Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View – Democracy, Xi’s big decision, Grumpy old men (and women) and more

|

11th March 2022 |

| The coverage of the war in Ukraine reminds us how lucky we are to live in Australia – ‘Freedom and democracy’!

Our political processes are far from ideal, but our democratic institutions and practices are praised for their robustness, functionality, and resilience. One of the very reasons Vladimir Putin wants to take over Ukraine is to remove the threat of an emerging democracy as a neighbour. After all, a nearby functioning democracy could undermine his power base if Russians were to want the same. When French revolutionaries stormed the Bastille prison in 1789 in pursuit of liberty, equality, and fraternity (and weapons), they could not have imagined how far democratic political rights would have spread a mere 200 years later. In the 19th century, there were few countries one could call democracies. Today, the majority are. Australia has maintained democracy (defined as a stable liberal democratic political system under its Constitution), one of the world’s oldest, since Federation in 1901 (122 years), the USA, on the other hand, is pushing 235 years. Two centuries ago, a somewhat obscure Scotsman named Alexander Tytler made this profound observation: “A democracy cannot exist as a permanent form of government. It can only exist until the voters discover that they can vote themselves largesse from the public treasury. From that moment on, the majority always votes for the candidates promising the most benefits from the public treasury with the result that a democracy always collapses over loose fiscal policy, always followed by a dictatorship. The average age of the world’s greatest civilisations has been 200 years. These nations have progressed through this sequence: From bondage to spiritual faith; From spiritual faith to great courage; From courage to liberty; From liberty to abundance; From abundance to selfishness; From selfishness to apathy; From apathy to dependence; From dependence back into bondage.” In short, he surmised the downfall of democracy comes at a point when both the electors and the politicians learn that those who get elected are those that give the electors more of what they want. The votes are bought, albeit indirectly. The benefit of society is no longer the winner but rather the benefit of the individual. Mmm… With an ever-increasing inequality gap, the rise of woke power (the power of the disempowered) and the disruptions to a stable democracy in the USA, perhaps there may just be some credibility to the hypothesis… Who would be a politician knowing what it takes to be elected whilst your mandate is to improve the lives of every constituent! |

|

| We read recently “during the last month everything but the kitchen sink has been thrown at investors”.

