Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View – Bitcoin, Lower for Longer and Super Update

Issue: Friday 19 February 2021

Last week was GameStop; this week, it’s Bitcoin with some similar themes – waves of money, speculation and a movement behind it.

Thanks mainly to a tweet from Elon Musk, Bitcoin has risen more than 30% in just over a week and is currently sitting just above $US50,000. Tesla’s explanation for their $1.5 billion plunge into the cryptocurrency – it had updated its investment policy to provide it with more flexibility to diversify and to maximise the returns on cash that wasn’t required to maintain adequate operating liquidity.

The strategy has ignited another round of debate about whether bitcoin is going mainstream as a financial asset and as a medium of exchange. Neither, however, is yet the case.

By design, the cryptocurrency has a limited supply, so supporters promote it as a real asset that should flourish if inflation rises. However, in reality, it is hard to pinpoint exactly why or when crypto currencies gain and lose popularity.

With no intrinsic value, it is hard to understand what Bitcoin has going for it outside of past performance based on speculation. As Perpetual chief executive Rob Adams put it in today’s AFR “Cryptocurrencies such as bitcoin are ‘vapour’ and Reddit-driven moments of ‘madness’ on the sharemarket will end in tears”.

Like everyone, we look forward to understanding Tesla’s investment motivation. We point out here that Bitcoin could move the needle for Tesla. If it goes up 10x, that’s $15 billion. With millions of followers hanging on his every word, it was inevitable that a tweet like this would lead to market demand and price rises. One wonders if he will be good enough to tweet when he sells…

Here at FinSec, we won’t be investing in an asset class we can’t understand anytime soon. Call us boring, but we’ll stick to the assets that are well underpinned by their fundamentals and can prove underlying value.

In markets this week

The Australian sharemarket fell for a second week running despite a number of strong earnings results and dividend surprises, with a heavy sell-off today offsetting a strong start to the week’s trading. With one day still to trade, in the US, the S&P500 is down 0.4 per cent and the Nasdaq is down 0.7 per cent. Bond yields continue to drift up.

A common mantra in investing circles is ‘it’s about time in the markets, not timing the markets’. A guiding principle that the Japanese Nikkei has taken to a whole new level – 30 years to be exact. This week the Nikkei returned above 30,000 for the first time since 1990, unbelievably it still remains 25% below it’s 1989 all time high of 40,000.

On home shores

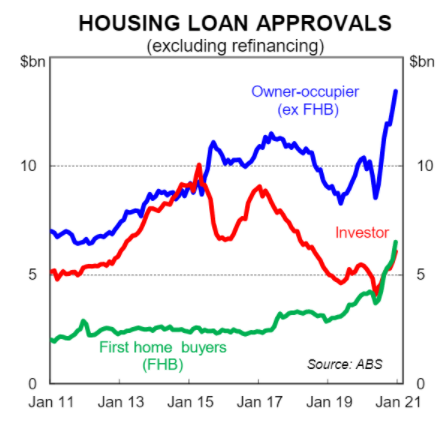

With so much money floating around and banks eager to lend, CBA economists came out on Monday with a new prediction for house prices:

“We expect strong growth in national dwelling prices of ~14% over the next two years (8 capital city basis). A critical assumption underpinning our forecasts is the cash rate remaining at its record low of 0.1%, which is in line with RBA forward guidance … Our forecast profile is centred on prices growth of 8% in 2021 and 6% in 2022. The risks are skewed towards stronger outcomes given the strength of the demand impulse from the reduction in mortgage rates over 2020.”

14% in two years is quite a jump for a group of economists who a year ago were predicting price falls. With the relaxation in the responsible lending laws and borrowers embracing sub-2% rates, it is little wonder that housing loans are growing rapidly. However, property valuations are driven as much by payment affordability as true value. Given we have had ten years of decreasing interest rates to a point where we can not reduce them anymore, payment affordability is at an all-time high. When the time comes (and it will), an increase in interest rates will have a profound impact unless wage growth can counteract it.

On Thursday we received news that Australia’s employment market grew for the 4th consecutive month with the unemployment rate dipping from 6.6% in December to 6.4% in January. Led by job growth in Victoria following its 4-month lockdown, an extra 29,100 jobs were created last month. That means 93% of jobs lost in March last year have now been recovered.

