Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View – RBA review, Charlie’s happy & fulfilling life, 60/40 portfolios, To wait or not? and More

5th May 2023

It’s reached the stage where the RBA cash rate leads the news every few weeks.

After this week’s increase to 3.85%, the 11th in a year, it’s not difficult to conclude that Governor Philip Lowe will most likely use the remaining four months of his term to quash inflation, even if the consequences for some borrowers are a little dire (Australians are definitely feeling it. Consumer credit agency Equifax reports a large increase in demand for credit cards and personal loans).

We don’t envy Lowe’s job (particularly navigating a pandemic and the aftermath thereof). There’s little doubt that his intentions are to serve best interests and do his job well, and criticisms in the review of the Reserve Bank of Australia (RBA) released to the public just over a week ago have stung him.

The report recommended profound changes to the central bank. Lowe, amongst a significant cohort, argues it lacked any evidence that these changes are, in fact, necessary – beyond that other countries do things differently and that Australia should follow suit. Others say it delivered the pragmatic changes necessary to bring Australia into line with international best practice.

Assuming the recommendations are adopted, the Albanese government is set to split the long-standing board of the RBA, separating the setting of monetary policy and institutional governance functions of the central bank into two distinct boards “to bring greater technical and operational expertise” to its functions.

The separation of the RBA board is one of 14 core recommendations stemming from the review that constitutes one of the biggest changes since the institution was formally separated from the Government in 1983.

The review suggests the Government should legislate changes to commence from July 1 next year.

We can only assume that Lowe’s time will not be extended in that while the Government has accepted all recommendations, he disagrees with many of them. Putting aside that he has been at the RBA for 43 years and ‘CEO’ since 2016, it would be near impossible for him to implement changes he does not agree with, or at least the supporting evidence that led to them.

To be sure, Lowe has made mistakes. The errant 2024 interest rate rise guidance was obviously unfortunate in light of the eleven interest rate rises and counting (to be fair the media’s criticism did not take into account the need to move in synchronicity with the rest of the West in avoiding exchange rate turmoil). But, running the RBA is more than setting interest rates. It involves overseeing the national payments system, providing liquidity to the financial system, managing 1400 staff, chairing the Council of Financial Regulators, producing and issuing banknotes, attending global economic meetings, fronting parliament and taking questions from journalists.

A dilemma for Treasurer Jim Chalmers, perhaps, is that when Treasury casts around for candidates to be governor, there is not an obvious successor.

What we do know is that whoever is governor, condemnation bourne of politics should never deter them from taking what they believe is the best course to manage the nation’s monetary policy.

As for the recommended changes, only time will settle the debate on whether they will deliver superior monetary policy outcomes or not.

Market Update

Significant data from the last fortnight included the inflation numbers out of the UK and PMI numbers out of Europe and the US.

In inflation terms, the UK remains a ‘mess’ with numbers still in the double-digit territory. Food inflation came in just under a whopping 20%, and headline inflation (excluding mortgage costs) has also increased.

PMI numbers out of Europe and the US were surprisingly good.

*** By way of reminder, PMI (Purchasing Manager Index) is a survey of businesses that provides an important ‘pulse check’ for the economy. Generally, the index moves around a level of 50. Anything more than 50 and it indicates businesses are seeing improving conditions; anything below 50 and conditions are getting worse. For the purpose of the survey firms are separated into manufacturing and services.***

US figures came in at 50.2 compared with 49.2 in March. New orders returned to expansion territory, and production increased at the fastest pace since May 2022. Anticipating greater future sales has led firms to ramp up employment, with the rate of job creation reaching the fastest since September 2022. Looking ahead, the degree of optimism rose to the strongest for three months.

It was a similar story in Europe with a composite figure of 54.1 up from 53.7 in March. Interestingly manufacturing fell from 47.3 down to 45.8, but services rose from 55 to 56.2 (a trend we are seeing universally, including Australia). This marked the strongest growth in services in a year with Italy and Spain being the main drivers, helped by the tourism industry and a travel boom.