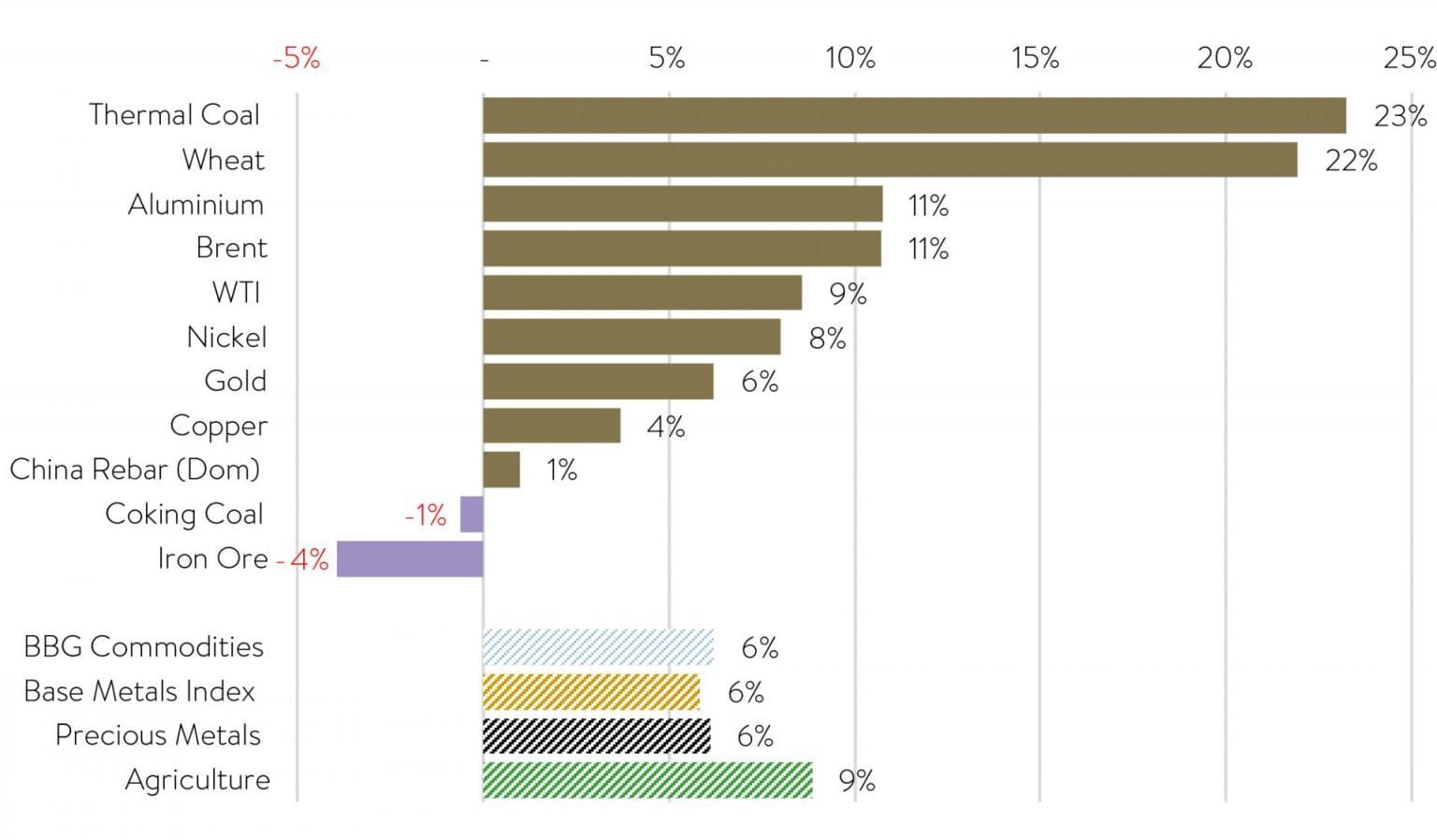

Already dealing with the spectre of rising interest rates, financial markets (and the world) we were rocked by the Russian invasion of Ukraine. Company reporting season is typically the main event during February but it took a back seat as investors tried to understand what impact the conflict will have on markets and importantly rate hikes by the US Federal Reserve. Below we cover the biggest themes in markets right now. Russia – Ukraine Beyond the human tragedy, it has the potential to throw more fuel on the inflation fire by turbocharging commodity prices (given the sanctions against Russian exports). The Bloomberg Spot Commodity Index which tracks 23 futures contracts on commodities, rose by 13% last week – the most in a week since 1960.