New data from the ATO also showed that by the end of December last year, more than 2.1 million employees and around 520,00 businesses had left the JobKeeper program since its first iteration came to an end in September 2020 (29% down to 13%). This latest set of numbers shows that the decline in the number of Australians on JobKeeper is currently running ahead of Treasury’s projections. and as such is consistent with the story of a (labour market) recovery that continues to beat expectations.

Whilst good news, let’s not forget this is still a substantial number of people reliant on government support, so the upcoming end of the scheme will represent an important test of the labour market’s resilience.

Chart of the Week

Our chart of the week looks at 10-year government bond yields.

2020 was an odd year in that both equities and government bonds generated positive returns. This has only ever happened on a few occasions, and typically when huge amounts of liquidity are injected into financial markets.

However, benchmark 10-year government bond yields are either at or close to record lows.

As bond prices rise as yields fall, such levels mean that further significant gains in prices will be difficult to achieve. It is expected that interest rates in major markets will be on hold for some time to come, this combined with the quantitative easing expected to last through most of this year should relieve the pressure for bond yields to rise.

Lower for Longer and Your Retirement Plans

Official interest rates in Australia are currently at an historic low. For many, this low cash rate is dragging down private pension payments and impairing returns on super balances. And, whilst for those in your 50s, 60s or retired, capital stability is a high priority, it’s a balancing act to ensure low interest rates don’t erode the value of your investment when the effects of inflation are taken into consideration.

Central Banks have indicated that ‘lower for longer’ is here to stay – So, what to do?

This article from global asset manager Schroders outlines the top tips for investing in a low rate environment. For those that have had reviews recently, the conversation may sound familiar.

Options to consider include:

- Re-allocate some cash to actively managed, higher-yielding fixed income funds for some additional volatility.

- If retirement is still some years away, consider increasing your allocation to growth assets which offer a higher return potential for higher volatility.

- Review whether your retirement target date is still a good fit for you. If you’re thinking of working longer, that extra time will give you an advantage.

- Making additional super contributions can offset the drag caused by low rates. Tax incentives may be available.

Read the article here.

Things that make you go ‘mmm’

Not only were an incredible 90% of US IPOs in 2020 made by companies which are not making a profit, but it would seem executives and board members within companies do not believe their own optimistic stories either. Insider buying (not insider trading) of shares is at its lowest level in a decade, as shown below ‘mmm’.

Superannuation

Senator Jane Hume, Minister for Superannuation, Financial Services and the Digital Economy, spoke at the Association of Superannuation Funds of Australia (ASFA) conference last week. She said superannuation is the “most frustratingly partisan sector of financial services” and she criticised the industry’s reluctance to support a reform agenda.

In what may be an election year, it is important for retirement plans and super policy to know what the Minister is thinking. For context we link to the reproduction of a speech she made to the SMSF association on Tuesday (16th February). Given the audience it is no surprise that she gives a strong endorsement of SMSFs and importantly raised the importance of the Retirement Income Covenant. Read speech here.

In more super news The Treasurer also introduced the Your Future, Your Super Bill to parliament this week. The reforms are scheduled to commence on 1 July 2021.

Information on the legislation can be found here.

Former views on the topic can be found here.

We hope that any change looks to reduce rather than increase the system’s complexity – unfortunately, when there are 3 trillion dollars involved, there will inevitably be politics and partisanship.

As Strong as an Ox

February 12 marked a very important date on the Chinese and south-east Asian calendar: Chinese New Year. The year of the rat is now behind us and celebrations continue as the Year of the Metal Ox begins.

The ox is known for being hardworking and symbolises diligence, honesty, earnestness, altruism, and never needing to be the centre of attention or seeking praise for their hard work. Where the year of the rat, the first of 12 animals in the zodiac calendar symbolised change and quick-wittedness, the year of the methodical ox will be one of endurance.

According to Chinese folklore, the one characteristic that runs dominant through the years of the ox is wealth but only for those that make a considerable effort. According to the Chinese zodiac organisation, “this year, no explosive or catastrophic events will occur, so it is a favourable year for economic recovery or consolidation, a year of long-term investments (especially for creating a reserve stock for the coming unproductive years).”

Sounds good to us!

From all at FinSec

Gong xi fa cai (Kung hei fat choi) – Wishing you wealth and prosperity

Shen ti jian kang (Sun teai geen hong) – Wishing you good health

Da ji da li (Dai gut dai lei) – Good luck and may things go smoothly.