Overall it is good news for economies but bad news in the fight against inflation.

In Australia, last Wednesday’s CPI figures made for our most significant data of late. Over the twelve months to the March quarter, the CPI rose to 7%, showing signs that interest rate rises are beginning to flow through to households and dampening consumer demand.

The figure is slightly higher than the 6.9% that analysts were predicting but lower than the 30-year-high of 7.8% from the December quarter. It is not expected that the drop is enough for the RBA to stop interest rate hikes (as evidenced this week).

From the market’s perspective, volatility is the continuing trend along with the ‘good news is bad news’ and ‘bad news is good news’ cycle.

We are certainly at a point not anticipated a year ago, but we feel we are now very near to the end of the cycle. Maybe one more rise, more than that, risks a tailspin for the economy.

Charlie’s Tips for a Happy and Fulfilling Life

Warren Buffett and his business partner Charlie Munger are by far the most quoted people in investing and finance (including our own missives). They regularly give insightful interviews, and Buffett has written a letter to Berkshire Hathaway shareholders every year since 1977. Trawling through his letters is a great way to learn about investing.

It is less well-known that Munger often talks about how to enjoy a happy and fulfilling life, despite his many personal setbacks. He will soon turn 100 and seems as enthusiastic as ever. He says:

“Generally speaking, envy, resentment, revenge, and self-pity are disastrous modes of thought. Self-pity gets pretty close to paranoia… Every time you find yourself drifting into self-pity, I don’t care what the cause, self-pity is not going to improve the situation. It’s a ridiculous way to behave.”

There are many articles on Munger’s rules for a happy life, but here are a few favourites, some with relevance for investing:

-

Manage expectations.

“The first rule of a happy life is managing expectations. Aspiration is a wonderful motivator but managing expectations avoids disappointment. You want to have reasonable expectations and take life’s results good and bad as they happen with a certain amount of stoicism.”

-

Avoid envy.

“Envy not only makes people miserable, but turns them into lousy investors.”

-

Eliminate resentment.

“Wallowing in resentment leads to more misery, and it’s better to think of things to be grateful for.”

-

Stay cheerful despite adversity. Life does not follow a predetermined path.

“Life will have terrible blows in it, horrible blows, unfair blows. It doesn’t matter. And some people recover, and others don’t.

There I think the attitude of Epictetus is the best. He thought that every mischance in life was an opportunity to behave well. Every mischance in life was an opportunity to learn something, and that your duty was not to be immersed in self-pity, but to utilise the terrible blow in a constructive fashion. That is a very good idea.”

-

Be reliable and surround yourself with reliable people.

“If you’re unreliable, it doesn’t matter what your virtues are. Doing what you’ve faithfully engaged to do should be an automatic part of your conduct. You want to avoid sloth and unreliability.”

-

Read and study constantly.

“Learn from past mistakes and become as educated as possible.”

What is the relevance of happiness to investing? It’s a stretch to argue happier people make better investors, but if the daily volatility of the market and share prices make you tense and losses create anxiety, then perhaps you’re not living your best life. Whilst it may be tempting to adjust your portfolio constantly, the results are likely to be inferior versus staying invested for the long term.

Take Munger’s advice and look for rules that make you happy – outsource the investment worry to the experts!

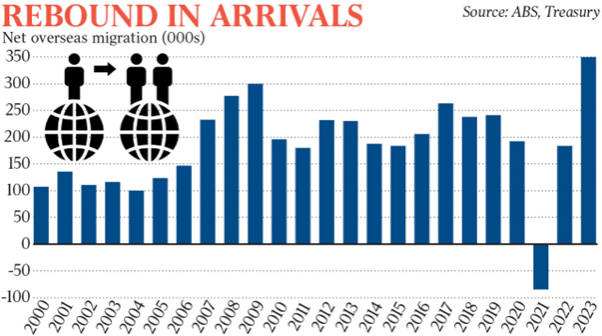

Chart of the Week #1

An extra 900,000 residents are set to join us.