Source: J.P. Morgan Global Economics As we detailed last week geopolitical and military events have historically only inflicted minor damage on global share markets, with selloffs followed by speedy recoveries. Rate rises in the US The war is unlikely to stop Fed’s aggressive rate rises. With inflation at a 40 year high (and likely to now go higher) some economists are arguing for a shock and awe approach. They want to see successive 0.5% hikes each meeting this year until it gets to 2.5-3%. Other economists promote a go-slow approach arguing that inflation is likely to start heading down very soon, regardless of what the Fed does. They say that bottlenecks, which have been choking goods supply chains and causing much of today’s high prices, are easing – a leading indicator of tomorrow’s lower inflation. This said it is worth noting that the Russian-Ukraine war has added a new source of supply chain and inflation pressures. Indicators suggest that the Fed will likely get on with its job of raising rates fairly aggressively this year from March, with any escalation in the Russia-Ukraine war to make it a little more cautious. The Australian reporting season With current geopolitics at play, it is easy to forget we have just been through one of the busiest times of the year – reporting season. And, for listed corporate Australia it was a good one. The strength came from two main sectors financials and commodities. Financials (& more specifically the big banks) are benefiting from funding costs remaining low, while banks are benefitting from a lot of businesses looking to borrow to expand amid strong economic activity. For commodities, while some of the main players are facing cost issues, particularly around labour, they have not had any trouble passing this on given the health of most commodity prices. Industrials was the standout laggard, with bigger-than-average downgrades due to a host of reasons. Many were company-specific, but if there was one common theme it was cost issues that have progressively moved from higher raw materials to higher labour costs. We suspect the Ukraine war’s impact on commodity prices will keep the pressure on materials costs, given many of them are commodity-linked. What lies ahead? On equity markets, we expect the speculative tech/online sector to continue to come under pressure from the prospect of rising interest rates, but the resources sectors benefiting from higher commodity prices. With so many ‘big picture’ themes at play, it will most certainly be ‘more volatility for longer’. The world is most likely in the early stages of a long commodity boom driven by three big themes; military build-ups, the shift to renewable energy sources and infrastructure spending particularly across the US and Europe, driven partly to stimulate jobs (with unemployment remaining stubbornly high in Europe) and partly to address chronic underinvestment over the past two decades. As a principal producer of most of the key raw materials, Australia is well placed to benefit. As mentioned above the US Federal Reserve will start raising interest rates (most probably at its March meeting). In Australia, the RBA still appears reluctant to react to rising inflation. It seems to be waiting and indeed hoping for, wage rises to start a wage-price inflationary spiral. |

|

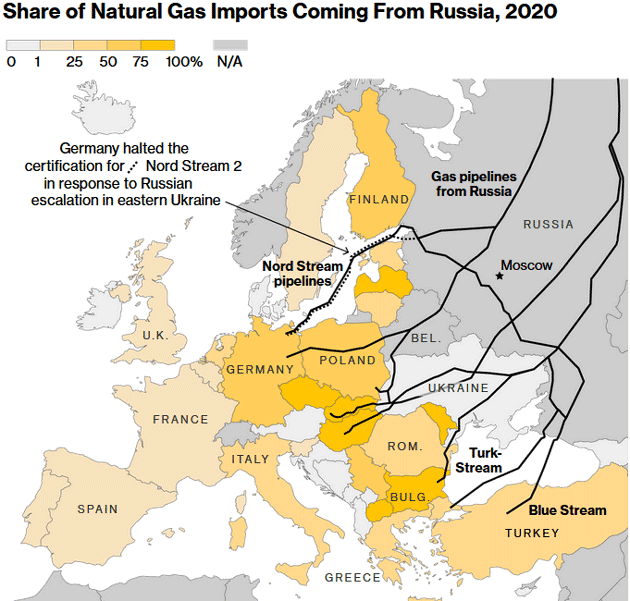

| We are guessing that Europe is now realising it may have made a strategic mistake with its dependence on Russia for its energy supplies, as this startling map shows the natural gas pipelines and share of supply from Russia and much of it from Ukraine.

One of the lessons they teach in investing 101 is ‘not to put all your eggs in one basket ‘. In a business sense, this means don’t be too dependent on any one customer or supplier. One day, you might not like their politics, their ethics, their human rights or the people you deal with. Or they may not like you! There may just be some parallels between Europe’s dependence on Russia for energy and Australia’s heavy reliance on China for our export revenues. Where once the UK, the US and then Japan dominated Australia’s export markets, today China buys by far the greatest share. In fact, Australia has not been as reliant on one country for export revenues (government tax receipts, and company profits & dividends) since the 1950’s when our largest buyer was England. China’s recent sanctions on Australia may just have done us a favour in forcing businesses to diversify, something that will be even more important if we are ever forced to choose sides over Taiwan. |

|

| It would seem Xi Jinping (Xi) has some big decisions to make.

