Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A FinSec View – Stagflation, Ok Boomers, Market emotions, Labour shortages and More

1st July 2022

It is a brand new month, quarter and fiscal year, and we will just have to wait and see if (for markets and the economy) it is indeed a new beginning or much of the same.

Today also marks the 30th anniversary of the introduction of compulsory super and the Superannuation Guarantee (SG). Initially set at 3%, the SG rises to 10.5% today on its way to 12% by 2025. For all its complexity and shortcomings, it’s an exceptional policy achievement which forces most people to save for their later years and boosts the capital and savings of the country.

On 1 July 1992, when SG started, total super balances from other schemes totalled $148 billion. The 23 million accounts are now worth about $3.4 trillion. The architects of the system are no doubt amazed at this milestone.

For those interested in a bit of history, this article by author and journalist Noel Whittaker draws on his extensive memory and records to show how we ended up with the current retirement savings system. From airline strikes to unpopular surcharges, it’s an interesting read and a revealing journey indeed – please click here.

In this week’s view, we ponder stagflation, take a look at the new census data and reveal some frightening statistics about Australia’s labour shortages. We hope you enjoy the read.

Market Update

Following a 2% tumble on Thursday and the worst month and quarter in two years (at the time of writing), the ASX200 is up today in the order of around 0.4%. No mean feat, as it manages to shake off a decline in the US markets overnight that wrapped up its quarter in a not-so-encouraging way, now down 21% for the first half of the year, the worst first half for Wall Street since 1970.

Last night’s significant drivers were, firstly, an update on inflation and the good news that whilst prices are still rising at a fast pace, they are trending below expectations. Unfortunately, this optimism was largely offset by a big drop in consumer spending. In fact, the growth and consumer spending numbers came in at only half of what the market was expecting. It highlights the tightrope that policymakers are forced to walk…

We expect it to remain a volatile time in markets as investors continue to grapple with a range of different issues – inflation being the most obvious one.

There are, of course, several underlying causes of inflation and the markets (the world) are trying to get a handle on them. First and foremost is the disruption in energy markets. Years of structural underinvestment in energy have left us short of supply, and Russia’s invasion of Ukraine has compounded this.

Second are the logistics and supply chain issues. Global lockdowns saw demand switch from services to goods creating a mismatch in supply and demand, with factory closures, delays and disruptions (more recently China) exacerbating the issue.

And then, we have the more structural forces posing potential longer-term risks.

- Demographics

- Integration of cheap labour into the global economy (particularly China) is maturing.

- The size of the working-age sector is set to decline in both absolute terms and relative to the overall population.

- Geopolitics and de-globalisation

- A pandemic and a war see countries and corporates increasingly keen to ensure ‘resilience’ of key inputs = bias towards home production.