In the September quarter of 2022, 106,000 migrants came into Australia. This is the largest quarterly addition since the data commenced in 1979. The influx is boosting spending and the tax take, helping to ease labour shortages and fuelling demand for services. All of which is good.

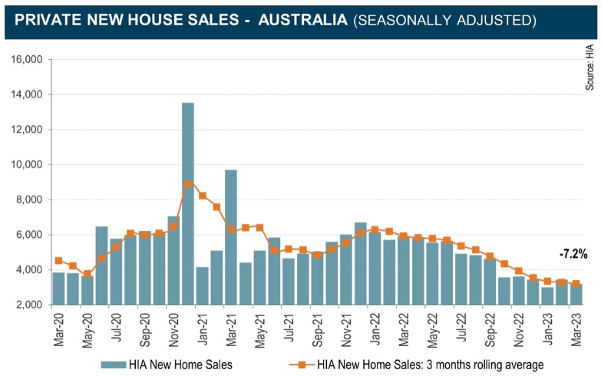

Chart of the Week #2

The raft of new entrants to Australia is putting severe strain on our already struggling housing sector. New home sales have plummeted in recent months, based on data from the largest volume home builders in the five largest states.

The continuing failure of some building companies, coupled with higher construction costs and difficulty getting finance, all mean it will probably get worse before it gets better. It’s a real issue for the nation and a big dilemma for policymakers.

Population is one of the cornerstones of a healthy economy, but shelter is a basic necessity. All eyes will be on next week’s budget, in which Chalmers is set to reveal a migration policy overhaul (an effectively smaller Australia) – let’s just hope he gets the balance right.

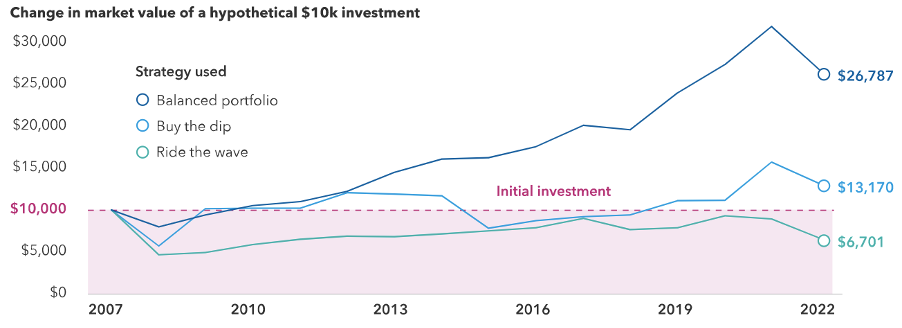

Capital Group – Investment Trend #3

In this week’s instalment of Capital Group’s 10 investment themes for 2023, we look at 60/40 portfolios.

Ask your favourite search engine, “Is the 60/40 portfolio dead?” and it will generate about half a million results. Such scepticism is understandable following a year in which stocks and bonds both declined for the first time in decades. Despite the poor year, Capital believe the concept of a well-balanced portfolio — whether a 60/40 or 70/30 equity/fixed income split — is indeed alive and well.

For the first time in years, it’s possible to seek total returns in the high single digits by investing in core bonds and proven dividend-paying stocks without taking undue risk or reaching for yield. With the yield on the Bloomberg U.S. Aggregate Index currently above 4%, many core bonds can provide a consistent return in the mid-single digits. That’s something we haven’t seen since 2008.

Companies that pay a dividend can contribute to an attractive return picture with yields north of 3% and the potential for capital appreciation.

Traditional asset allocation is not an outdated strategy. It will always make sense to think about balance, diversification and risk. A one-size-fits-all approach doesn’t work for every investor. It’s about building portfolios from the bottom up that align with investor goals.

A balanced portfolio would have outpaced other strategies over the past 15 years.

Whether you are a Republican or a Monarchist, the coronation is a compelling ceremony.

