles into older age and our population continues to live longer – And it’s definitely the topic headlining many a review meeting of late.

However, it would seem this is where the conversation both begins and ends. Many people are having the conversation with us, they don’t seem to be having the conversation with them and by them we’re referring to the children (generation one down) and the parents (generation one up).

Our advice; talk openly about money, make the conversation of finance real across all the generations.

Some tips

Generation one down – Discuss the basic tenets of sound money management with your children to help them develop good saving and spending habits at an early age. This includes helping them understand the role that superannuation, insurance protection, fixed investments and equity investments play in their overall financial strategy.

Consider this dialogue (it might just put a ‘stone in your shoe’);

“Does your son-in-law have life insurance?”

“No why?”

“Well…. where are your daughter and 4 grandchildren going to live if something happens to him?”

It may be confronting to plan for the worst, but choosing to believe it won’t happen to me is a dangerous strategy.

Generation one up – EDUCATE YOURSELF ABOUT YOUR PARENTS’ FINANCES

Adult children often are reluctant to question their parents about money, but it’s important to understand our parents’ financial situation so that you are prepared to help them when they need it. Ideally, you want to determine what they receive in pension and Social Security payments and how much they have in savings. Find out about their fixed expenses too, such as mortgage or rent and utilities payments. Familiarise yourself with their insurance coverage, have any policies lapsed? Don’t forget to consider medical expenses, including the cost of health care insurance, medications, and provisions for emergencies. Do they have any Aged Care preference? What are their Estate Planning desires, are their wills and powers of attorney up to date?

It may feel awkward to ask your parents about these details, but when you are informed, you are in a better position to help. You can use this information to gain a broader sense of how their needs may affect your own financial situation.

Don’t neglect your own needs; It’s one thing to be sandwiched between the needs of generations one up and one down, but it’s quite another to loose yourself and your own financial goals. You can’t help others if you’re not on firm financial footing yourself. Don’t be afraid to re-evaluate, talk to your adviser about your changing needs and those of your family, being realistic about the current financial challenges, revisiting a retirement plan, and rebalancing a portfolio for a change in risk-readiness can help keep retirement a reality, even in the face of economic uncertainty.

By focusing on your retirement, you’ll set the foundation for a secure financial future and ensure that your own children will not have to help you in your later years.