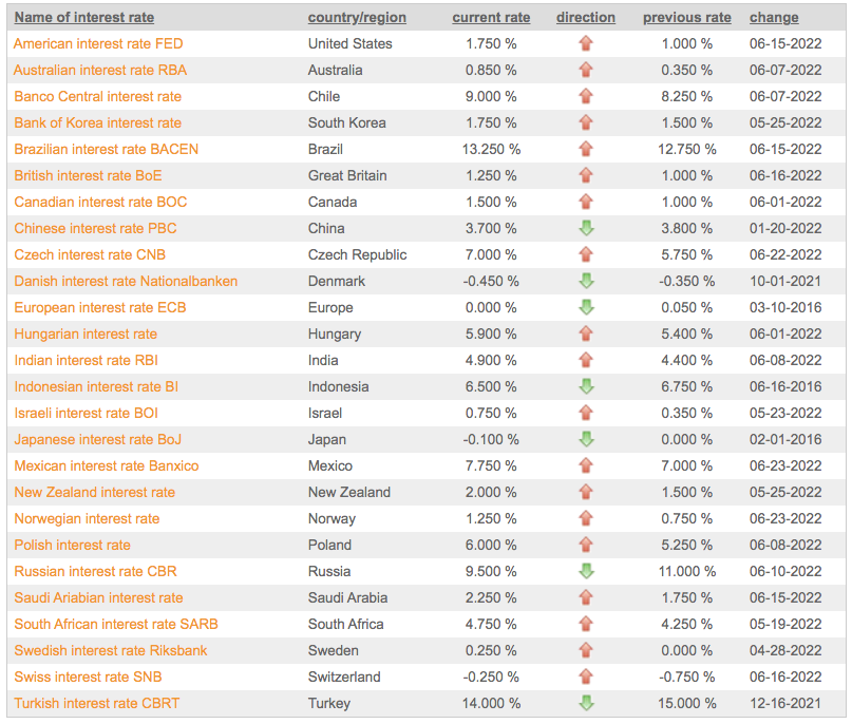

Central banks, of course, remain aggressive in trying to tame inflation through rate hikes.

For those who missed our last missive, our views on how high we believe interest rates will go and what the chances of a recession look like can be found here.

Stagflation

Do we fight the ‘stag’ or the ‘flation’ is the conundrum faced by Central Bankers right now.

To date, Central bankers have exclusively chosen, (as the below chart depicts – with a few obvious exceptions) to attack the ‘flation’ with rapid rate hikes.

However, some experts will argue that it is a misunderstanding of how the economy works to focus on inflation alone. Put simply:

- Supply and demand – prices rise when the amount of spending increases by more than the quantities of goods and services sold, and

- The way Central Banks fight inflation – is by taking money and credit away from people and companies to reduce spending.

Lifting rates could be seen as just a shift from ‘squeezing’ people via inflation to ‘squeezing’ people by giving them less buying power.

With elevated financial vulnerabilities (unprecedented debt levels and surging house prices) and the Fed also selling government debt, it is likely that private credit growth will have to contract, weakening the economy (as we saw in the consumer spending data released last night). As a result, those in the stagflation (both low growth and high inflation) camp believe that over the long run, many Central Banks will be forced to chart a middle course if they are to avoid a hard landing. A period of stagflation is looking more likely…

Ok Boomers

The 2021 census results are in, and the Millennials (or Gen Ys) have overtaken the Baby Boomers as the largest generational group in Australia. Each generation has over 5.4 million people, but over the last decade, Millennials have increased from 20.4% to 21.5% of the population, while Baby Boomers have decreased from 25.4% to 21.5%. Generation X and Generation Z come in at 19.3% and 18.2% consecutively.

We have been told that Boomers had it good for many years, whereas in 1996, 42% of homeowners had no mortgage; this was down to 31% in 2021. This said, the younger generations are set to inherit billions in wealth in coming decades (although Boomers may have the last laugh yet again, as life expectancy continues to rise).

Interestingly, data also revealed that the size of households has declined over the past five years (a shift that may have been accelerated during the pandemic), with the average number of people per household falling from 2.6 to 2.5 people. This variation whilst appearing insignificant as a percentage involved the establishment of an additional 200,000 households – which goes some way toward explaining the fact that housing vacancies have plummeted and rents are soaring once again (they initially fell in some areas early in the pandemic as students and tourists left the country and migration came to a halt).

Around 13% (one in eight) of Baby Boomers are caring for other peoples’ children (usually their grandies), and Boomers are the generation most likely to volunteer and provide unpaid assistance.

The Census also found that 48% of Australians have a parent born overseas, and 28% of people were born overseas. As a nation, we rely heavily on immigration for population growth (more on this below).

Leading demographer, Bernard Salt, writing on the Census this week in The Australian, concluded optimistically:

“The lesson for business and government is that there will be no return to normal. The lesson is to read the market, to read the electorate, to understand the drivers of modern Australian thinking. Even from yesterday’s high-level data release it is evident to me at least that Australia is being reshaped not so much by individual events but by the quiet determination of the Australian people to create what they consider to be a better version of their nation for the 2020s and beyond.”