It is easy to forget that the monarchy itself has evolved over the last 350 years (Queen Elizabeth II was the first to pay taxes), and in acknowledgement of tomorrow’s events, the below stats and facts may be of interest.

Since 1760, the net income of The Crown Estate has been surrendered to the Exchequer by the Monarch under successive Civil List Acts, passed at the beginning of each reign. Responsibility for managing The Crown Estate is trusted to the ‘Crown Estate Board’.

The Crown Estate gives its entire annual surplus (net profit) to the Treasury. The Act simply provides a mechanism that will be used by the Treasury to determine the amount of Government funding for the Monarch.

The Monarchy has often been described as an expensive institution, with Royal finances shrouded in secrecy. In reality, the Royal Household is far more transparent, publishing a summary of Head of State expenditure together with a full report on Royal Public finances available to the public here.

The Royal Household is also subject to the same audit scrutiny as other government expenditures via the National Audit Office and the Public Accounts Committee.

Another misconception is the payment of taxes. While it is not required, Queen Elizabeth II paid her dues on a volunteer basis, paying income tax and capital gains tax since 1992. We assume King Charles III will follow suit…

The Only Free Lunch in Investing

Mercer’s 2023 periodic table colour-codes 17 major asset classes and ranks how each performed, on an annual basis, over the last 10 years. It is used to highlight the volatile nature of financial markets.

At a glance, it’s easy to see that one year’s winner can be at the bottom ranks the next. We can never predict with a high degree of confidence what the future will hold over the short to medium-term. Therefore, for most individuals, the power of investing is harnessed through securing asset class diversification, taking on the risk you can tolerate and adopting a longer-term perspective – all we need is just a little patience…

As the old adage goes, “Diversification is the only free lunch in investing”.

Demystifying the Mosaic

Looking across 2022 and the past decade, the following observations can be made:

- Fifteen of the 17 asset classes generated a negative return last year, compared to only four asset classes in 2021, showing the breadth of financial market correction in 2022.

- Leading the positive returns in 2022 was Australian Direct Property, with a stellar positive return of 10.7%, reflecting that investors sought out alternative inflation-linked sources of return. Mmm… watch this space.

- Cash featured in second place in 2022, with a positive return of 1.3%, as confidence in risky assets declined with the tightening of monetary policy.

- Australian equity declined 2.7%, which was relatively moderate compared to other asset classes, as Australia benefitted from elevated commodity prices and the eventual re-opening of China in November 2022. Australian Small Caps, on the other hand, down 18.4%, underperformed the broader index.

- International Equity (H) declined 18.1%, with a re-pricing of (especially) US and Growth style equities, as did Global Listed Property (H), down 23.5%, in anticipation of the impact of rising interest rates.

A Thorny Issue – To Wait or Not?

It’s a question we are often asked to discuss – should make our children wait for their inheritance or not?

As you can imagine, it’s a thorny issue. The parents reflexively believe that the money should be given through inheritance after they pass away. The children, or at least some of them, think the money would be of more value if it were given to them before that time. To them, it would be more compassionate, and might also avoid any quarrelling between the children after their parents’ deaths.

The issue doesn’t make for pleasant dinner table conversation but it’s one that’s likely to be aired more often as Baby Boomers in Australia get older and leave behind larger bequests (an estimated $3.4 trillion to 2050). There is no simple answer and whilst every situation is different there are some common ‘pros and cons’ that can be useful in making a decision.

Pros:

- The joy of giving. If you give money to your children early, you will get to see the fruits of that. Whether it’s a holiday, the purchase of a home or the funding of education, helping loved ones like this can nott be overstated.

- You may be able to give money when your children most need it. It is believed that the peak utility for money is around 30 years of age. Instead of children inheriting it at age 50 or above, when they often don’t need it so much, it might be better to give the money to them when they require it most.

- Potential tax benefits. Australia is one of only eight developed countries that don’t tax inherited wealth. However, there is a 17% tax on superannuation passed to a non-dependant, which is an important part of estate planning as strategies are required to take the money out of super before death. Given the current government’s crackdown on super tax breaks for the wealthy, it wouldn’t be surprising if inheritance taxes were looked at in future.