According to a recent AFR article, China’s president may just have the greatest leverage of any world leader when it comes to brokering a peace deal between Russia and Ukraine. At the opening of the Winter Olympics last month, the joint Sino-Russian co-operation agreement was signed. “It featured a long list of common interests, as well as commitments to addressing climate change, global health, economic co-operation, trade policy, and regional and geostrategic ambitions”. In premise, China gave its unlimited support for Russia, including tempering the impact of Western sanctions. Just one month later and Russia has invaded Ukraine, adding a whole new meaning to the deal. One can’t but ponder whether this was all in Putin’s grand plan? As the esteemed political commentator Megyn Kelly said in a recent article ” (from personal experience) it’s hard for me to buy that he’s completely lost it in such a short amount of time. He’s extremely cunning, extremely manipulative, extremely well-informed, well-read and ready for anything”. Whichever way you look at it, China is in a very compromising position. If they remain committed to the new partnership, they face guilt by association. Russia is facing Western sanctions that could devastate its economy for decades and China will not want to face the same treatment. This would be in contradiction to one of Xi’s three central tenets of foreign policy, namely ‘increasing participation in international economic institutions’ in order to support China’s domestic growth. On the flip side, if they condemn Russia, it would call into question China’s conviction to the intent of the agreement. Furthermore, any perceived alliance with western forces, under American leadership in NATO, would also run counter to a third pillar of Xi’s geopolitical vision: his quest for geostrategic parity with the United States. Without China, Russia’s prospects are bleak, at best. China holds the trump card in the ultimate survival of Putin’s Russia. With Xi’s own appointment on the line, politics will certainly come into play (later this year, the 20th Party Congress will convene in Beijing. The major item on the agenda is Xi’s appointment to an unprecedented third five-year term as the Party’s General Secretary.) Xi has three choices. He can stay the course set by his February 4 agreement with Russia and be forever tainted with the sanctions, isolation, and economic and financial fallout that may come with that stance. He can broker the peace that will “end the war” and enhance his goodwill with the West. Or, he can take the middle ground that of strategic ambiguity. The full AFR article (albeit behind the paywall) can be found here.

|

|

| Director Identification Numbers (DINs)

A gentle reminder that all directors, including corporate trustees of Self Managed Super Funds (SMSF), family trusts and/or company directors in Australia must obtain a Director Identification Number (DIN) by November 1 2022. Details can be found on our website by clicking here. The fastest way to get a DIN is online using the myGovID app. To help you navigate this process, SuperConcepts have put together a simple step by step guide (with pictures). As always, if you have any questions, please reach out to a member of the FinSec team.

|

|

| Everyone knows that sensible people have a retirement plan, but a new bestseller argues that what we really need from our 50s onwards is an emotional investment plan. Although its author, Arthur C Brooks, is an economist at Harvard, his book Strength to Strength: Finding Success, Happiness, and Deep Purpose in the Second Half of Life, ignores all the usual monetary tips.

Instead, he says we must put in the effort to invest in our happiness, embrace ageing, avoid trying to compete with our past selves and most importantly, cultivate long-term relationships. “Imagine a future time, a year, five years ahead, and imagine what is making you happy, and then let your future self give your present one some advice as to what it is that you want.” This article from the Sydney Morning Herald provides a nice change of pace and includes some good sage advice to boot. Read the full article here.

|

|

| Finally, with so many passionate cricketers in the FinSec team (and our wider community), we could not end our view without acknowledging the passing of Shane Warne and Rod Marsh.

As much as people like to focus on both men’s larrikinism, it was the intensity with which they pursued their quarry that dominated. This was both their cricket brain at work as well as a visceral understanding that combining effective theatre with the substance of one’s performance is a recipe for success. Whether you’re a fan of cricket or not, it goes without saying that both men had a profound impact on Australia. From ‘Warnie’s 708 test wickets (he remains the second-highest wicket-taker of all time), his’ ball of the century’ or Rod’s 355 dismissals behind the wicket (a world record at the time) we can all agree that Australian sport is the poorer for their loss.

|

| Stay safe and look after one another. As always, if you have any concerns or questions at any time, please reach out to your FinSec adviser. |

|

|