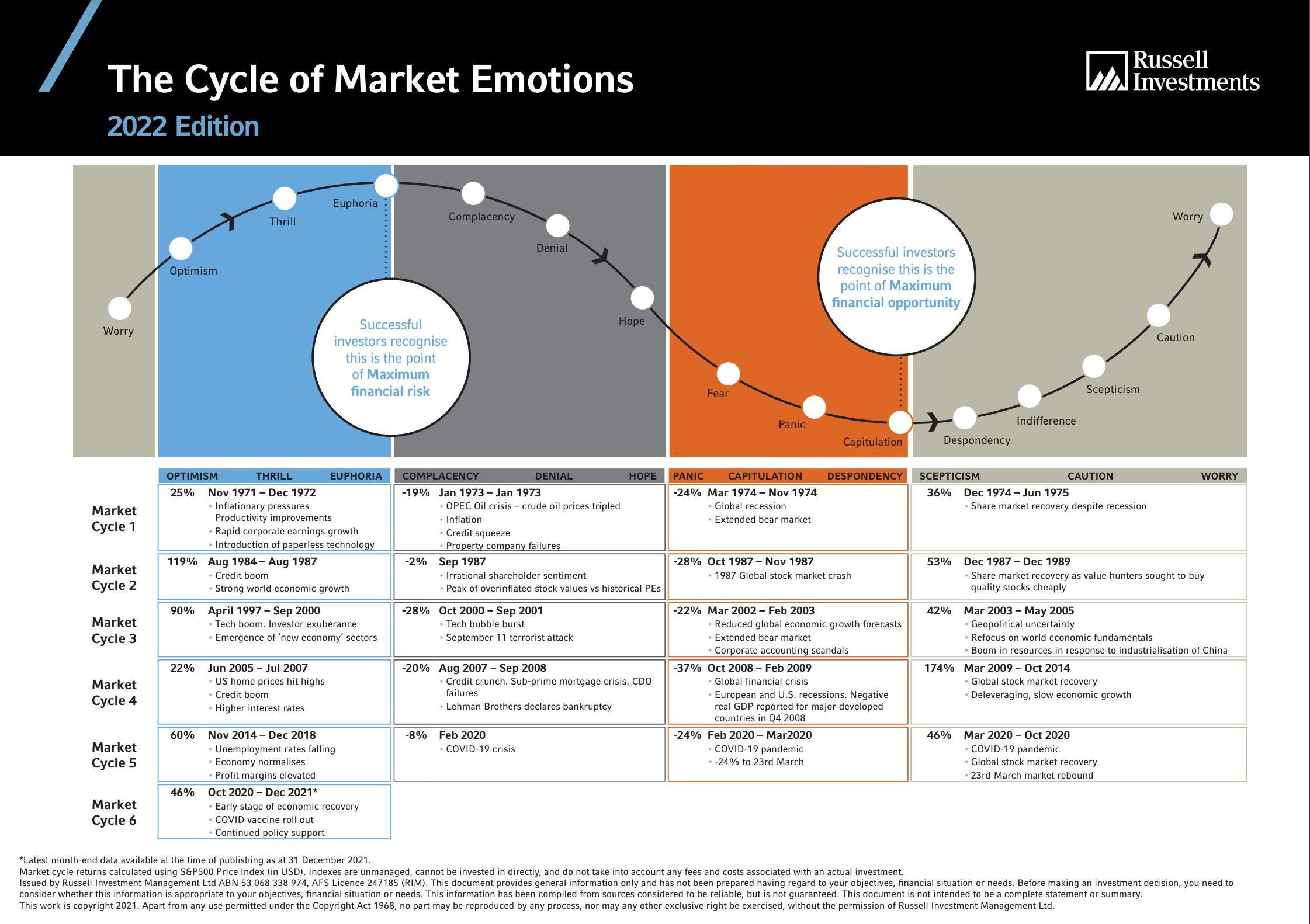

The Cycle of Market Emotions

“History doesn’t repeat itself, but it does rhyme.” It’s well documented that Twain used this phrase back in 1874. Many others have said something similar over the years, and in 1965 psychoanalyst Theodor Reik said essentially the same thing in an essay titled ‘The Unreachables.’ It took him a few more words, but his formulation is a good one.