Cons:

- You might run out of money. Despite all the research suggesting that Australians spend little of their retirement money, the most common fear is running out of money, regardless of asset backing. And it’s understandable: you must plan and save for the future, including for unexpected spending events/decisions. Tip: Take advantage of the tools available eg. financial products that offer a guaranteed income stream for life (recent innovation in this space is remarkable.).

- Tax issues. If you give money to your children, they won’t have to pay tax on that gift. But if you sell an investment to fund the gift, there may be tax consequences, such as capital gains on any profit that you make on the sale.

If you decide to finance a future expense such as a grandchild’s education, you may need to consider the tax implications. Beware of family trust distributions to minors. Gifts are fine.

An alternative option that may avoid tax complications is to loan rather than gift money to your children. With a written loan agreement, you can set the terms to benefit and protect people according to your wishes, just beware of bank lending rules.

- May lead to more family drama. Giving money to children before you die may seem like it will reduce the prospects of inflaming family drama, yet that might not be the case. Early giving may cause resentment among loved ones who don’t receive the most of your generosity.

There can be other complications. Say you gift your child money, and they buy an apartment with the funds. They later break up with their partner, who could ask for half of the money that was put into the property purchase.

- It can affect your age pension. Centrelink has special gifting rules to prevent people from giving money away to qualify for the age pension. It says you can only give away $10,000 in one year, or up to $30,000 spread over five years, without any effect on your pension.

For amounts exceeding this, you will still be treated as though you have held onto the money for five years. The excess over the limit will be included in your assets for the pension assets test, and you will be deemed to have earned income on it for the pension income test.

Can you get around the gifting rules by selling your home or other assets to your children at a reduced price? Centrelink says gifting also includes assets that are sold or transferred for less than their market value.

- The value of effort People often appreciate the things they have had to work hard to obtain over the things that come easily.By no means is this an exhaustive list, and as always, we recommend seeking professional advice.

Know Your Biases – Take the Test

Here’s a little test to get your brain firing on all cylinders.

First, consider the following question: Jack is looking at Anne, but Anne is looking at George. Jack is happy, but George is not. Now, answer this question: Is a happy person looking at an unhappy person?

You’ve got three choices: a) yes, b) no, or c) cannot be determined.

This test is one of the ways James Montier, senior investment strategist and partner at fund manager GMO, likes to illustrate the biases and behavioural challenges that investors must overcome if they are to prevent themselves from becoming (in his words) their own worst enemy.

The starting point is our brain’s two key decision-making systems.

- The emotional approach – often defaulted to for a quick response that is full of assumptions and less than precise.

- The logical approach – requires a deliberate effort and is limited in terms of the amount of information the brain can handle.

These limitations mean we make a range of mistakes, many of which will be familiar: present bias (the tendency to value the now over the future), confirmatory bias (seeking information that affirms our views rather than seeking evidence that could prove them wrong) and anchoring (clinging to irrelevant information in the face of uncertainty).

The aim is to not only get investors to recognise these biases and their dangers but also to understand that evolution makes de-biasing hard.

Now, back to Jack, Anne and George.

The vast majority of people answer c) when in fact, the correct answer is a).

To correctly answer, you need to consider both possibilities for Anne’s state of happiness. If Anne is happy, then the answer is yes, because she is looking at George, who is not happy. If Anne isn’t happy, then the answer is still yes because Jack (who is happy) is looking at Anne.

The fact that the question setup doesn’t reveal Anne’s state of happiness suggests to people that the answer can’t be determined. Effectively, people tend to make a simple and easy (though incorrect) inference.

Rather than thinking through all the information, they focus on what seems like the logical response.

(Excerpt from Financial Review, Chanticleer, Apr 26, 2023)

Friday Funny

Looking for a higher rate of return?

Stay safe and look after one another. As always, if you have any concerns or questions at any time, please reach out to your FinSec adviser.