“There are recurring cycles, ups and downs, but the course of events is essentially the same, with small variations. It has been said that history repeats itself. This is perhaps not quite correct; it merely rhymes.”

The events of investment history don’t repeat, but familiar themes do recur especially behavioural themes. Over the past 50 years, we’ve seen dramatic examples of ups and downs, and we are always struck by the reappearance of some classic themes in investor behaviour.

When things are great, we feel nothing can stop us. And when things are going badly, we look to take drastic action. This chart from Russell Investments – ‘The cycle of market emotions’ – looks at past market cycles to learn about historical market returns. It certainly gives some perspective to the emotions that many investors may be feeling right now.

How do we ride the rollercoaster? Through the implementation of rigorous, process-driven portfolio management built on a foundation of careful analysis and research.

A pdf version can be found here.

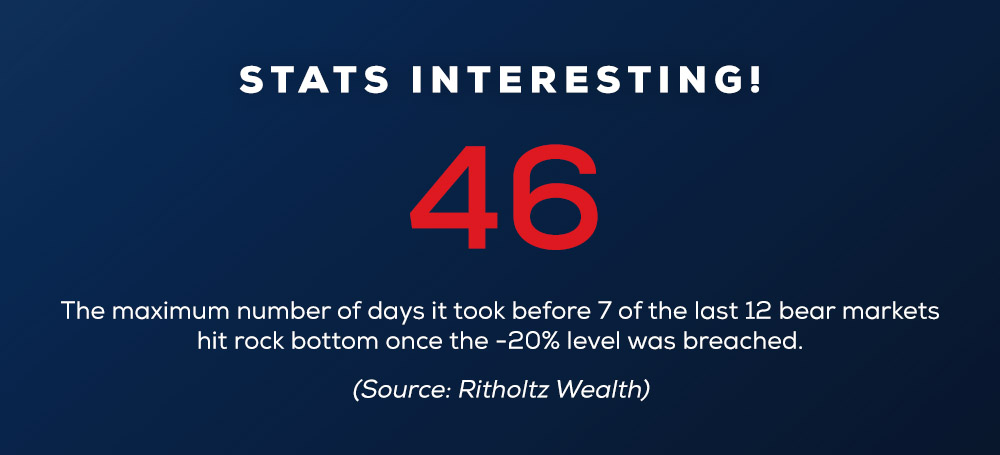

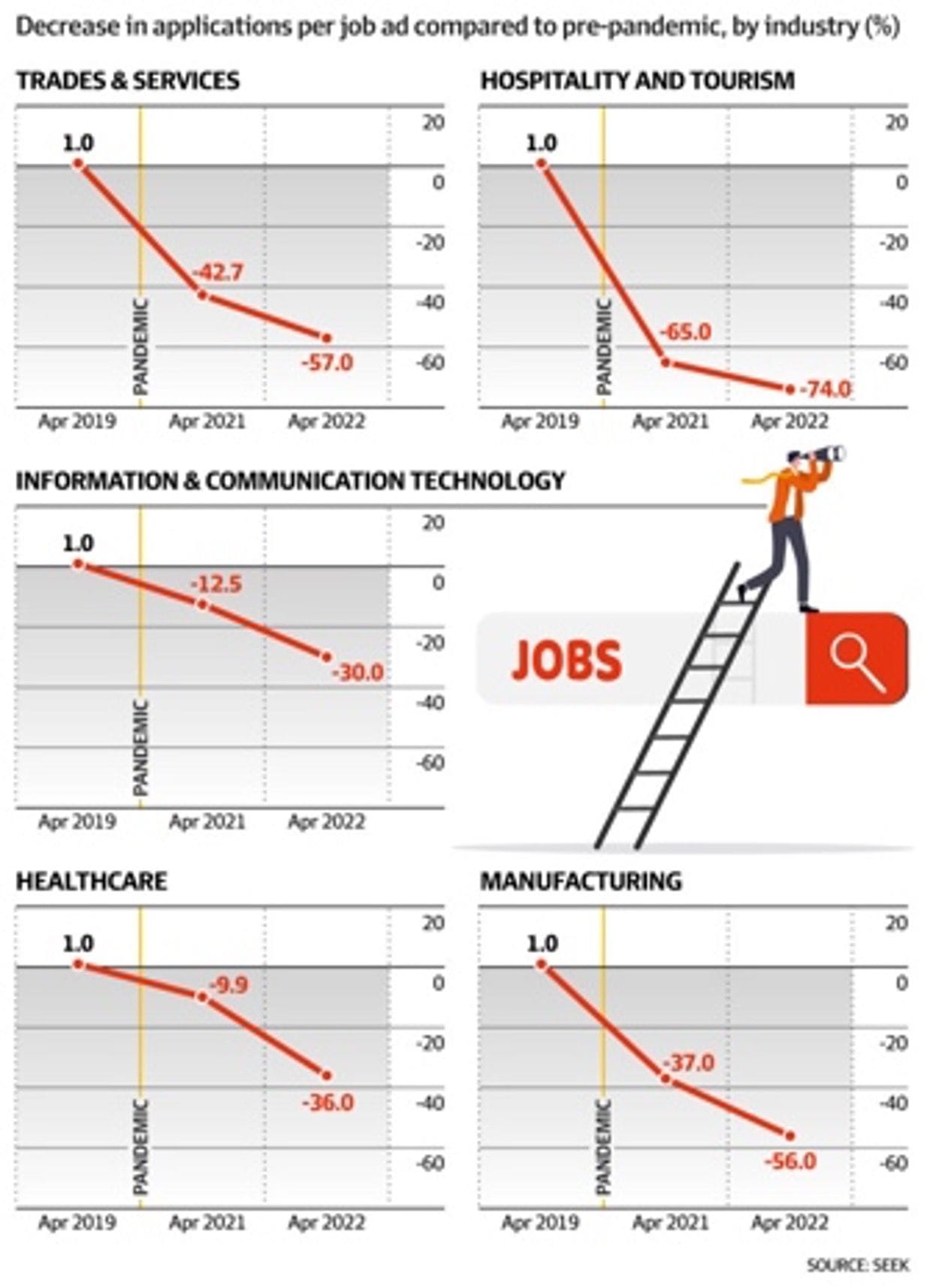

Chart of the Week

Our chart(s) of the week will come as no surprise to many business owners and recruiters out there. Australia is in the midst of one of its largest-ever labour shortages. There are more than 423,000 job vacancies, according to data from the Australian Bureau of Statistics. Australia’s unemployment rate sits at 3.9 per cent, a 48-year low, and the proportion of the adult population holding a job has hit a record high of 66.7 per cent.

According to Seek, the five sectors that have been hit hardest are trades, hospitality and tourism, healthcare, manufacturing, and technology. The causes:

- A lack of available workers as a result of the pandemic. Sectors such as hospitality and manufacturing currently do not have their usual supply of international students and holidaymaker visa holders to take on jobs; and

- A shortage of skills is impacting healthcare, technology and specialised trade roles.

With the labour market so tight, attention is now closely focused on whether businesses can pay higher wages to attract staff, both from Australia and overseas. Not likely, is what most business owners will tell you – high energy and freight costs, the cost of ever-increasing ‘red tape’ and compliance costs as well as a low Aussie dollar making the cost of importing goods more expensive than usual, makes for a tough environment.

Regular readers of the View will no doubt be aware of our position. The three Ps – productivity, participation and population. With zero population growth and record-high participation, the answer comes down to productivity. As businesses face their most uncertain period since the GFC, being able to produce more with existing resources is not only a path to growth but a path to avoid the stagflation referred to in our article above.

Picture of the Week

Stay safe and look after one another. As always, if you have any concerns or questions at any time, please reach out to your FinSec adviser.